Most advice on a business loan with EIN gets one thing wrong. It treats the EIN like a shortcut to funding, as if the number itself convinces a lender to take risk.

It doesn't.

An EIN is useful for a different reason. It gives your company its own financial identity, which is the first step toward separating business debt from personal debt. That matters if you're trying to stop running everything through your own credit, your own bank account, and your own name. But lenders still want evidence that the business can repay what it borrows.

That's where many owners get stuck. They have the EIN, the LLC, maybe even a clean formation file. What they don't have yet is the operating trail lenders trust: bank activity, payment history, documented revenue, and financial statements that hold up under review.

Table of Contents

- Get a Business Loan with an EIN the Right Way

- Understanding What Your EIN Actually Does for Lenders

- Comparing Loan Types and What Lenders Prioritize

- How to Build Strong Business Credit from Scratch

- Preparing Your Documents for a Successful Application

- Avoiding Common Mistakes When Applying for an EIN Loan

Get a Business Loan with an EIN the Right Way

Seeking a business loan with an EIN likely means you're aiming to do something smart: move borrowing into the business and reduce dependence on personal finance. That's the right goal. The bad advice is thinking the EIN alone gets you there.

In practice, the EIN is the front door, not the approval letter. It helps the business exist in the financial system under its own identity. After that, lenders look for proof that the company operates like a real borrower and not just a registered shell.

That distinction matters because business borrowing is large, but approval is far from automatic. The UK business loans market is reported at £485.9 billion, with SMEs borrowing an estimated £62.1 billion annually. Even with that volume, only about three in five UK SMEs had their applications approved, according to Money.co.uk's business loan statistics. The lesson is simple: demand for funding is mainstream, but preparation still decides who gets through underwriting.

What works in the real world

Owners who get traction usually do three things well:

- They separate finances early. Revenue lands in a business account. Expenses leave from a business account. That gives lenders a clean trail.

- They borrow for a clear use. Equipment, working capital smoothing, inventory, hiring, expansion. Specific uses are easier to underwrite than vague "growth."

- They match the product to the business. A company with strong receivables may fit invoice-based funding better than a long-term unsecured loan.

What doesn't work

A few patterns fail over and over:

- Relying on formation alone. An LLC and EIN without operating history won't carry much weight.

- Mixing personal and business transactions. That muddies the cash flow picture and slows review.

- Applying blind to every lender. Different lenders care about different risks. One size doesn't fit all.

Practical rule: Treat your EIN like the frame of a building. It's necessary. It isn't the plumbing, wiring, walls, or roof.

Owners who understand that move faster. They stop asking, "Can I get approved with just my EIN?" and start building the file that makes the business lendable.

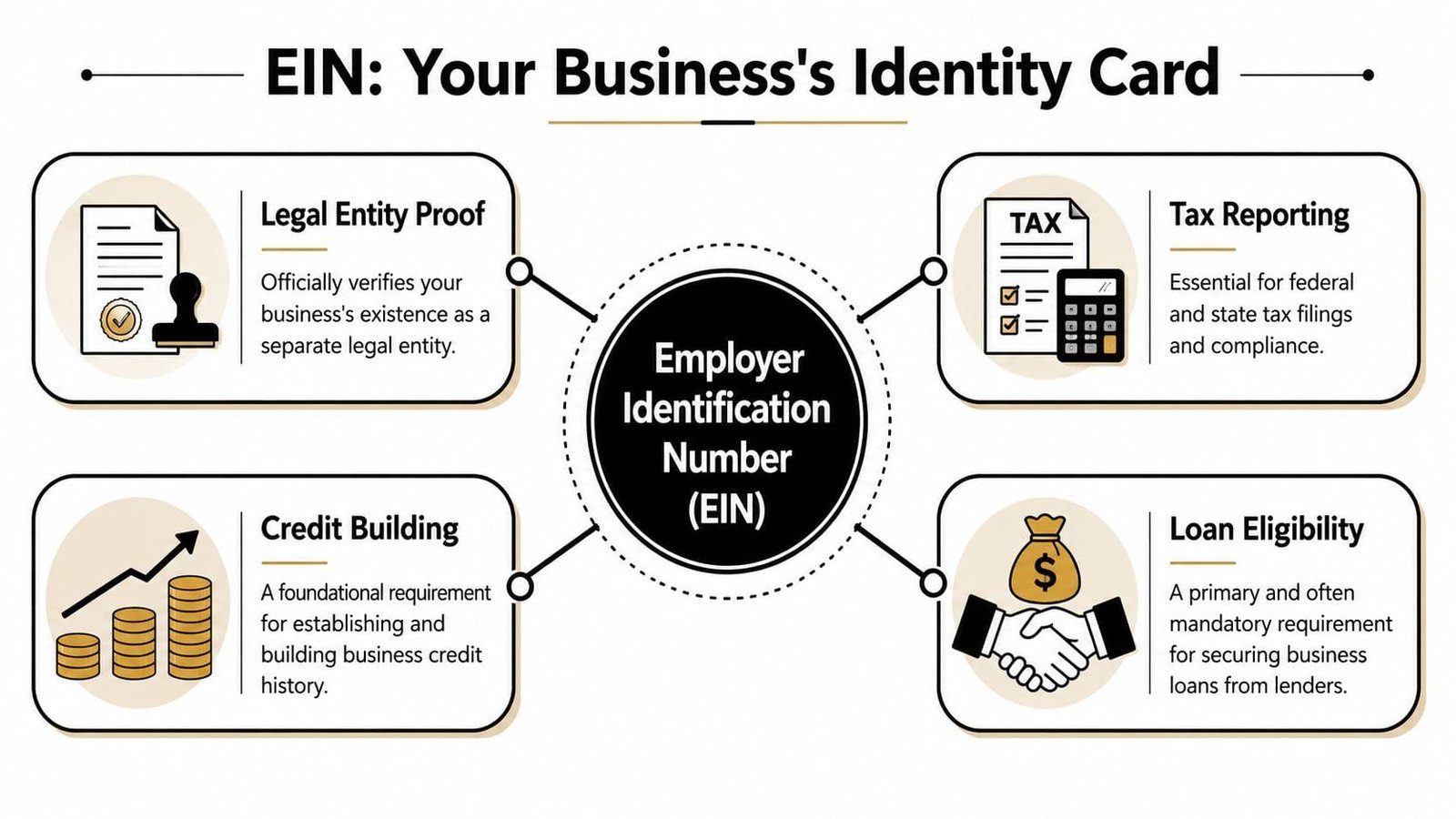

Understanding What Your EIN Actually Does for Lenders

A lot of owners start in the wrong place. They hear "business loan with EIN" and assume the EIN is the approval trigger. It isn't. An EIN is the business identifier that lets lenders, banks, and credit bureaus pull the right file. If that file is thin, the EIN does not carry the application.

Your EIN proves business identity

An EIN works like a business tax ID card. It confirms the company exists as a separate legal and tax entity, which matters if your goal is to stop using your personal identity for every financial step.

That separation is the starting point. The IRS explains that businesses use an EIN to identify the business for tax administration, and lenders use that same identifier to match your application to your legal entity, bank records, and business credit file when one exists. A lender can verify the company. A lender still has to decide whether the company is lendable.

A new EIN has no repayment history attached to it. No revenue trend. No deposit pattern. No evidence that the business can take on debt and pay it back on schedule.

What lenders use the EIN to connect

In underwriting, the EIN is less like a key and more like a file label. It helps the lender pull together the records that matter.

Those records often include:

- business bank account activity

- revenue consistency

- time in business

- trade line or business credit history

- entity documents and ownership details

- any required personal guarantee from the owner

This is why owners get confused. They did the paperwork, formed the LLC, got the EIN, and opened the door. The lender is still looking past the door at the operation itself.

The SBA makes the same point in practice across its lending guidance. Approval depends on the strength of the business, the purpose of funds, and the applicant's ability to repay, not on having an EIN by itself. If you are comparing options, this matters even more with different alternative business loan products, because some lenders put more weight on deposits, some on receivables, and some on owner backing.

What an EIN can help you build over time

Used the right way, an EIN helps separate business finance from personal finance. That is its primary value.

It lets you open and run a true business bank account. It gives vendors and bureaus a way to report payment history to the business. It supports applications in the company's name. Over time, those steps can create a business profile that gives lenders more to review than your personal credit alone.

A lender is not funding a tax ID. The lender is funding a business with a record it can verify.

That is the practical way to view an EIN loan. The EIN starts the file. Your banking history, revenue, credit behavior, and documentation are what make that file strong enough to approve.

Comparing Loan Types and What Lenders Prioritize

The phrase business loan with EIN covers very different products. Some lenders care mostly about the company's operating performance. Others will still lean heavily on the owner's personal backing, especially when the debt is unsecured.

Where underwriting leans on the business itself

If the financing has clear support from business assets or business cash conversion, the lender can focus more on the company than on the owner.

| Loan Type | Primary Underwriting Focus | Personal Guarantee (PG) Typically Required? |

|---|---|---|

| Equipment financing | Value and usefulness of the equipment, plus business cash flow | Sometimes not, especially when the equipment strongly supports the deal |

| Invoice financing | Quality of receivables and payment behavior of customers | Often less central than in unsecured lending |

| Revenue-based or cash-flow financing | Bank activity, deposits, and operating consistency | Often still possible, but business performance plays a larger role |

These products make sense when the lender can point to something concrete. Equipment can be repossessed. Receivables convert into cash. Bank activity can be analyzed for patterns. If you're evaluating nonbank options, it's worth reviewing different alternative business loan products before choosing a structure.

Where personal guarantees usually stay in the picture

Unsecured lending is a different animal. If there's no obvious collateral and the business is still developing its credit profile, lenders often want the owner as a backstop.

| Loan Type | Primary Underwriting Focus | Personal Guarantee (PG) Typically Required? |

|---|---|---|

| Unsecured term loan | Cash flow, credit profile, and overall risk | Frequently yes |

| Business line of credit | Ongoing liquidity, account behavior, and credit strength | Common for younger or thinner-file businesses |

| SBA-backed loan | Full business profile, documentation quality, and credit strength | Common in practice for many owner-operated firms |

Expectations matter. Many owners pursue the wrong product because they want "EIN-only" funding in the abstract, when what they need is financing built around business performance.

The fastest way to narrow the field

Use this filter before applying:

- If the business owns or is buying a hard asset, start with asset-backed products.

- If the business invoices other businesses, look at receivables-based options.

- If the business has steady deposits but limited collateral, cash-flow products may be more realistic.

- If you're chasing long terms and lower cost, expect deeper review and more documentation.

The mistake is treating all lenders like they read the same file the same way. They don't. A term lender, an equipment lender, and an invoice finance provider are looking at three different risk stories even when the same EIN sits on top of the application.

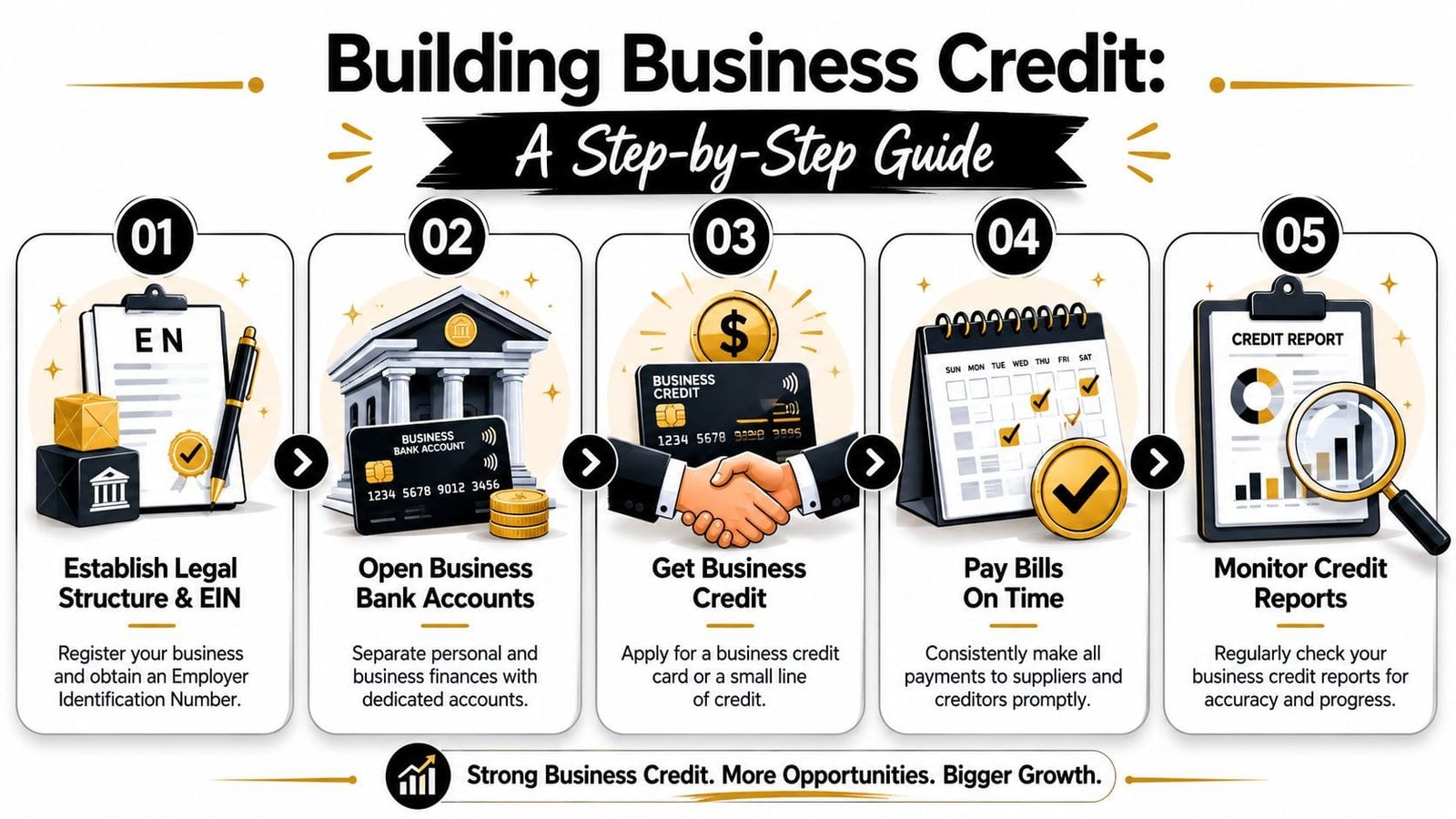

How to Build Strong Business Credit from Scratch

An EIN starts the file. It does not make the file strong.

That distinction matters because many owners hear "business loan with EIN" and assume the number itself carries lending weight. It doesn't. Lenders use the EIN to identify the business. Approval comes from the record attached to it.

Start with clean separation

The first job is to stop blending business activity with personal money. Open a business checking account under the company name and EIN, then run operations through that account with discipline. Deposits, payroll, rent, software, inventory, owner draws, and vendor payments should move through one business system that matches the legal entity applying for credit.

Owners sometimes ask whether this step is just bookkeeping hygiene. It isn't. Underwriters look for a business that behaves like a business. If revenue lands in a personal account and expenses are paid from three different cards, the lender has to guess. Guessing raises risk.

Clean separation also makes weak spots obvious. If balances swing hard, if transfers to the owner are irregular, or if recurring expenses are eating margin, it shows up early. That gives you time to fix the pattern before a lender reviews it.

Build a file lenders can verify

Business credit starts small. The goal is not to stack accounts fast. The goal is to create a record that can be checked and trusted.

Use a simple sequence:

- Set up vendors that report payment history. Net terms with reporting suppliers can help establish the first trade lines in the business name.

- Add one manageable revolving account. A business card or small credit line used for routine expenses works well if balances stay controlled.

- Pay on time every time. Early payments help. Late payments hurt more when the file is thin.

- Monitor business credit reports for errors. A wrong address, duplicated account, or missing trade line can weaken the picture lenders see.

This works like building trust with a landlord. One on-time payment does not prove much. A long stretch of clean payments, stable account use, and consistent activity proves the business can handle obligations without chaos.

For a more tactical step-by-step plan, see this guide on building lender-trusted business credit in the first 90 days.

Good business credit is documented behavior, not branding.

A short explainer can help if you're visualizing the process.

Review the process visually

Strip away the marketing language and the sequence is straightforward.

- Form the business and get the EIN. That gives the company a legal and tax identity.

- Open dedicated business banking. This creates a transaction history tied to the company.

- Add a few accounts in the business name. Start with ones the business can handle comfortably.

- Keep payment behavior clean month after month. Consistency matters more than speed.

- Review the credit file before applying. Fix errors and tighten weak spots first.

Two companies can have the same age, the same industry, and an EIN. The one with cleaner banking, better payment history, and a more consistent paper trail is the one lenders take seriously.

Preparing Your Documents for a Successful Application

Applications fall apart less from bad intent than from weak documentation. If a lender can't verify what the business earns, how money moves, or who owns the entity, the file slows down or dies.

What to gather before you apply

Think like an underwriter for a minute. They aren't looking for paperwork because they enjoy paperwork. They're trying to answer three questions: Is the business real, does it generate enough money, and does the story in the application match the documents?

A practical file usually includes:

- EIN confirmation and formation records. These tie the legal entity to the application.

- Recent business bank statements. Lenders review these for deposits, balances, swings, and operating behavior.

- Profit and loss statements or annual financials. These show whether revenue translates into actual operating strength.

- Ownership and identity documents. Lenders need to confirm who controls the company.

- Tax records when required. These help validate consistency across filings and internal reports.

Bring documents that agree with each other. A lender can work with average numbers more easily than conflicting numbers.

Why connected bank data matters

A common underwriting benchmark for EIN-based business lending is recent bank-account transactions and annual financial statements. In efficient digital applications, linking a bank account allows lenders to analyze revenue in real time, reduce manual review, and speed up offers, according to Banxware's overview of current business loan underwriting.

That changes the application experience. Instead of emailing PDFs back and forth, many lenders can review live transaction data first, then ask for backup documents only where the file needs support.

For owners, that means two things:

- Clean account activity matters more than polished storytelling.

- Messy bookkeeping creates friction even in fast digital applications.

If you want a leaner submission process, this checklist on minimal documentation for a quick small business loan is a useful benchmark.

A strong application isn't fancy. It's consistent, complete, and easy to verify.

Avoiding Common Mistakes When Applying for an EIN Loan

The biggest mistake is simple. Owners confuse having an EIN with being credit-ready.

That shows up in predictable ways. They apply too early. They mix personal and business spending. They can't explain revenue swings because the bookkeeping isn't current. Or they chase an unsecured product when the business would fit better into asset-backed or cash-flow-based underwriting.

The mistakes that slow approvals

These are the errors that show up most often in real files:

- Commingled funds. If personal and business transactions live in the same account, the lender can't easily isolate operating performance.

- Thin documentation. Missing statements, outdated financials, or inconsistent ownership records create delays fast.

- Weak product fit. A borrower with solid receivables may get nowhere with one lender and move quickly with another because the product matches the business better.

- Ignoring the business credit file. If there's an error or missing trade data, the business can look weaker than it is.

A better question to ask lenders

For firms with an EIN but limited bankability, the market is moving toward more automated underwriting. The more useful question isn't "Can I get funded with an EIN?" It's which products can underwrite using bank data and business performance instead of just legacy credit files, a framing that is especially relevant for firms in the $20M to $50M revenue band, as discussed on BDC's financing guidance.

That question forces a better strategy. It pushes you toward lenders and products that can read your operating reality.

If your business is stronger than your paper file, look for underwriting that can see the business in motion.

A good next step is practical, not theoretical. Check the business credit profile. Clean up the bank story. Organize the documents. Then test the market with a platform that lets you compare realistic options before committing.

If you want to see where your business stands without turning the process into a full-time job, Business Loan Warrior is built for that. You can submit a single, no-fee application, check pre-approval without affecting credit, connect business bank data securely, and review customized funding options across products like term loans, SBA processing, equipment financing, invoice financing, and working capital. It's a practical way to find out whether your EIN is attached to a fundable business profile, and what to improve if it isn't.