Invoice factoring is not a loan. It's the sale of your business's unpaid invoices to a third party, and you usually receive 70% to 90% of the invoice value upfront while the factor collects payment from your customer.

If you're doing solid sales but still watching your bank balance squeeze you every payroll cycle, you're not confused. You're dealing with a timing problem. Your revenue is real, but it's trapped inside invoices that won't be paid for 30, 60, or 90 days.

That gap hits owners at the worst moments. A big customer places more orders, your team needs materials, labor, and freight now, and the cash tied up in receivables can't help you yet. On paper, the business is growing. In your operating account, it feels like you're falling behind.

That's why invoice factoring keeps coming up in conversations about working capital. It's built for companies that have already earned the money but can't afford to wait for slow-paying customers. The catch is that many owners hear only the simple version. They hear "fast cash from invoices" and miss the parts that matter most: how the fees work when customers pay late, and how a factoring arrangement can create friction if you're also pursuing SBA financing.

Table of Contents

- The Waiting Game Your Business Wins but Cash Flow Loses

- How Invoice Factoring Works A Simple Walkthrough

- Recourse vs Non-Recourse Factoring Who Holds the Risk

- Calculating the True Cost of Invoice Factoring

- Factoring vs Invoice Financing vs Lines of Credit

- The Factoring Application Process Step by Step

- Advanced FAQs for Strategic Business Growth

The Waiting Game Your Business Wins but Cash Flow Loses

A common small business story goes like this. You land a large B2B customer, send the invoice, and feel great for about a day. However, difficulties soon appear. Your customer pays on net terms, your suppliers want payment sooner, and your team expects payroll on schedule whether your customer pays early or not.

That mismatch creates pressure in otherwise healthy businesses. You can have a full sales pipeline and still feel cash poor because accounts receivable isn't the same thing as cash in the bank. If you've ever delayed a purchase order, stretched a vendor payment, or used your line of credit to bridge a customer delay, you've felt the waiting game firsthand.

Invoice factoring exists to solve that exact problem. Instead of waiting for the customer to pay, you sell the invoice and turn that future payment into cash you can use now. It's not some fringe tactic for distressed companies either. The global invoice factoring market was valued at USD 2,856.4 billion in 2024 and is projected to reach USD 7,752 billion by 2034, while recourse factoring accounted for over 76.1% of the market in 2024, according to invoice factoring market data from Market.us.

Cash flow stress usually starts after the sale

Most owners don't need help making the sale. They need help surviving the delay between invoicing and collection.

A few examples make that clear:

- Payroll pressure: You finish the work this week, but your customer won't pay for weeks.

- Inventory strain: A new order should be good news, yet you need cash now to buy stock or materials.

- Growth bottlenecks: You turn down opportunities because too much working capital is trapped in receivables.

Practical rule: Profit can look healthy while cash flow still feels tight. Those are related, but they aren't the same thing.

If you're trying to get tighter control over timing problems like these, resources on ReceiptsAI on cash flow can help you think through the operational side, and this guide on how to improve cash flow is useful when you want broader funding and cash management options.

Why owners get interested in factoring

Factoring appeals to established companies because it uses an asset they already have. You already did the work. You already issued the invoice. You're not borrowing against a future idea. You're accelerating payment on a completed sale.

That makes factoring powerful. It also makes it easy to underestimate the tradeoffs if you focus only on the upfront cash and ignore how collections, risk, and fee timing affect the final result.

How Invoice Factoring Works A Simple Walkthrough

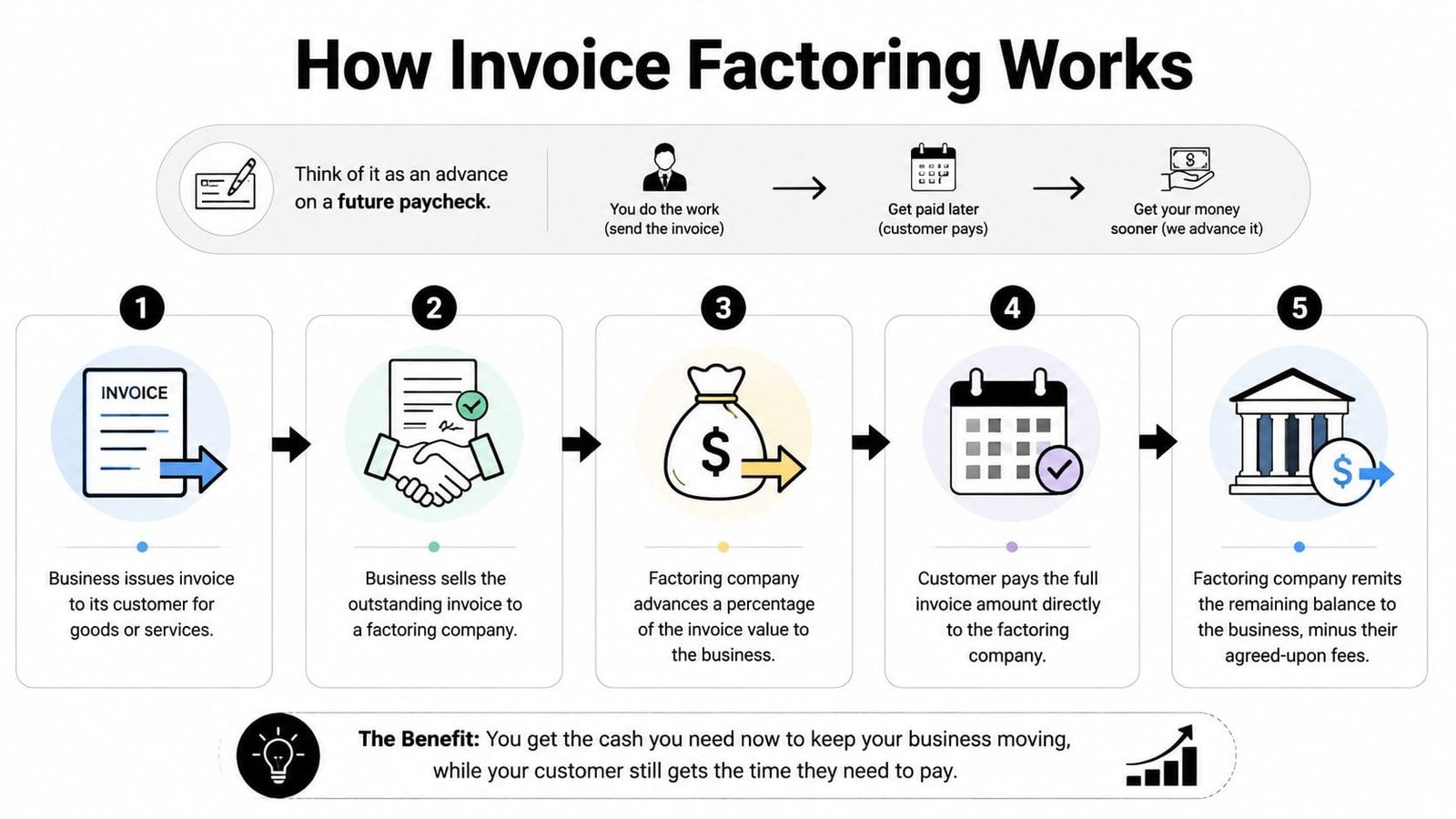

Your team finishes a job on Monday, sends a clean invoice on Tuesday, and still has to cover payroll before that customer pays. Invoice factoring changes that timing. It lets a business turn an unpaid invoice into cash sooner by selling the receivable to a factoring company.

That sounds simple, but the timing detail matters more than the label. For many established companies, the cost of slow payment is not just annoyance. It is overtime you cannot comfortably fund, supplier discounts you miss, rush freight you pay because cash arrived late, and growth decisions you postpone while money sits in accounts receivable.

A direct example of how the process works

Say you deliver products to a creditworthy commercial customer and issue an invoice with net terms. Instead of waiting through the full payment cycle, you submit that invoice to a factor. The factor reviews the invoice and the customer's payment profile, then sends you part of the invoice value upfront.

Businesses typically receive an upfront advance of 70% to 90% of the invoice value, and the fee for that service typically ranges from 1% to 5% of the invoice value per month, according to Allianz Trade's overview of invoice factoring.

If you want another plain-English breakdown before you compare providers, this guide on understanding invoice factoring adds helpful context.

The money flow in plain English

Here is the sequence most owners care about:

You deliver the work and issue the invoice.

The receivable now exists on your books, but the cash has not arrived.You assign or sell that invoice to the factor.

The factor checks that the invoice is valid and that the customer is likely to pay.You get an advance.

This is the first cash payment from the factor, usually a percentage of the invoice rather than the full amount.The customer pays the factor.

Payment goes to the factor under the arrangement you signed.You receive the balance, minus fees.

The factor releases the reserve after collecting from the customer and subtracting its charges.

A simple way to picture the reserve is as a holdback account. The factor keeps part of the invoice in place until the customer pays. Owners often focus on the advance and overlook that second half of the transaction, which is where the final economics become clearer.

That is also where hidden costs start to show up.

If your customer pays later than expected, the fee can keep running depending on the agreement. A deal that looked manageable at funding can become much more expensive by the time the reserve is released. The invoice did not change. The calendar did.

Another point gets missed in many basic explanations. Factoring can also affect future borrowing options, especially for established businesses that may want an SBA loan later. If a lender sees a broad factoring arrangement, concentrated customer risk, or strained receivables quality, that can change how your borrowing profile is viewed. Factoring is not automatically a problem, but it should be weighed against what it may signal when you apply for lower-cost bank or SBA-backed financing.

What confuses owners is the phrase "sale of invoices." In day-to-day terms, it means you are converting a receivable into earlier cash, while the factor takes over collection rights tied to that invoice.

Factoring improves timing first. Whether it improves your overall financing position depends on the fee structure, your customer payment habits, and your plans for future credit.

A short video can make that sequence easier to absorb:

For operations, the appeal is straightforward. Faster access to cash can help cover payroll, inventory, freight, repairs, and vendor payments. The smarter question is whether the speed you gain is worth the fees, the collection structure, and any tradeoff it creates for future financing.

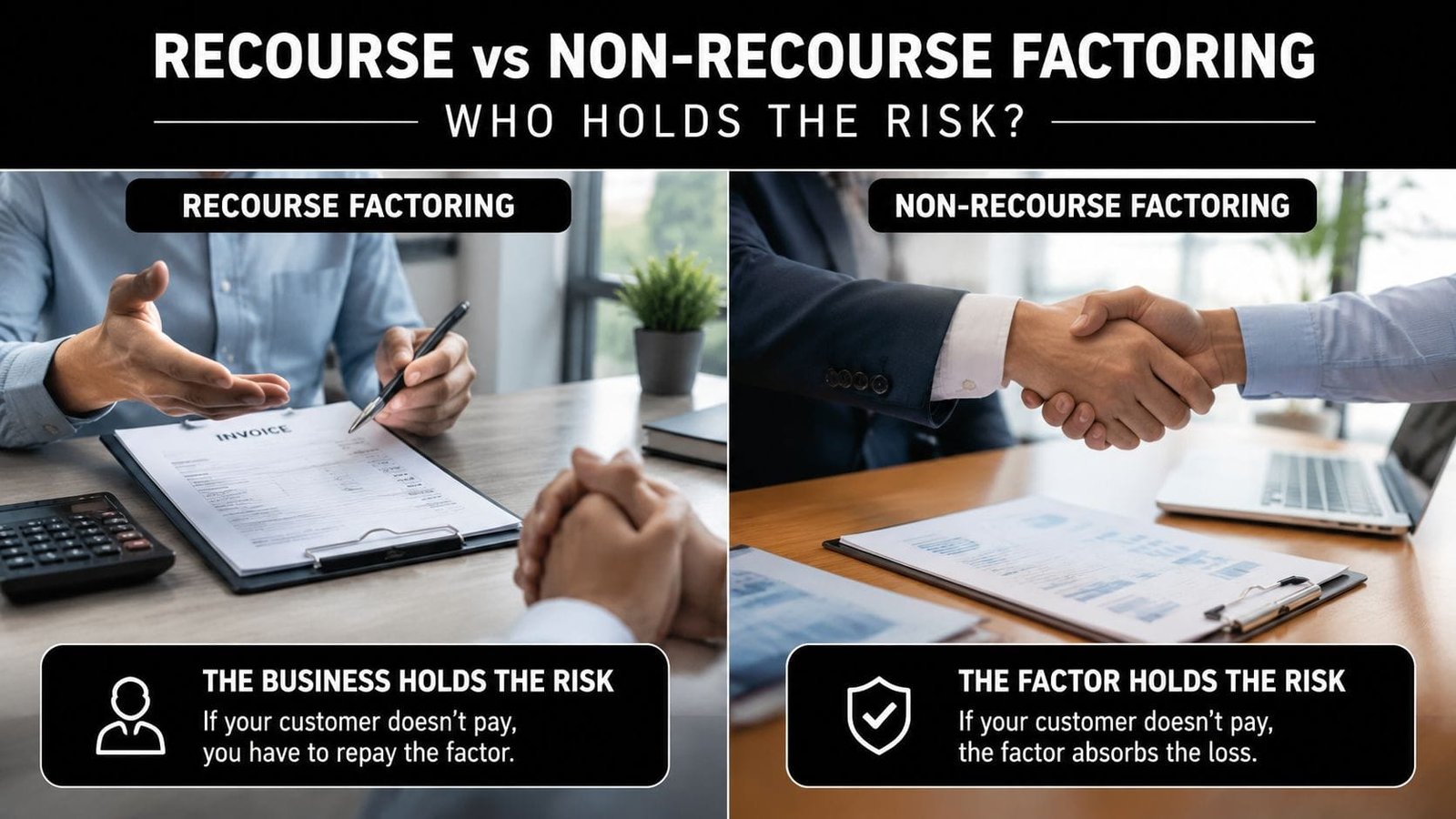

Recourse vs Non-Recourse Factoring Who Holds the Risk

Most factoring decisions come down to one question. Who takes the loss if the customer doesn't pay? That's where recourse and non-recourse factoring part ways.

Recourse factoring means you keep more of the default risk

In a recourse arrangement, the factor advances cash and handles the transaction, but if the customer ultimately fails to pay under the agreement terms, your business remains responsible.

That structure is common because it leaves more protection with the factor. According to Sage's explanation of invoice factoring structures, a factor underwrites the customer's ability to pay, and advance rates commonly fall in the 80% to 90% range, with fees and terms influenced heavily by the debtor's credit quality.

Recourse factoring often fits businesses that:

- Know their customers well: You trust the payer and have a long payment history with them.

- Want lower cost structures: More seller risk often translates into more favorable pricing.

- Can absorb occasional problems: If an invoice goes bad, your company can replace it or buy it back.

Non-recourse factoring shifts some credit risk to the factor

In non-recourse factoring, the factor takes on specified credit-related default risk. That's the key phrase: specified credit-related risk. It doesn't usually mean the factor covers every possible reason an invoice goes unpaid.

For owners, this often leads to misunderstandings. If a customer goes bankrupt, a non-recourse structure may offer protection depending on the contract. If the customer disputes the work, rejects the shipment, or claims the invoice is invalid, that may be treated very differently.

A simple way to compare them:

| Type | Main upside | Main tradeoff |

|---|---|---|

| Recourse | Usually simpler and often less expensive | Your business may have to repay or replace unpaid invoices |

| Non-recourse | More protection against certain credit defaults | Usually higher cost and tighter eligibility |

The factor is often judging your customer more than your company. That's one reason factoring can work for firms that have strong buyers but uneven cash flow.

The right choice depends less on preference and more on your customer base. If a few large customers dominate your receivables, the risk terms deserve close scrutiny before you sign anything.

Calculating the True Cost of Invoice Factoring

The headline fee is rarely the whole story. The actual cost of factoring often depends on how long your customer takes to pay, not just the percentage you were quoted at the start.

Why the reserve can disappoint owners

Many guides describe factoring fees as if they were flat. In practice, the fee is often tied to the factoring period, meaning the number of days the invoice remains unpaid. According to Paychex's discussion of invoice factoring, a customer delay can cause the fee to double or triple, and 42% of small businesses overestimate their net cash from factoring because they miss this detail.

That matters because owners tend to focus on the advance and underpay attention to the reverse side of the deal, the reserve payment that arrives later. If the customer pays later than expected, the factor may continue charging based on time outstanding. The reserve shrinks while your original operating need, payroll, materials, freight, taxes, doesn't shrink at all.

Here's the practical issue. A quote can sound manageable when you assume quick customer payment. The same quote can feel expensive when your customer drifts beyond their usual cycle.

Watch the clock, not just the rate. A low-looking fee can become a costly one if your customer pays slowly.

Questions to ask before you sign

When owners get surprised by factoring costs, it's usually because they asked "What's the rate?" but not "How does the rate behave over time?"

Ask these instead:

- How is the fee calculated: Is it tied to the actual days outstanding, and how often does it accrue?

- What reduces my reserve: Which charges come out of the final payment besides the base fee?

- What happens if the customer pays late: Does the fee step up after a certain point or continue accumulating?

- Who handles disputes and deductions: If the customer short-pays, who absorbs the gap?

- What exit costs apply: Are there documentation, servicing, early-termination, or buyout charges?

Another source of confusion is terminology. One provider may quote a discount fee and separate service charges. Another may bundle charges differently. If you don't compare the full fee structure, you can mistake a cleaner quote for a cheaper one.

A good rule is simple: estimate your net cash using your customer's slowest realistic payment behavior, not their best behavior. That's the risk-adjusted way to decide whether factoring helps or erodes margin.

Factoring vs Invoice Financing vs Lines of Credit

Invoice factoring isn't the only way to access working capital from receivables. Owners often compare it with invoice financing and business lines of credit because each solves a different kind of cash gap.

Financing Options at a Glance

| Feature | Invoice Factoring | Invoice Financing | Business Line of Credit |

|---|---|---|---|

| What you're using | Sale of invoices | Borrowing against invoices | Revolving credit facility |

| Who controls collections | Factor usually handles collections | Your business usually keeps collections | Your business keeps collections |

| Does the customer know | Often yes | Often less visible to the customer | No customer involvement |

| Approval focus | Strength of your customers and invoices | Your receivables and business profile | Your business credit, cash flow, and lender criteria |

| How funds are used | Tied to factored invoices | Tied to financed invoices | Flexible for broader working capital needs |

| Best fit | Businesses that want cash now and may welcome outsourced collections | Businesses that want to keep customer communication in-house | Businesses that want reusable access to capital for multiple needs |

If you want a deeper side-by-side on the cousin product, this guide to invoice financing helps clarify where financing and factoring split apart.

Which option fits which situation

Factoring tends to fit companies that care most about speed and cash conversion. If your back office is stretched, having a factor involved in collections can be a feature, not a bug.

Invoice financing usually appeals to owners who want to preserve more direct control over customer contact. They need liquidity, but they don't want a third party stepping into the payment relationship.

A line of credit is different. It isn't built around a specific invoice sale or advance. It's broader and more flexible, which makes it useful when your cash needs don't line up neatly with invoiced work. Think repairs, seasonal inventory builds, uneven payroll cycles, or a short-term operating cushion.

A fast decision guide:

- Choose factoring when the main problem is slow customer payment on completed B2B invoices.

- Choose invoice financing when you want to borrow against receivables but keep collections closer to home.

- Choose a line of credit when you need repeat access to capital for mixed operating needs.

If your issue is timing between invoicing and collection, factoring can be a strong fit. If your issue is broader working capital volatility, a line of credit may be cleaner.

The best option isn't the one with the simplest pitch. It's the one that matches how your company gets paid and how much control you want to keep.

The Factoring Application Process Step by Step

The application process is usually less mysterious than owners expect. A factor wants to understand your invoices, your customers, and whether the paperwork behind those invoices is clean.

What you'll usually need

Most applications move through four stages.

Initial application and quote

You provide basic company details, information about your customers, and the invoices or receivables you want the factor to review.Underwriting and due diligence

The factor evaluates the quality of your receivables and the payment strength of your customers. Complete records are particularly important at this stage.Contract and onboarding

If approved, you review the agreement, verify how collections will work, and confirm the fee structure, reserve treatment, and any termination language.Funding the first invoice

After setup is complete, you submit eligible invoices and receive the first advance.

A practical document checklist usually includes:

- Accounts receivable aging report: To show what customers owe and how old each balance is.

- Customer list: So the factor can review the businesses that will ultimately pay.

- Sample invoices and contracts: To confirm the underlying work, goods, and payment terms.

- Company formation documents: Basic records that establish your business entity and authority.

- Banking and operational records: To support onboarding and payment setup.

If your invoicing process is messy, funding gets slower and misunderstandings increase. That's why many finance teams tighten invoice workflows before applying. If you're reviewing systems that support cleaner billing and collections across borders, this roundup of invoicing tools for global payments is a useful place to start.

The smoother your records, the smoother the underwriting conversation. Factoring companies don't just want receivables. They want receivables they can verify, collect, and trust.

Advanced FAQs for Strategic Business Growth

Established companies rarely stop at "How does factoring work?" The better questions are strategic. How does it affect other funding plans? Can you use it selectively? What does it signal to customers?

Can factoring hurt SBA loan eligibility

It can. Even though factoring isn't technically a loan, some SBA lenders may treat factored receivables more like debt for underwriting purposes. According to NerdWallet's discussion of invoice factoring and SBA lending, lenders often reclassify factored receivables as debt, and a U.S. Chamber of Commerce study found 28% of SBA rejections for businesses using factoring were tied to this debt mischaracterization rather than credit scores.

For an owner planning a dual-funding strategy, that's a major issue. You may use factoring to smooth working capital, then find that the documentation or lender interpretation weakens your SBA profile. The problem isn't that factoring is bad. The problem is that balance sheet presentation and lender treatment may not match the simple "it's not debt" story owners hear upfront.

If you're weighing fast capital options against longer-term borrowing plans, this comparison of short-term loans, MCA, and invoice factoring for quick capital gives useful decision context.

Before you combine factoring with an SBA application, ask your lender how they will classify the arrangement. Don't assume the legal definition and underwriting treatment are the same.

Other questions established businesses ask

Can I factor only certain invoices?

Sometimes, yes. Some structures allow selective use, while others are designed around a broader receivables relationship. The contract language matters.

Will customers think my business is in trouble?

Not necessarily. In many industries, receivables finance is a normal working capital tool. Customer communication still matters. A clean notice process and professional collections approach can make the arrangement feel routine.

Is factoring a good growth tool?

It can be, especially when growth itself is what's creating the cash squeeze. But it's strongest when used with discipline. If slow invoicing, weak collections processes, or customer concentration are the issue, factoring may relieve pressure without fixing the underlying cause.

When is factoring a poor fit?

It's usually a weaker fit when invoice disputes are common, margins are already thin, or you're preparing for lending events where debt appearance matters as much as legal structure.

Owners who use factoring well tend to treat it as one financing tool, not a universal solution. They model the timing risk, understand who holds the default risk, and check how the arrangement will look to future lenders before they sign.

If you're weighing invoice factoring against SBA loans, lines of credit, or other working capital options, Business Loan Warrior can help you compare funding paths and find a structure that fits your cash flow, growth plans, and underwriting goals.