You're probably seeing some version of this right now. Sales look solid, your accountant says the business is profitable, and yet cash still feels tight. Then a lender asks for your last two or three years of financials, starts drilling into expense categories, and suddenly your “good” P&L doesn't feel good at all.

That disconnect is where a lot of owners get stuck. They've been using the profit and loss statement as a tax document or a rearview mirror. Lenders use it differently. They use it to decide whether your numbers are consistent, whether your cash generation is believable, and whether your business can carry new debt without strain.

Managing a P&L well isn't just about knowing whether you made money last month. It's about turning your financials into a document an underwriter can trust. If you want working capital, equipment financing, an SBA loan, or expansion funding, that trust matters as much as the profit figure itself.

Table of Contents

- Beyond Profitability Your P&L's Real Job

- Decoding Your P&L Line by Line

- The Repeatable Monthly Close Process

- From Cost Cutting to Strategic Profit Growth

- Forecasting and Planning for What's Next

- Translating Your P&L for Lenders and Investors

Beyond Profitability Your P&L's Real Job

A healthy-looking P&L can still fail you when you need capital.

I've seen businesses show profit on paper while the owner can't explain why the line of credit request stalled. Usually the issue isn't that the business is weak. It's that the financial story is incomplete. Revenue may include one-time spikes that won't repeat. Expenses may be lumped into vague categories. Inventory, receivables, or debt payments may be swallowing cash faster than the income statement suggests.

That's why managing a P&L has to go beyond bookkeeping. Your P&L is part performance report, part credibility test. A lender reads it to answer practical questions. Are margins stable? Are expenses classified consistently? Does management understand what drives profitability? Can these numbers be tied back to bank activity and supporting records?

A lender isn't looking for perfect numbers. They're looking for numbers they can follow, verify, and believe.

This standard didn't come out of nowhere. The Sarbanes-Oxley Act of 2002 required senior executives at public companies to personally certify the accuracy of P&L reporting, which helped establish the broader expectation that profit reporting is a governance issue, not just an accounting exercise, as explained in Rippling's overview of how Sarbanes-Oxley changed P&L accountability.

Small businesses aren't bound by that law in the same way, but lenders still operate in the world it shaped. They expect financial rigor. They expect consistency. They expect an owner to know the difference between being profitable and being fundable.

The real shift

If you're serious about growth, stop asking only, “Did we make money?”

Start asking:

- Can I defend every major line item?

- Can I explain why profit and cash differ this month?

- Would an outside underwriter trust this report without a long cleanup project?

That's the job of your P&L. It has to help you run the business, yes. But when capital is on the line, it also has to prove the business deserves funding.

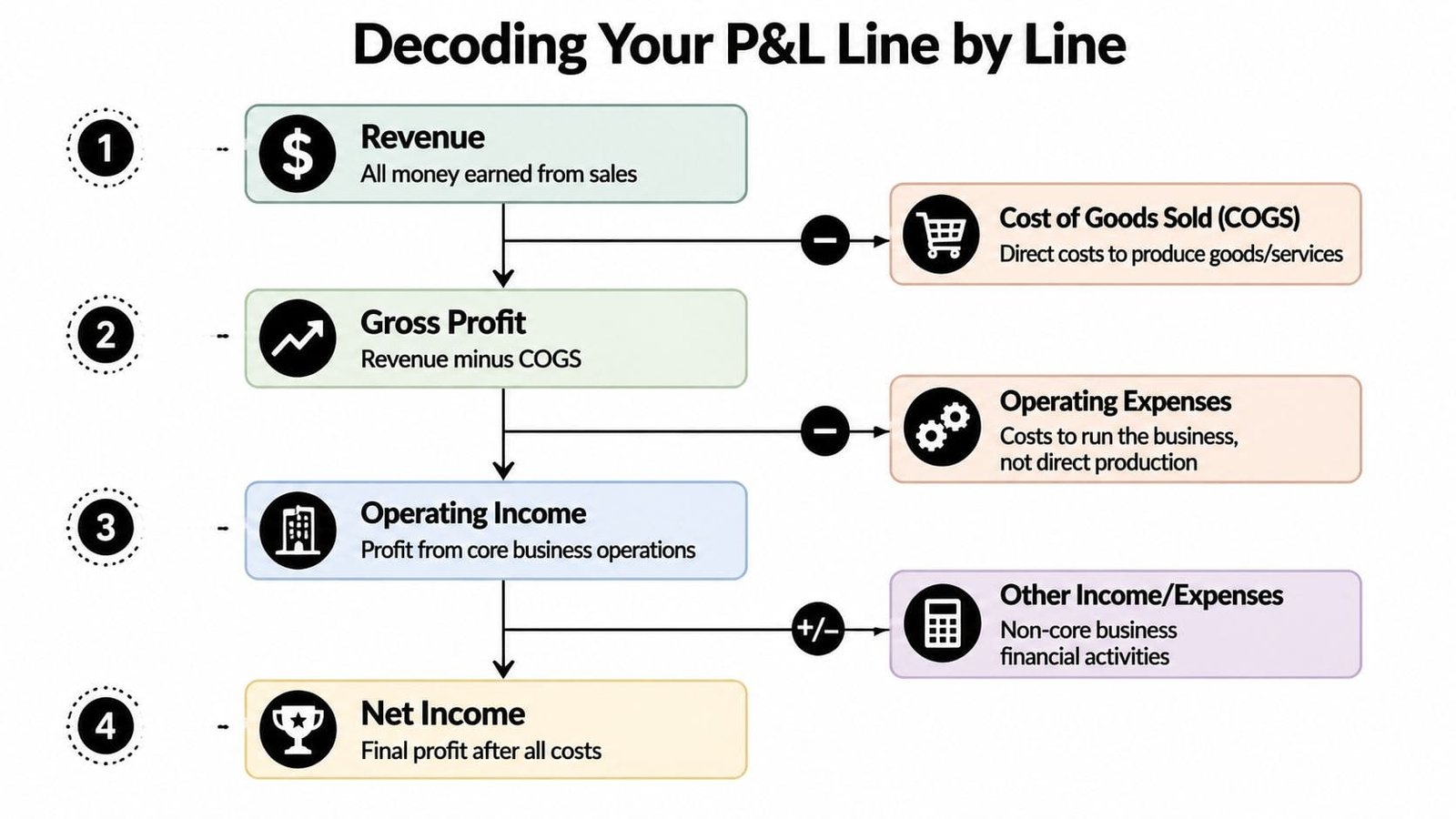

Decoding Your P&L Line by Line

Most owners don't need a textbook definition of a P&L. They need to know what each line tells a lender, investor, or buyer about how the company runs.

What each section is really saying

Start at the top.

| P&L line | What it means in practice | What a lender notices |

|---|---|---|

| Revenue | All sales recognized in the period | Whether sales are recurring, concentrated, or erratic |

| COGS | Direct costs tied to delivering what you sold | Whether your gross margin is reliable |

| Gross Profit | Money left after direct delivery cost | Whether the core model works before overhead |

| Operating Expenses | The cost to run the company | Whether spending is controlled and explainable |

| Operating Income | Profit from normal operations | Whether the business works before financing effects |

| Other Income and Expenses | Non-core items like interest or unusual gains/losses | Whether non-operating items are masking weakness |

| Net Income | Final accounting profit | Whether the profit is durable and useful for debt repayment |

Revenue isn't just “sales.” It's the top-line claim you're making about your business. If that number includes one-off jobs, project overages, or unusual customer activity, a lender will want to know. Predictable revenue gets treated differently from noisy revenue.

COGS is where many stories break. If you manufacture, distribute, install, or deliver a service with direct labor, materials, or fulfillment costs, COGS should reflect that. Gross profit then tells you whether the actual work you sell produces enough margin to support the business around it.

For owners in hospitality, retail, or foodservice, industry-specific examples help. A practical reference is this walkthrough of a profit and loss statement for restaurants, which shows how category detail affects decision-making.

Later in the section, it helps to hear the concepts explained out loud as well:

Where classification mistakes cause damage

The biggest mistake I see is treating expense categories as if they're flexible. They aren't, at least not if you want clean financials.

A direct production cost pushed into operating expenses can make your gross margin look healthier than it is. A financing-related cost buried in general overhead can hide debt pressure. A vehicle purchase recorded as an ordinary expense instead of being handled properly can distort profitability and make your statements harder for a lender to reconcile.

Practical rule: If you can't explain why an item sits in a specific line, don't assume the classification is harmless. Misclassification changes the story the P&L tells.

A good P&L also separates owner-specific spending from true operating cost. Underwriters often adjust for discretionary expenses, but they need to see them clearly first. If everything is buried in “miscellaneous,” you force the lender to guess. Guessing slows decisions.

How to read trends instead of snapshots

One month in isolation doesn't tell you enough. You need two lenses.

Vertical analysis shows each line item as a percentage of sales. Horizontal analysis shows how those items change across periods. In small businesses with $20M to $50M in sales, institutionalizing both approaches increases the success rate for sustainable profitability by 35%, according to the verified data provided for this article.

That matters because it turns the P&L from a list into an operating dashboard. If payroll as a share of sales keeps drifting up, that means something. If gross margin dips each quarter, that means something else. If rent is stable but software spend keeps climbing, you've found a conversation worth having.

Use these questions every month:

- What changed as a percentage of revenue

- What changed versus last month and the same month last year

- Which changes are strategic and which ones are drift

- Can I explain the cause in one sentence

That last question is the test. If you can answer it cleanly, your P&L is becoming useful.

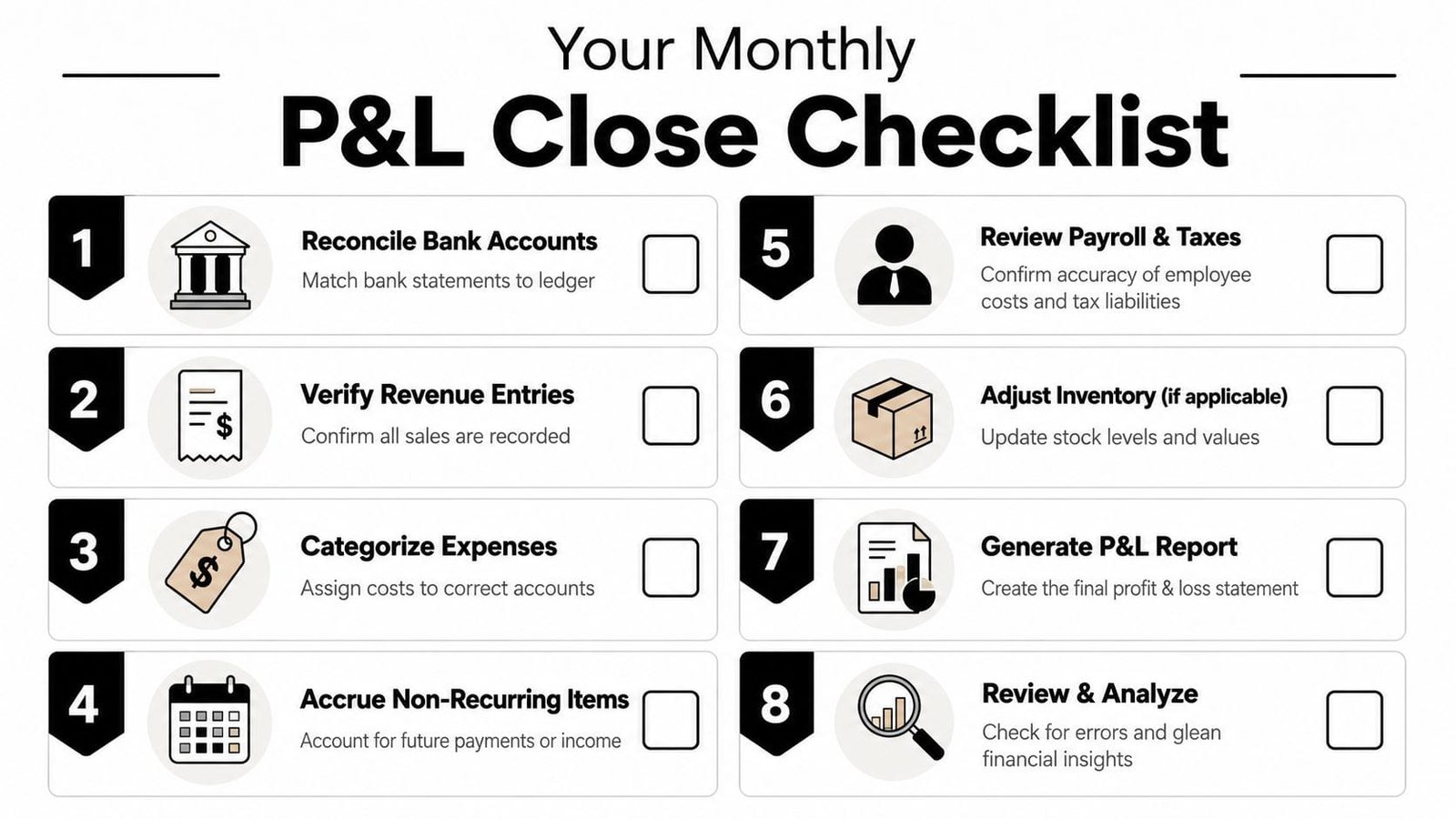

The Repeatable Monthly Close Process

Lender-ready financials come from discipline, not heroics at year-end.

If your books only get cleaned up when taxes are due or when a loan application is pending, you're always going to be behind. A reliable monthly close creates a clean historical record. It gives you reports you can trust now, not after a scramble through receipts, payroll reports, and old bank statements.

What a dependable close looks like

The process doesn't need to be glamorous. It needs to be repeatable.

Reconcile cash first. Match every bank account, credit card account, and loan statement to the general ledger. If cash doesn't tie, the rest of the P&L is suspect.

Lock down revenue. Confirm invoices, deposits, merchant processor settlements, and any credits or refunds. Revenue is the first line underwriters test because it drives every ratio below it.

Categorize expenses cleanly. Push every transaction into the right bucket while the details are still fresh. Don't let suspense accounts and uncategorized expenses pile up.

Book accrued items. Payroll that crosses month-end, vendor bills received late, commissions earned but not yet paid, and taxes owed all need to land in the right period.

After the mechanics are done, generate the draft P&L and compare it with the prior month and the same month last year. The comparison matters more than most owners realize. It exposes spikes, omissions, duplicates, and timing issues quickly.

The review that catches lender problems early

Owners often stop too soon. They produce the report, glance at net income, and move on.

Don't do that. Review the report line by line as an operator. Ask whether each major variance has a business reason behind it. If advertising jumped, was there a campaign launch? If repairs spiked, was there a facility issue? If subcontractor cost dropped, did labor shift in-house?

A simple variance log makes this much easier. If you want a practical template, this guide on how to build an expense variance log that speeds up lending decisions is worth using as part of your close.

Close the books like someone else will read them tomorrow, because eventually someone will.

A strong monthly close usually includes these final checks:

- Owner review: The owner or finance lead signs off on unusual items.

- Supporting files: Bank recs, payroll reports, debt statements, and major invoices are stored where they can be retrieved fast.

- Consistency check: Categories match prior periods unless there's a deliberate reason to change them.

- Narrative note: One short explanation for any unusual month. That note becomes valuable during underwriting.

The benefit is simple. When a lender asks for trailing financials, you aren't creating a story under pressure. You already have one.

From Cost Cutting to Strategic Profit Growth

Many owners hear “manage the P&L” and immediately think “cut expenses.” That's too crude.

The job isn't to spend less at all costs. The job is to stop spending on things that don't move revenue, margin, efficiency, or capacity. That requires judgment. Some costs weaken the business. Others create future earnings and should be protected.

Cut bad cost not productive cost

A common pitfall in P&L management is failing to test expenses against ROI. That problem leads to an average 15% waste in operational spend, often through redundant software or non-essential vendor contracts, according to the verified data provided for this article.

That number tracks with what shows up in real businesses. The waste usually isn't one giant mistake. It's accumulation. Multiple software tools doing overlapping work. Agency retainers no one reviews. Service contracts renewing out of habit. Freight or vendor fees that haven't been renegotiated in years.

Use a short decision table for major expense categories:

| Expense type | Keep | Reduce | Eliminate |

|---|---|---|---|

| Produces measurable revenue | Yes | Only if efficiency drops | Rarely |

| Protects capacity or quality | Usually | Sometimes | Carefully |

| Administrative but necessary | Yes, with controls | Often | If duplicated |

| No clear owner or outcome | Question it | Likely | Often |

Owners often get into trouble by cutting sales support, customer service, or maintenance because those lines look discretionary. Then revenue slips, retention softens, or equipment downtime rises. The P&L improves briefly and then worsens.

Use the P&L to defend the right spending

The better move is to separate value-destroying cost from value-creating investment.

If a software platform automates billing and cuts manual rework, that may deserve a place. If marketing spend produces qualified leads and repeatable payback, defend it with confidence. If a piece of equipment reduces cycle time or labor bottlenecks, the cost may improve both margin and lender confidence because it strengthens operating consistency.

Good cost should survive scrutiny. Bad cost disappears when someone asks what return it creates.

This is also where pricing and service mix belong in the discussion. A well-managed P&L can show you whether your issue is spending at all. Sometimes the deeper issue is underpricing, poor mix, or low-margin work taking up too much capacity.

If you want a margin-focused lens for thinking through these decisions, this resource on how to boost profitability offers useful framing.

A practical monthly review should include questions like these:

- Which expense categories directly support revenue generation

- Which costs protect quality or fulfillment

- Which subscriptions, vendors, or contracts no one owns

- Which products, customers, or jobs produce the weakest gross profit

- Where are we funding complexity without getting paid for it

Owners who answer those questions consistently don't just cut cost. They improve the economic shape of the business.

Forecasting and Planning for What's Next

A historical P&L is useful. A forward-looking one is bankable.

Lenders want evidence that management understands what's coming next, not just what already happened. That means taking the patterns in your P&L and projecting them into a rolling forecast you can update as conditions change.

Build a rolling view not a frozen budget

Static annual budgets age badly. Sales shifts, supplier pricing changes, labor pressure shows up, and suddenly the budget becomes a document everyone ignores.

A rolling forecast works better because it updates with real conditions. Start with your sales pipeline, backlog, renewals, seasonality, and customer concentration. Then estimate the direct costs and operating expenses required to support that revenue. Keep the structure simple enough that you'll maintain it.

The most useful forecast isn't the most elaborate one. It's the one your team updates regularly and uses to make decisions.

A good operating forecast usually includes:

- Revenue assumptions: New sales, repeat business, seasonality, and one-time projects

- Direct cost assumptions: Materials, direct labor, fulfillment, or subcontracting

- Overhead assumptions: Payroll, occupancy, software, insurance, and debt obligations

- Cash timing notes: Receivable collection patterns, inventory purchases, and large vendor payments

If you want a practical companion to this process, this guide on how to build a cash flow forecast that empowers your loan strategy is a strong next step because it connects profit planning to liquidity planning.

Run scenarios before the bank asks

Forecasting becomes much more useful when you pressure-test it.

Create three versions of your P&L outlook. A likely case, a downside case, and an upside case. Don't make them theoretical. Tie them to actual business levers. A slower close rate. A customer delay. A supplier increase. A hiring pause. A new contract starting earlier than expected.

The owner who has already modeled a tough quarter gives lenders more confidence than the owner who says, “We'll figure it out.”

You don't need a dense financial model to do this well. A plain spreadsheet is often enough if your assumptions are clear. The discipline matters more than the tool.

Here's a simple scenario framework:

| Scenario | Revenue view | Cost response | Management action |

|---|---|---|---|

| Likely case | Current pipeline converts as expected | Maintain planned spend | Execute normally |

| Downside case | Sales soften or customer payments slow | Delay non-critical hiring and discretionary spend | Protect cash and monitor weekly |

| Upside case | Sales land faster or volume expands | Add capacity carefully | Fund growth without creating chaos |

This exercise also sharpens how you speak with lenders. Instead of saying, “We think things will be fine,” you can say, “If volume softens, here's how we'll adjust labor, purchasing, and overhead.” That's a very different conversation.

Translating Your P&L for Lenders and Investors

At this stage, many otherwise strong businesses lose momentum. They submit profitable financials, but the package still doesn't support approval.

The first reason is document quality. Over 40% of SBA loan denials stem from financial statement inadequacies like unverified or inconsistent P&L data, based on the verified data cited from the U.S. SBA Office of Loan Guarantee 2025 Annual Report. The second reason is the cash flow gap. Another 32% of rejections for other small business financing are due to a disconnect between reported P&L profit and actual operating cash flow, based on the verified data cited from NFIB's Small Business Financing Barriers 2025.

Why profit alone doesn't get deals approved

This is the cash flow versus P&L paradox.

Your income statement can show net income while the business still struggles to make debt payments on time. That happens when receivables build too fast, inventory absorbs cash, debt service rises, or profit is driven by activity that doesn't convert cleanly into operating cash.

A lender will usually compare your P&L with bank statements, balance sheet movement, and debt obligations. They're trying to answer one basic question. Does this business generate enough dependable cash to support another payment?

That's where DSCR, or Debt Service Coverage Ratio, comes in. In plain English, it asks whether the business generates enough income to cover its debt payments with room to spare. If your P&L is inconsistent, if expenses are misclassified, or if profit depends on one-time items, that ratio becomes weaker or harder to defend.

For owners preparing equity or debt discussions beyond traditional bank channels, a structured process to streamline your investor search can also help you present the right financial narrative to the right audience.

How to make your package lender ready

A lender-ready package does not need to be fancy. It needs to be coherent.

Use this checklist:

- Clean historical P&Ls: Make sure periods are closed, classifications are consistent, and unusual items are identified.

- Matching balance sheets: Your income statement has to make sense alongside receivables, payables, inventory, and debt.

- Cash flow explanation: Be ready to explain why profitable months didn't always produce cash.

- Debt schedule: Show current debt obligations clearly.

- Owner adjustments: Identify discretionary or non-recurring expenses that may matter in underwriting.

- Support for net income: If you need a clear refresher on the bottom line itself, this guide on how to find net income is useful.

One more point matters here. Don't send a lender a report you haven't read aloud to yourself. If a line item would prompt a question from you, it will prompt one from them too.

The best financing package answers the underwriter's next question before they have to ask it.

That's the capital-first mindset. You're not managing a P&L only to measure profit. You're managing it so an outside party can trust your profit, reconcile it to cash, and see a business that's ready to carry capital responsibly.

If you want funding without the usual back-and-forth, Business Loan Warrior helps small businesses check options through a single no-fee application, connect financial accounts securely, and move from underwriting questions to appropriate offers faster. If your goal is to turn messy financials into a lender-ready package for working capital, equipment, expansion, or SBA financing, it's a practical place to start.