You've got a payroll run coming up, inventory needs to land before the busy season, or a new contract is sitting on your desk waiting for equipment you haven't bought yet. The bank says it can look at the file, but first it wants tax returns, financial statements, collateral details, and patience. Lots of patience.

That's where most owners get stuck. Not because the business is weak, but because the timing is wrong. A good opportunity can die while a conventional lender moves through committee.

Alternative business loans exist for that exact gap. They're not magic, and they're not cheap by default. But they are often practical. The mistake I see most often isn't taking alternative capital. It's taking the wrong kind of alternative capital without calculating the actual cost, the repayment pressure, and the better options that may already be available to an established company.

Table of Contents

- When The Bank Says No or Too Slow

- Traditional vs Alternative Loans A Strategic Comparison

- Decoding The Types of Alternative Business Loans

- Choosing Your Funding Path A Framework for CEOs

- Your Step-by-Step Alternative Loan Application Guide

- The True Cost of Speed Common Pitfalls to Avoid

- Your Top Alternative Lending Questions Answered

- Secure Your Best Offer with Business Loan Warrior

When The Bank Says No or Too Slow

A restaurant group gets the chance to take over a neighboring space. A distributor can lock in a favorable inventory buy, but only if cash goes out this week. A service company lands a large customer and needs to hire before the first invoice gets paid. These are strong-business problems. They still create a financing crisis when the bank timeline doesn't match the business timeline.

Banks are built for measured underwriting. That works well when the project is planned months ahead. It fails when the need is immediate or when the borrower is solid but doesn't fit a narrow credit box.

That's why alternative business loans moved from fringe option to mainstream financing channel. One market summary says annual U.S. alternative lending originations surpassed $200 billion by the mid-2020s, while traditional banks posted a 56% denial rate for small business loans. The same summary says alternative lenders can approve 60% to 80% of qualified applicants and often fund in 1 to 3 days according to Crestmont Capital's alternative lending statistics roundup.

If you've been wondering whether this category is just a desperation play, it isn't. It's now part of normal capital strategy for companies that need speed, flexibility, or a different underwriting model.

Practical rule: If the cost of missing the opportunity is higher than the cost of fast capital, alternative financing deserves a serious look.

The real issue is timing

Owners usually ask, “Can I get approved?” The better question is, “Can I get the right money before the business need expires?”

That's why funding timelines matter as much as rates. If you're trying to judge whether a lender can move fast enough, this breakdown of realistic timelines for small business funding from application to cash in your account is worth reading before you apply.

Mainstream does not mean automatic

Alternative lenders still look for signals that the business can carry the payment. Strong deposits, consistent revenue, invoice quality, recurring customer activity, or equipment value can all matter more than a perfect bank-style package.

That shift helps established operators who are growing fast, running lean, or carrying less traditional collateral. It also creates a trap. Fast approvals can make owners ignore structure, repayment frequency, and total cost. Don't do that. Fast money is useful. Blindly expensive money is not.

Traditional vs Alternative Loans A Strategic Comparison

Stop thinking about this as “bank loan versus online loan.” Think of it as planned capital versus responsive capital.

A bank is like a commercial airline. It's cheaper when you can book ahead, follow the schedule, and fit inside the system. An alternative lender is closer to chartered transport. It moves faster, adapts more easily, and charges for that flexibility.

Where the models differ

Traditional loans usually reward preparation. Alternative business loans usually reward current operating performance.

One lender-focused analysis notes that SBA lending is attractive because federal guarantees can cover 75% to 90% of the loan, and lenders may also receive an additional 7% to 9% fee when loans are sold on the secondary market. The same analysis says Square offers business loans from $100K to $350K using operating signals like platform history, processing volume and frequency, and customer mix, rather than relying only on traditional collateral or tax-return-heavy underwriting, as described in Balanced Comp's SBA lending analysis.

That tells you something important. These aren't just different lenders. They are different math.

Side-by-side decision lens

| Decision factor | Traditional bank or SBA route | Alternative loan route |

|---|---|---|

| Speed | Slower, more review layers | Faster decisions and funding |

| Documentation | Heavier paperwork and historical review | Often more operational-data driven |

| Approval fit | Better for strong collateral and conventional profiles | Better for cash-flow-driven or nontraditional profiles |

| Cost | Often lower if you qualify and can wait | Usually higher because speed and flexibility cost money |

| Repayment shape | More predictable monthly structure | Can be daily, weekly, revenue-linked, or short-duration |

My recommendation

Use a traditional lender when the need is planned, the project has a long payoff period, and your file is strong enough to survive a slower process. Expansion with runway, owner-occupied real estate, major equipment, and refinance situations often belong here.

Use alternative business loans when the timing is tight, the return on capital is immediate, or the business has strong cash flow but weak collateral presentation. Seasonal inventory, short working-capital gaps, bridge financing, invoice acceleration, and urgent repair or payroll situations fit this lane.

Cheap money that arrives too late isn't cheap. It's useless.

The mistake is using each product for the wrong job. I've seen owners force a bank request into a week-long emergency and lose the contract. I've also seen owners take expensive daily-pay financing for a project that easily could've waited for lower-cost capital. Both are avoidable.

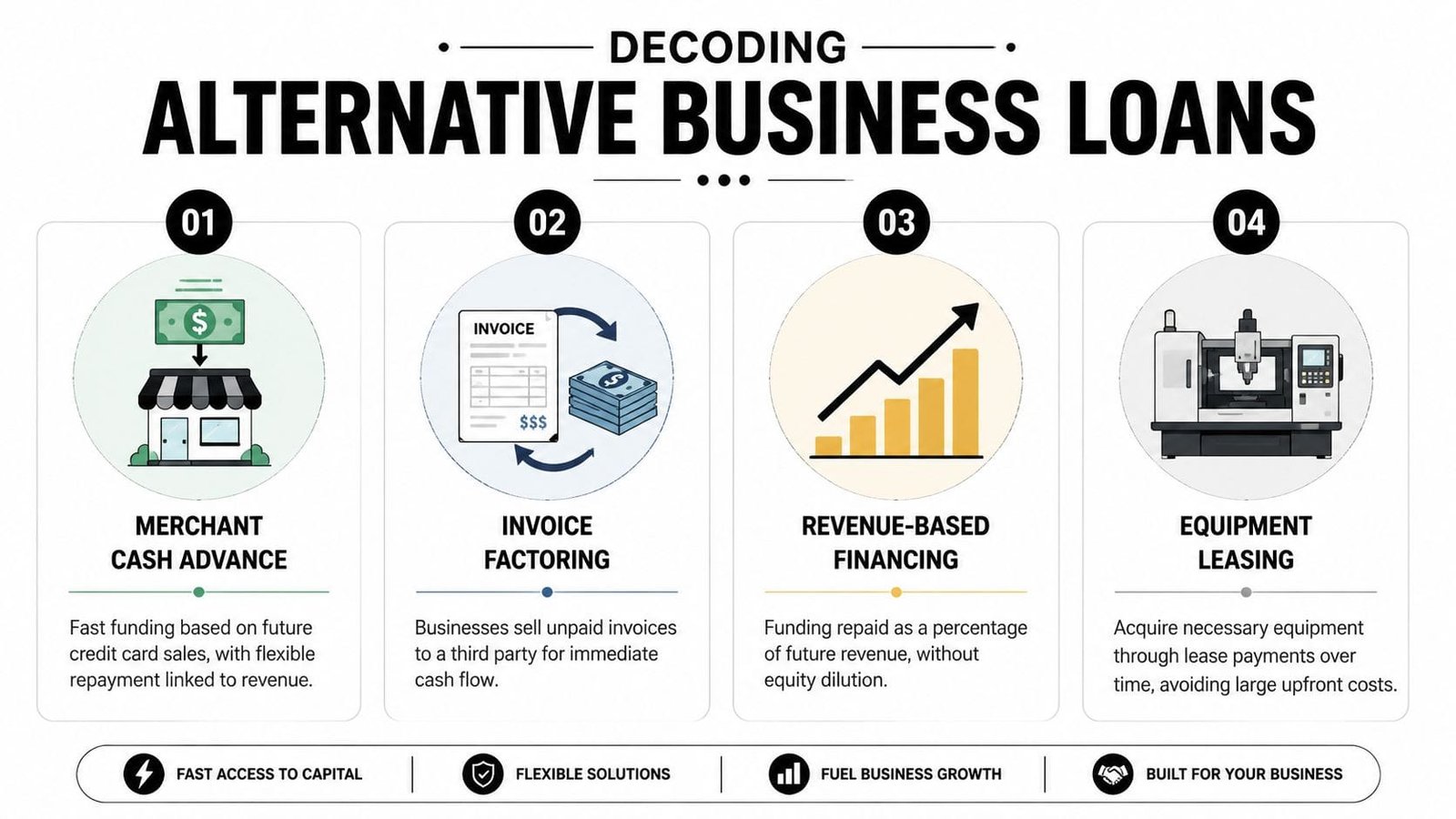

Decoding The Types of Alternative Business Loans

Alternative business loans get lumped together, but the products behave very differently. A merchant cash advance is not the same as invoice financing. A short-term loan is not the same as equipment leasing. If you don't separate them, you'll compare offers badly.

Merchant cash advance

An MCA is an advance against future sales, usually repaid through frequent withdrawals or a holdback tied to card or revenue activity.

This fits businesses with strong sales volume and urgent needs. Restaurants, retailers, and hospitality operators use it when speed matters more than elegance.

It's usually the fastest product in the stack. It's also one of the easiest to misuse because the payment pressure shows up quickly.

Short-term loan

A short-term business loan is a lump sum repaid over a shorter schedule than a conventional term loan. Think of it as a sprint loan, not a marathon loan.

It works for inventory purchases, temporary working-capital gaps, quick marketing pushes, or a bridge between expense and receivable. It's cleaner than an MCA if the payment schedule is manageable and the fee structure is transparent.

If you need a simple overview of product structures in this category, this guide to short-term business financing can help you sort the options.

Business line of credit

A line of credit gives you access to capital as needed rather than forcing you to take one large lump sum. That matters if your need is uneven.

Use it for recurring but unpredictable gaps. Payroll timing, smaller inventory buys, contract mobilization, and periodic vendor pressure fit well here.

The biggest advantage is control. You borrow what you need, when you need it. The downside is that some owners treat available credit like free cash and keep the balance revolving longer than planned.

A line of credit is a working-capital tool. It is not a license to cover a broken business model.

Invoice financing or factoring

This is the best product for companies that are profitable on paper but slow to collect cash. You've done the work, issued the invoice, and now you're waiting.

Invoice financing is basically a paycheck advance on your receivables. Factoring can also involve the finance company purchasing invoices and collecting from the customer directly.

This works especially well for B2B firms, staffing companies, distributors, and service businesses with strong accounts receivable. It's often smarter than taking a broad cash-flow product if your problem is specifically tied to collections timing.

Equipment financing or leasing

When the equipment itself has value and drives revenue, finance the asset with the asset. Don't use a high-pressure working-capital product for a long-life machine if you can avoid it.

Equipment financing is best when the purchase is specific, trackable, and productive. Leasing can preserve cash and reduce the upfront burden.

For contractors, manufacturers, medical practices, logistics operators, and certain restaurant concepts, this is often the most rational path because the funding structure matches the use of proceeds.

Alternative Business Loan Comparison

| Loan Type | Best For | Typical Speed | Cost Structure |

|---|---|---|---|

| Merchant cash advance | Urgent revenue-driven cash needs | Very fast | Advance fee or factor-style pricing with frequent repayment |

| Short-term loan | Short-duration working capital | Fast | Fixed-fee or interest-based repayment over a short schedule |

| Business line of credit | Repeating cash flow gaps | Fast to moderate | Pay for what you draw, terms vary by lender |

| Invoice financing | Slow-paying B2B receivables | Fast once invoices are verified | Fee tied to invoices advanced or purchased |

| Equipment financing | Revenue-producing equipment | Moderate | Payments tied to the asset and financing term |

Choosing Your Funding Path A Framework for CEOs

You don't need more product names. You need a decision filter.

Start with urgency, not optimism

Owners routinely understate urgency and overstate affordability. Fix that first.

Ask these four questions:

How fast do I need funds?

If the answer is days, you're already narrowing the field. Don't waste a week pretending a slow lender will suddenly move quickly.What is the money for?

A payroll bridge, an equipment purchase, and invoice acceleration should not use the same product.How stable is the revenue behind repayment?

Daily-payment products are dangerous if revenue is lumpy.What happens if I wait?

If waiting costs you margin, customers, or a hard deadline, speed has value. If waiting costs nothing, shop for lower-cost structure.

Here's the blunt version. If the need is urgent and temporary, use a temporary product. If the need is strategic and long-term, push for a longer-term structure even if it takes more work.

Know how lenders will view your business

Established companies are often evaluated on more than a personal credit score. Underwriters may look at company size, margins, recurring revenue quality, and cash generation. An industry breakdown of direct lending segments borrowers by EBITDA, with core middle market defined as $30M to $50M EBITDA and upper middle market at $50M to $100M EBITDA. The same piece notes that some asset-light businesses can be underwritten against recurring revenue, and it cites a $45M facility structured primarily on ARR, according to ABF Journal's review of direct lending moving down market.

That matters if you run a services, SaaS, or digitally enabled business with strong revenue but limited hard collateral. You may have more options than you think.

For a closer look at how operators think through lender fit and deal timing, this short video is useful:

My framework in plain English

- Urgent and small enough to absorb premium pricing: consider line of credit, short-term loan, or MCA only if the payoff is immediate.

- Receivables are strong but cash is delayed: invoice financing is usually cleaner than broad unsecured debt.

- Asset purchase with clear resale or productive value: equipment financing or leasing belongs at the top of the list.

- Established business with stable operations and time to underwrite: push toward SBA-backed or more conventional structures first.

Borrow based on the use of funds, not the ad copy that got your attention.

Your Step-by-Step Alternative Loan Application Guide

The application process for alternative business loans is simpler than most owners expect. The actual effort is not filling out the form. The primary task is presenting a clean story.

Get your file tight before you apply

Start with documents that prove identity, revenue flow, and business control. In practice, that usually means recent bank activity, business formation details, owner identification, and basic information on use of funds. Some products will ask for more. Some will ask for less.

If you don't have traditional statements organized, there are still paths. This guide on business loan options without bank statements shows how some lenders approach alternative documentation.

A practical checklist:

- Explain the use of funds clearly: “inventory for signed seasonal demand” is better than “working capital.”

- Match the request to the need: Don't ask for a broad facility if you really need one equipment purchase.

- Clean up obvious file issues: inconsistent legal entity names, stale licenses, and missing ownership details slow down deals.

- Know your average deposit behavior: lenders care about operating rhythm, not just headline revenue.

Compare the offer, not just the approval

A fast approval can make people reckless. Don't celebrate too early.

Review these items before you sign:

- Repayment frequency: Daily and weekly drafts change your cash cushion more than many owners expect.

- Total repayment obligation: What do you pay back if everything goes according to schedule?

- Prepayment treatment: Some products reward early payoff. Others don't.

- Collateral or guarantees: Understand what support the lender requires if revenue dips.

Close cleanly

Once you accept terms, funding can move quickly if your bank connection, business details, and signatures are clean. Delays at this stage are usually self-inflicted. Wrong account information, unsigned forms, and last-minute ownership questions kill momentum.

If you're applying through a marketplace platform, keep communication centralized. Business Loan Warrior, for example, uses a single no-fee application, lets borrowers check pre-approval without affecting credit, and provides a dashboard to track approvals and repayments. That kind of setup is useful when you want multiple options without restarting the process with each lender.

The True Cost of Speed Common Pitfalls to Avoid

This is where owners get hurt. Not in the approval. In the math.

Fast funding always sounds manageable at the top line. The payment amount looks small enough. The draft schedule seems fine. Then the withdrawals start hitting daily or weekly, and cash gets tighter than expected.

One summary of alternative lending warns that nonbank products usually carry higher rates and fees, and it highlights a major structural difference: many require daily or weekly payments, which can put real pressure on operating cash flow, as noted in Swoop Funding's overview of alternative business lending.

How to calculate all-in cost

You don't need a perfect finance model. You need disciplined questions.

Use this checklist on every offer:

How much cash am I receiving?

Not the approved amount. The net amount hitting the account.How much total money am I required to repay?

Include every fee, every fixed charge, every required deduction.How often is repayment collected?

Monthly feels very different from daily, even when the total payback looks similar.Over what real period will this be repaid?

Short duration increases the annualized cost dramatically.

If you're looking at factor-style pricing, the core issue is simple. A factor rate is not the same thing as an annual interest rate. It tells you the fixed multiple applied to the advance, but it does not tell you what the financing costs on an annualized basis, especially when repayment starts immediately and happens frequently.

If a lender won't clearly show you total payback, repayment frequency, and whether early payoff reduces cost, keep shopping.

Mistakes that wreck cash flow

The first mistake is focusing only on approval speed. The second is ignoring repayment rhythm.

Watch for these problems:

- Daily draft compression: Even profitable businesses can feel squeezed when cash leaves the account every business day.

- Loan stacking: Taking a second advance before the first one is digested is one of the fastest ways to damage liquidity.

- Mismatch between product and purpose: Don't finance a long-life asset with a high-pressure short-term product unless you have no better option.

- Fee blindness: Owners often compare proceeds, not total repayment.

- False prepayment assumptions: Some products don't get meaningfully cheaper just because you pay them off early.

For established companies, the smartest move is often boring. Compare the all-in cost of the fast option against slower structures that fit the same need. If the use of funds can support waiting, premium-speed capital should be your backup plan, not your default move.

Your Top Alternative Lending Questions Answered

Can I get an alternative loan with weak personal credit

Possibly, yes. Many alternative lenders care more about business performance than a clean personal credit narrative. That doesn't mean credit is irrelevant. It means deposits, receivables, customer concentration, time in business, and repayment capacity can carry more weight than they would at a traditional bank.

Will applying hurt my credit

Sometimes lenders start with a soft review and only move to a hard inquiry later in the process. Ask before you apply. Don't assume. A serious lender should be able to tell you exactly when and how credit gets checked.

Can I repay early

Maybe. But “yes” is not enough. Ask whether early payoff reduces your total cost. Some products are front-loaded. Others have fixed-fee economics that don't reward early repayment much. Get the answer in writing.

How do lenders verify revenue without endless paperwork

They often use business bank activity, processor data, invoices, platform history, and other operating signals instead of relying entirely on tax returns and hard collateral. That's one reason alternative business loans can move faster. The underwriting is still real. It's just based on more current business behavior.

What's the biggest mistake borrowers make

They chase approval instead of fit.

If you borrow against future sales to solve a margin problem, you've added pressure without fixing the business. If you use invoice financing to smooth timing on strong receivables, that can be a smart move. Product fit matters more than lender branding.

Which option should an established business try first

If you have stable revenue, decent records, and a little time, start with the lowest-cost structure that matches the use of funds. For many established firms, that means checking conventional or SBA-backed paths before jumping into premium-speed products. If timing is tight, then move down the speed ladder with your eyes open.

Good financing gives the business room to operate. Bad financing takes oxygen out of the room.

Secure Your Best Offer with Business Loan Warrior

Alternative business loans can solve real problems fast. They can also create new ones if you don't match the product to the purpose, calculate the all-in cost, and pressure-test the repayment schedule against your actual cash flow.

My advice is simple. Treat financing like an operating decision, not an emotional one. If the money is for a short-term gap, use a short-term structure. If the money supports a longer asset or strategic project, keep pushing for a structure that gives the business breathing room. Speed has value, but only when it doesn't drain margin and flexibility later.

If you want to compare options without filling out separate applications all over the market, Business Loan Warrior lets you check pre-approval through a single no-fee application, review funding paths without an automatic credit hit, and sort through offers with both technology and human support.