You need cash now. Payroll hits Friday, a supplier wants payment before release, or a project is moving faster than receivables. So you search for line of credit same day funding and find pages that make it sound simple: apply in minutes, get approved instantly, funded today.

That promise is usually true only in a narrow sense. Fast decisions are real. Fast funding is real in some cases. But for a substantial business line of credit, especially for an established company with real revenue, multiple owners, and meaningful bank activity, same-day funding is the exception, not the operating standard.

The fastest path isn't chasing the loudest marketing claim. It's knowing which products can move quickly, which ones only sound fast, and what underwriters need in front of them before they can release funds.

Table of Contents

- The Reality of Same Day Business Funding

- Your Fast-Funding Eligibility Checklist

- The Step-by-Step Application Playbook

- A Realistic Funding Timeline

- Funding Red Flags and Safer Alternatives

- Your Path to Fast and Responsible Capital

The Reality of Same Day Business Funding

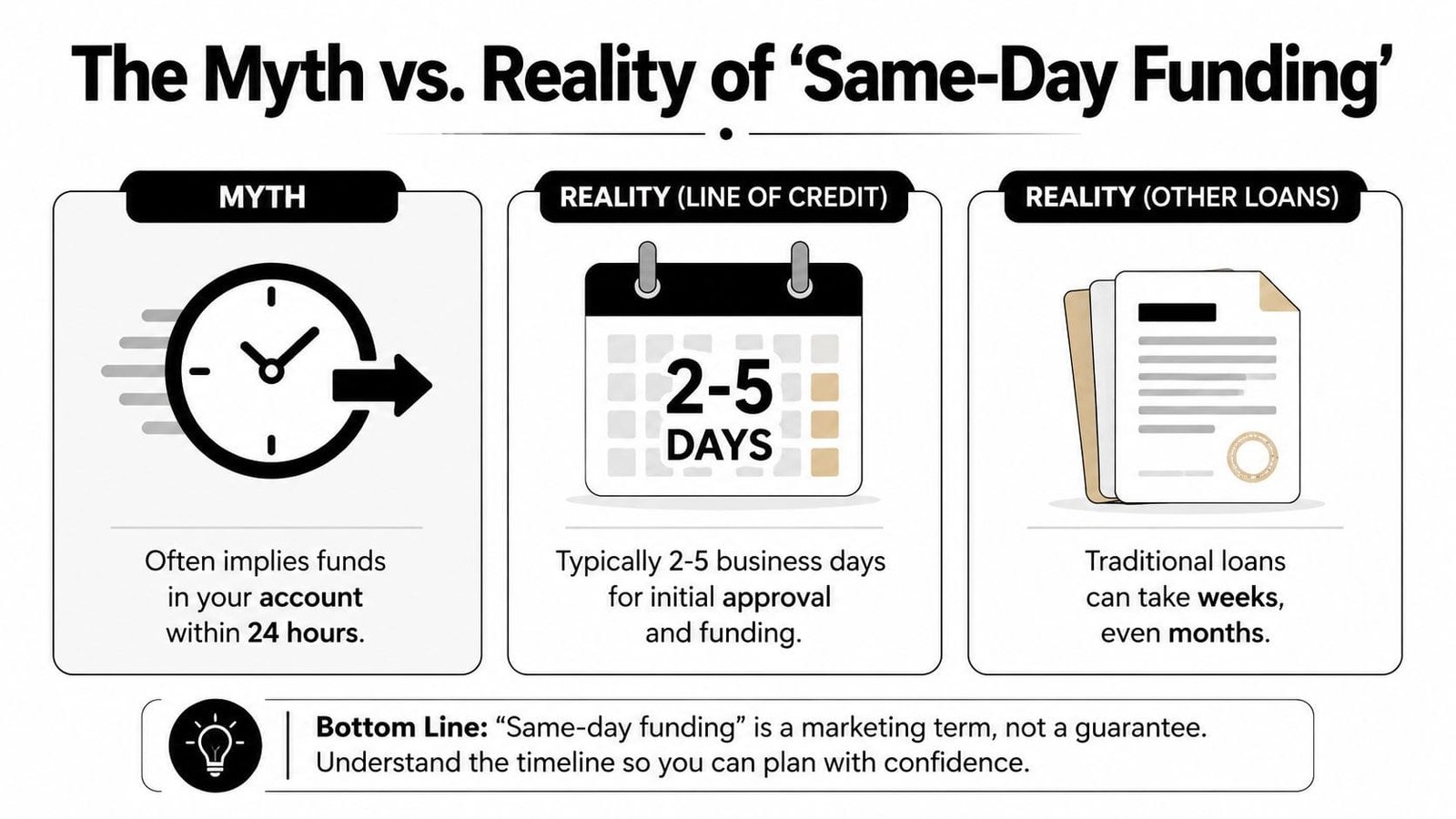

If you're looking for true business working capital, start with the uncomfortable truth: most “same-day funding” language borrows credibility from the personal loan world, not the commercial lending world.

Data shows 92% of business loan approvals take 3–7 days because lenders still need revenue verification, tax review, and bank statement analysis, while same-day personal loans cap at $8,000 and target sub-580 FICO borrowers, according to LendingTree's review of bad-credit personal loan options. That distinction matters. A personal emergency loan and a business line for operating capital are not underwritten the same way.

What same-day usually means in marketing

Most lenders use “same-day” to describe one of four things:

- A fast pre-qualification. You answer a few questions and get a preliminary signal.

- A same-day approval decision. The lender says yes, conditionally or fully.

- A same-day draw. This only applies if the line already exists and you're drawing against an approved facility.

- A same-day transfer window. Funds move only if approval, signing, and bank cutoffs all line up.

That isn't wordplay. It's the difference between solving a cash crunch and learning at 4:40 p.m. that the money won't post until tomorrow.

Why real business lines take longer

A real business line of credit has to answer harder questions than a personal loan. Underwriters need to know whether the business itself can support repayment, not just whether the owner can.

They review things like:

| Review area | Why it slows funding |

|---|---|

| Business revenue | Lenders need to see stability, not just one strong deposit |

| Bank statement activity | Returned payments, volatility, and low balances trigger deeper review |

| Ownership structure | Multiple owners or layered entities require documentation |

| Tax and compliance checks | These can delay even strong files if records don't match |

| Use of funds | Urgent need is fine. Unclear need is not |

Practical rule: If the lender can approve you without understanding your business cash flow, you're probably not being offered a true business line of credit.

For larger operating companies, the “same-day” story gets even weaker. Businesses above a certain size generate more transactions, more documentation, and more diligence. That's not a flaw in the system. That's the system doing its job.

The good news is that fast funding is still possible. You just need to aim for the fastest realistic outcome: a clean file, a lender that uses automation well, and a funding path that fits the actual urgency.

Your Fast-Funding Eligibility Checklist

When a file moves quickly, it's rarely because the borrower got lucky. It moves because the business was easy to verify.

Underwriters don't need perfection. They need clarity. The faster you remove ambiguity, the faster a line of credit can move from application to offer.

What lenders want to see immediately

Before you apply, check these areas first:

- Business identity is consistent. Your legal business name, address, ownership details, and tax identifiers should match across bank records, formation documents, and the application.

- Business bank activity looks usable. A lender wants statements that show real operating activity, not an account that only occasionally receives transfers.

- Revenue pattern is understandable. Seasonal businesses can still qualify, but if deposits swing sharply, expect questions unless you explain the pattern upfront.

- No unresolved document conflicts. If one statement shows an old address and another shows a new one, fix it before applying.

- Authorized signer access is ready. Deals stall when the person applying can't sign final agreements or provide missing documents quickly.

What usually causes preventable delays

Most funding delays don't happen because the business is weak. They happen because the file arrives half-built.

Watch for these issues:

- Unreadable statements. Cropped screenshots, partial PDFs, or missing pages force manual follow-up.

- Mismatched ownership percentages. If the application says one thing and formation records say another, underwriting pauses.

- Unexplained negative events. Overdrafts, sudden revenue drops, or unusual transfers aren't automatic declines. Silence about them is the problem.

- Applying too late in the day. Even strong approvals can miss disbursement windows if signing happens after bank cutoff times.

- Submitting while you're still gathering documents. That's one of the most common self-inflicted delays.

A fast application is not the same as a fundable application. The clock starts when your file is complete, not when you click submit.

Your pre-application file stack

If you want the fastest possible decision, prepare a lender-ready package before you begin:

- Current business bank statements

- A simple ownership breakdown

- Basic business formation records

- Recent internal financials if available

- A short written use-of-funds explanation

- Direct contact info for the person who can sign and answer follow-up questions

That last item matters more than most CEOs expect. Good files still hit friction when an underwriter has one open question and nobody responds for half a day.

How to pressure-test your readiness

Use this quick self-check:

| Question | If the answer is no |

|---|---|

| Can you upload complete documents in one sitting? | Expect manual follow-up |

| Do all business details match across records? | Expect compliance review |

| Can you explain recent cash flow swings clearly? | Expect underwriting questions |

| Can an authorized signer respond quickly today? | Funding may slip |

| Do you know whether you need a line, loan, or bridge product? | You may apply for the wrong thing |

If you want to see how a lender screens for speed before a full application, review a line of credit pre-approval workflow and compare it against your own file readiness.

The businesses that get funded fastest usually do one thing well. They make it easy for the lender to say yes without guessing.

The Step-by-Step Application Playbook

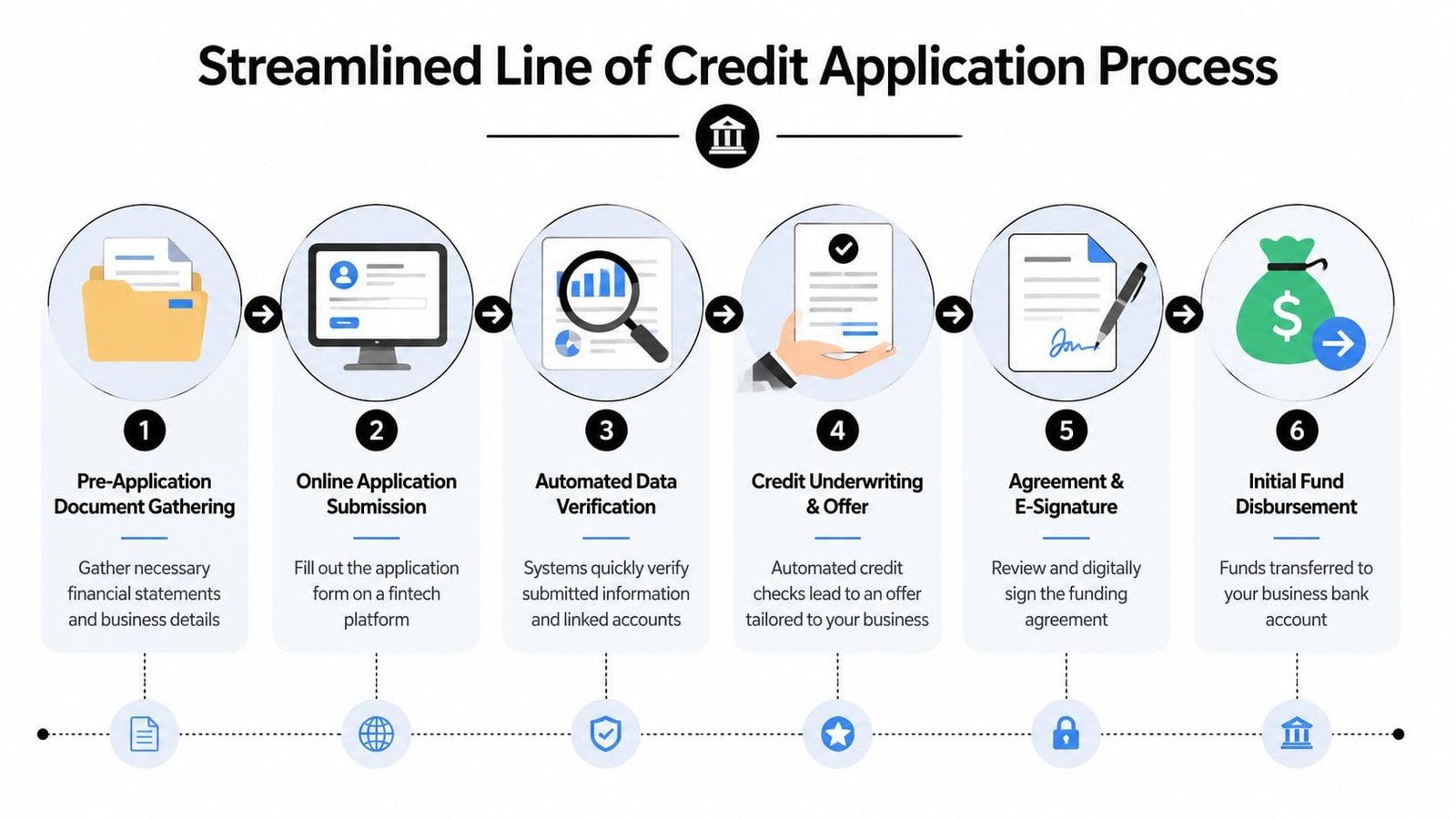

Modern lending platforms can move fast because they compress the messy parts of underwriting. They don't remove underwriting. They organize it.

A same-day line of credit is typically disbursed the same day of approval, with lenders offering funding in as fast as one hour. Automated underwriting drives those quick decisions for most applicants, though income verification can add a few hours, and the loan agreement itself often takes only five to 15 minutes to complete and sign, according to Experian's explanation of how same-day loans work.

Step 1: Gather before you log in

The biggest mistake applicants make is opening the application first and hunting for documents second.

Start with your materials ready, named clearly, and easy to upload. If the platform allows direct bank connection, decide in advance whether you'll use it. Digital verification often helps speed because it gives the underwriter cleaner transaction visibility than emailed attachments and screenshots.

Step 2: Complete the application like an underwriter will read it

Don't treat the form like a lead capture page. Treat it like part of the credit memo.

That means:

- Use the exact legal name from your business records.

- Enter revenue accurately. Inflated numbers don't impress underwriters. They trigger reconciliation.

- List the right industry and use of funds. “Working capital” is acceptable, but a more concrete explanation is better when the need is time-sensitive.

- Double-check owner information before submission.

A clean first pass saves hours later.

Step 3: Expect an automated pass first

Most fast lenders run your file through automated checks right away. They assess identity, business data, credit signals, and bank activity. If your file is straightforward, the process moves quickly.

If the system sees inconsistency, it escalates the file to manual review. That doesn't mean a decline. It means a person now needs to answer what the model couldn't.

When automation hands the file to a human, speed depends on how quickly the borrower can remove uncertainty.

Here's a useful overview of how digital applications are typically structured:

Step 4: Review the offer like an operator, not a desperate borrower

Once an offer arrives, slow down for a moment. Fast capital can still be bad capital.

Check:

- Repayment structure. Daily or weekly repayment changes cash flow pressure dramatically.

- Pricing transparency. If the lender won't explain the cost in plain terms, keep moving.

- Draw mechanics. Some products are revolving in practice. Others behave more like closed-end advances.

- Conditions after approval. “Approved” can still mean “pending final verification.”

Step 5: Sign fast, then stay reachable

The agreement stage can be short, but avoidable delay often arises at this point. Sign promptly, confirm funding instructions, and stay available by phone or email in case operations or underwriting needs one final confirmation.

If you disappear after approval, same-day funding can turn into next-day funding for no good reason.

A Realistic Funding Timeline

The cleanest way to think about line of credit same day funding is this: there are two clocks running at once. One is the credit decision. The other is the money movement.

A lender can approve quickly and still fund later if documents arrive late, the agreement sits unsigned, or your bank cutoff is missed. That's why smart operators plan backward from the cash need, not forward from the application timestamp.

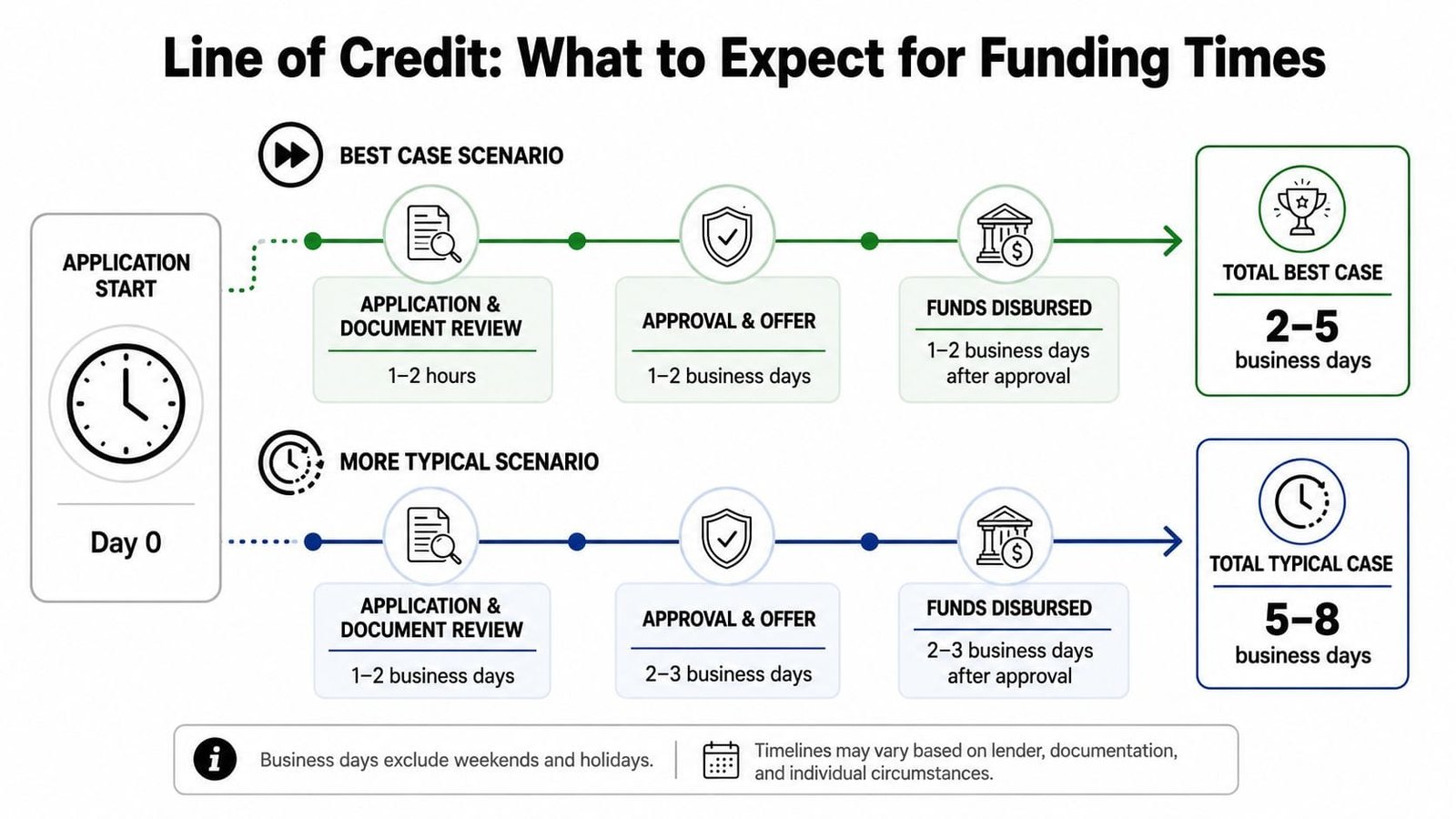

Best-case timeline

A best-case file has three features: complete documents, clear bank activity, and no ownership or verification surprises.

That timeline often looks like this:

| Stage | Best-case outcome |

|---|---|

| Application starts | Early in the business day |

| File review | Fast because documents are complete |

| Approval | Same day or shortly after review |

| Agreement signing | Immediate |

| Disbursement | Same day if all cutoffs are met |

This is the version borrowers see in ads. It can happen. But it depends on a narrow set of conditions lining up at once.

Typical timeline

For most real businesses, the more useful expectation is “fast this week,” not “money today.”

Common friction points include:

- Revenue needs explanation. Not a problem, just not instant.

- Statements require review. Large transfers, uneven deposits, or recent changes get a second look.

- Compliance checks need cleanup. Names, addresses, and ownership details must align.

- Bank timing gets in the way. Even after approval, transfer timing still matters.

The practical target for a serious business borrower isn't magical same-day funding. It's the shortest timeline with the fewest surprises.

If you want a lender-side view of where approvals slow down, this breakdown of how long business line of credit approval usually takes is worth reading before you apply.

How to improve your odds of landing in the fast lane

Three moves matter most:

- Apply early in the day

- Submit a complete file the first time

- Respond to follow-up questions immediately

A fourth matters too. Apply before the cash emergency becomes a crisis. The best funding decisions happen when the borrower still has options.

Funding Red Flags and Safer Alternatives

Urgency makes borrowers vulnerable. Lenders know that. When a business needs money now, bad products often get sold as speed solutions.

Line of credit same day funding becomes dangerous. A product may be fast, available, and easy to close, while still being the wrong tool for the business.

The MCA trap dressed up as a line of credit

For firms in the $20M to $50M revenue range, same-day funding often comes through merchant cash advances with hidden APRs of 70% to 150%. The NCUA reports that 68% of underserved small businesses in this revenue bracket accept MCAs for speed, while 79% of lenders refuse same-day business lines of credit without 12+ months of positive cash flow, as noted by the NCUA's access-to-credit resources.

That tells you two things.

First, speed is often available only by changing products. Second, the product that moves fastest may create a repayment burden that damages the business right after the emergency is solved.

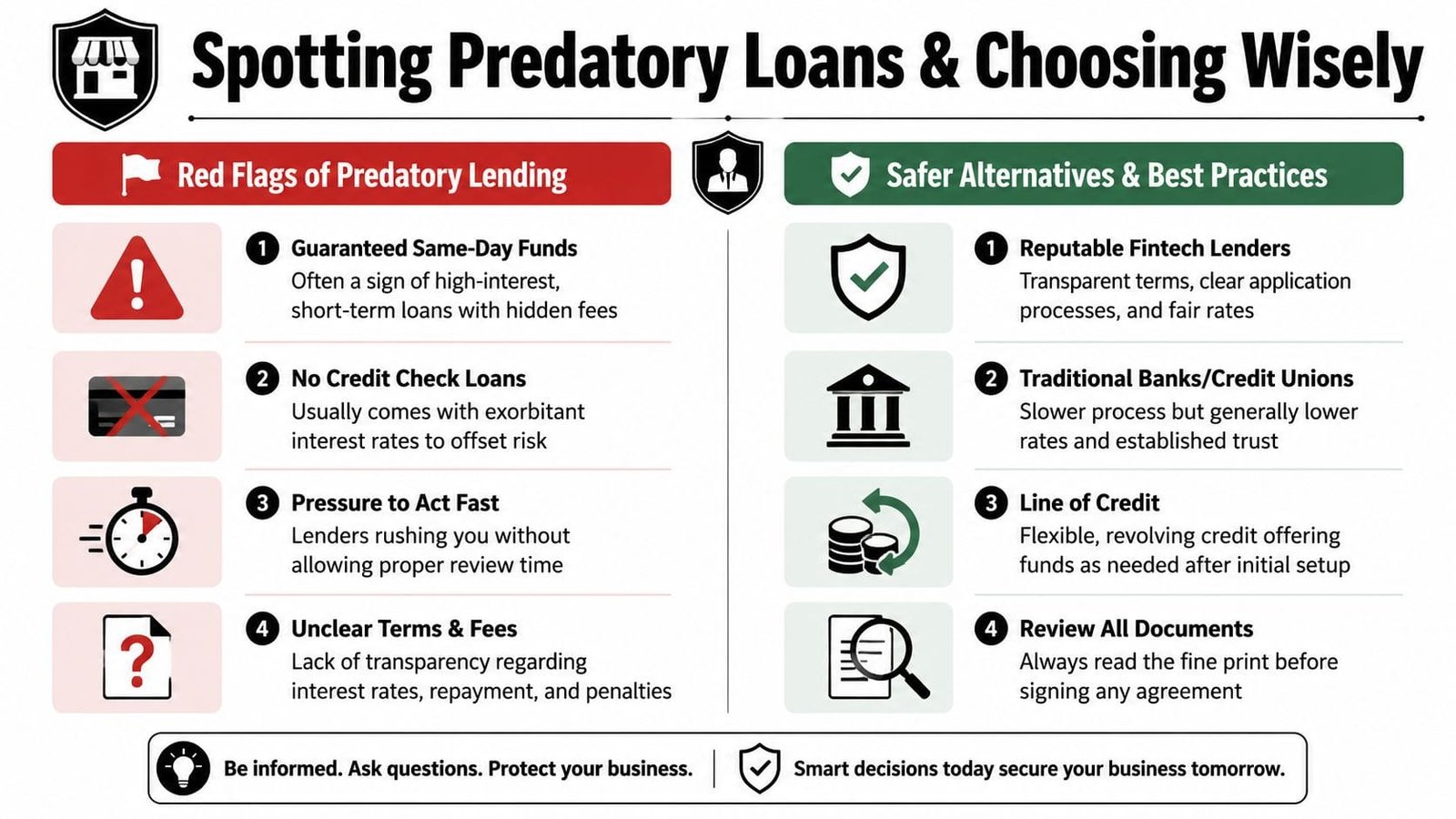

Four red flags that deserve immediate skepticism

- Guaranteed approval language. Real lenders underwrite. If approval is promised before review, pricing is usually absorbing the risk.

- Confusing fee math. If the cost can't be translated into a plain-language borrowing cost, assume it's expensive until proven otherwise.

- Pressure to sign immediately. Good lenders move fast. They don't force panic.

- Repayment pulled too frequently. Daily debits can crush a business with lumpy collections or project-based billing.

If the lender talks only about how fast you can get the money and never about how the repayment hits your cash flow, you're not in a financing conversation. You're in a sales conversation.

A quick product comparison

| Product | Speed potential | Main trade-off |

|---|---|---|

| Business line of credit | Fast when prepped well | Initial setup takes review |

| Short-term business loan | Can move quickly | Less flexibility than a revolving line |

| Invoice financing | Useful when receivables are strong | Best only for specific A/R-heavy situations |

| Merchant cash advance | Often very fast | Repayment can destabilize cash flow |

If you're evaluating looser-documentation offers, this guide to business line of credit options without bank statements and other fast-funding routes can help you distinguish convenience from risk.

What works better in practice

The safer move depends on the reason for the funding gap.

If receivables are the issue, invoice financing can be more rational than forcing a line of credit approval on an unrealistic timeline. If the need is a temporary operating shortfall and the business fundamentals are sound, a transparent short-term facility may be better than a disguised MCA. If the company needs recurring access to working capital, a real line of credit is still the stronger long-term tool, even if setup takes longer.

The wrong move is calling everything “same-day funding” and pretending the repayment economics don't change.

Your Path to Fast and Responsible Capital

Fast capital starts before the application. It starts with a business that can be understood quickly.

That means your records match, your bank activity tells a coherent story, your signer is available, and your funding request fits the product you're applying for. If you need a real business line of credit, treat “same-day” as a best-case outcome, not a planning assumption.

The practical strategy is simple:

- Prepare before the need becomes urgent

- Use lenders that combine automation with real underwriting

- Read the repayment structure before focusing on speed

- Avoid products that solve today's shortage by creating next month's crisis

One tool that helps many operators stay ahead of funding pressure is a rolling cash forecast. A disciplined essential tool for business growth is a 13-week cash flow model because it shows when the squeeze is coming early enough to choose better financing options.

Good CEOs don't just ask, “How fast can I get money?”

They ask better questions: Is this a true line of credit? What has to be verified? What could stall funding? What does repayment do to weekly cash flow? Those questions protect you from expensive shortcuts.

If you approach line of credit same day funding with that mindset, you'll move faster than most borrowers and make fewer costly decisions.

If you want to see real options without chasing hype, Business Loan Warrior lets you submit one no-fee application, check pre-approval without impacting credit, connect accounts securely, and review specific funding paths with human underwriters who can explain the trade-offs clearly.