You win a solid contract. The job could keep your crews busy, strengthen your backlog, and put your company in a different league. Then the main problem hits. You have to mobilize before the owner pays you. Materials need deposits. Subs want schedules. Payroll still lands every week. Equipment doesn't care that your first draw is still pending.

That cash squeeze is normal in construction. It doesn't mean your business is weak. It means the job is larger than the cash sitting in your account today. The right financing closes that gap so you can build without starving the rest of the company.

Table of Contents

- The Contractor's Dilemma Bridging the Capital Gap

- What Exactly Is a Construction Business Loan

- Exploring Your Construction Financing Options

- How Lenders Evaluate Your Loan Application

- Navigating the Application and Draw Process Timeline

- The True Cost of a Construction Loan

- Alternative Funding for Contractor Cash Flow

The Contractor's Dilemma Bridging the Capital Gap

A lot of owners reach for financing after the stress shows up. The better move is earlier. The capital gap usually appears right after you win the work, not after you've finished a phase and sent an invoice.

Say you land your biggest tenant improvement or ground-up project so far. On paper, the job is profitable. In real life, the first weeks are expensive. You need labor on site, rented iron scheduled, permits moving, and key materials ordered before you can bill enough to cover what went out. That's where many contractors get pinched.

Field reality: A profitable project can still create a cash crisis if the billing cycle lags behind labor, equipment, and supplier payments.

Construction businesses don't fail this test because they can't build. They fail it because timing gets brutal. Cash leaves quickly and comes back slowly. That mismatch is one reason builders look beyond generic small business loans and toward financing built around projects, draws, equipment, or receivables.

If that feels familiar, this practical breakdown of smart financing moves for small builders is worth reading alongside your project planning. It helps frame financing as part of operations, not an emergency patch.

The pressure points owners feel first

Some costs hit before the owner release does. Others arrive while retainage is still tying up your margin.

- Mobilization costs: Site prep, deposits, insurance, and early labor hit fast.

- Material timing: Suppliers may want money before the phase is complete enough to invoice.

- Payroll rigidity: Crews expect to be paid on schedule whether the draw has cleared or not.

- Overlapping jobs: One growing company often funds one project's start-up while waiting on another project's payment.

The fix isn't always a single product. Sometimes it's a true construction loan. Sometimes it's a line of credit paired with equipment financing. Sometimes it means keeping project financing separate from working capital so one job doesn't drain the whole company.

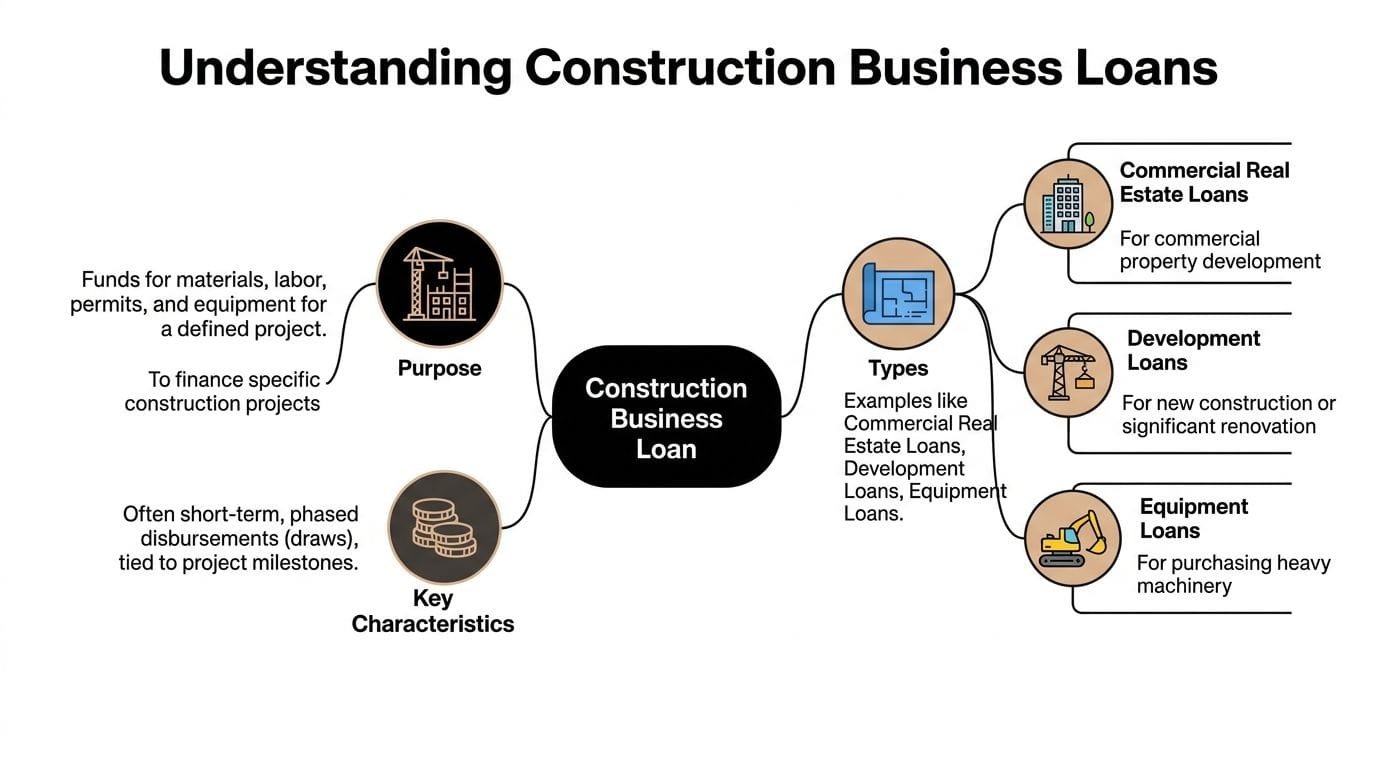

What Exactly Is a Construction Business Loan

A construction business loan funds a defined project, not just the business in general. The lender approves a budget tied to the job, then releases money in stages as work is completed and documented.

That difference matters on a live project. If you are pouring cash into mobilization, labor, and materials before the next owner payment hits, the structure of the financing matters almost as much as the rate.

Commercial construction loans are usually set up as short-term financing for a build cycle, with funds disbursed through draws tied to progress, as described by the builder's guide to construction financing. In plain terms, the loan is built to match the way a project spends money.

Why the money comes in draws

Draws exist because construction spending is uneven. Early costs hit before the project has enough progress to support a full invoice, and later phases often require inspections, lien waivers, and updated budgets before more money goes out.

A draw structure protects all sides of the deal.

- For the lender: funds go out against verified work, not assumptions.

- For the contractor: interest often applies only to the amount already disbursed, which can reduce carrying cost.

- For the project: the budget stays tied to milestones, change orders, and actual completion.

Many owners skim this part and regret it later. The draw process controls timing, paperwork, and how fast cash reaches the job.

That is also why lenders ask for more than tax returns and bank statements. They often want plans, permits, a detailed scope, project budget, timeline, subcontractor information, and evidence that your company can complete the work. They are evaluating the job and the borrower at the same time.

When this structure makes sense

Construction business loans fit projects with a clear scope and a defined use of funds. Ground-up builds, major renovations, additions, tenant improvements, and other milestone-based jobs usually fit that model well.

A standard term loan solves a different problem. It works better for broad business needs that are not tied to a phased build. If you are weighing both approaches, this guide on construction loans vs equipment financing for your business can help you separate project funding from long-term asset purchases.

The wrong structure creates avoidable pressure. A lump-sum loan can leave you paying for idle cash too early, while a draw-based loan can feel too rigid if flexible working capital is needed across several jobs. Good financing matches the job's billing pattern, inspection schedule, and cash gap, not just the total dollar amount.

Exploring Your Construction Financing Options

A contractor finishes payroll on Friday, fronts materials on Monday, and still waits two weeks for the next draw or owner payment. That gap is where the wrong loan creates stress and the right one keeps the schedule intact.

The first decision is not bank versus online lender. It is matching the financing tool to the problem in front of you. A ground-up build with inspections and staged costs needs a different structure than a skid steer purchase, and both are different from covering a 45-day receivables gap after progress billing goes out.

Construction loan options at a glance

| Feature | Traditional Bank Loan | SBA Loan (7a/504) | Fintech/Alternative Lender |

|---|---|---|---|

| Best fit | Defined construction project with strong documentation | Established business seeking competitive pricing or long-term use cases | Speed, flexibility, or nontraditional cash flow situations |

| Pricing | Often lower than fast capital, but highly selective | Often competitive when eligibility fits | Usually easier to access, but you need to examine total cost carefully |

| Approval speed | Slower | Slower, with more paperwork | Faster in many cases |

| Structure | Often draw-based for project lending | Can support broader business uses depending on program | Varies widely by product |

| Flexibility | Lower | Moderate, program-dependent | Higher |

| Documentation burden | Heavy | Heavy | Often lighter, but still serious for larger requests |

| Strong use case | Ground-up or major renovation | Expansion, equipment, real estate, working capital depending on program | Bridging timing gaps, receivables pressure, urgent operational needs |

Traditional bank construction loans usually fit owners who have strong financials, clean records, and a clearly defined project budget. The trade-off is speed and rigidity. Banks tend to offer better pricing than fast capital, but they usually want more paperwork, more borrower equity, and a job that stays close to plan.

SBA financing can work well if you need lower monthly payments, longer terms, or funds that support the business beyond one job. The SBA publishes current rate limits for 7(a) loans through its official SBA loan interest rates page, and loan volume data through its SBA 7(a) and 504 lending reports. In practice, the appeal is usually cash flow, not just rate. Stretching repayment over a longer term can leave more room for labor, retainage, and change-order lag.

Alternative lenders solve a different problem. They are often used when a contractor cannot wait a month for committee approval, needs to make payroll before an invoice clears, or has uneven deposits because several jobs are at different billing stages. That speed costs more. Sometimes that premium is justified. Sometimes it is a sign that the business needs a receivables strategy, not expensive debt.

A broader builder's guide to construction financing can help if you're comparing project finance with larger development planning decisions.

A smart fit depends on what is squeezing cash

If the pressure is tied to one project, a draw-based construction loan may be the cleanest answer. If the pressure comes from equipment needs, use a structure built for the asset, not the job. If the pressure comes from progress billing delays, retainage, or slow-paying GCs, flexible working capital or invoice-based funding may fit better than a standard construction note.

That distinction matters. I have seen profitable contractors create unnecessary strain by using long-term project debt to solve a short-term billing gap. They ended up paying for money longer than needed and still had timing issues on the next job.

One area owners often miss is specialized support programs. Biz2Credit notes in its report on financing for underserved small businesses that many eligible firms fail to pursue programs designed for underserved borrowers. If that applies to your company, ask about 8(a), CDFIs, and local lending programs instead of stopping with a standard bank application.

If you are sorting out whether your need is project funding or an asset purchase, this comparison of construction loans versus equipment financing helps frame the decision correctly. Finance the build, the machine, or the gap between billing and cash. Those are three different problems, and they rarely call for the same loan.

How Lenders Evaluate Your Loan Application

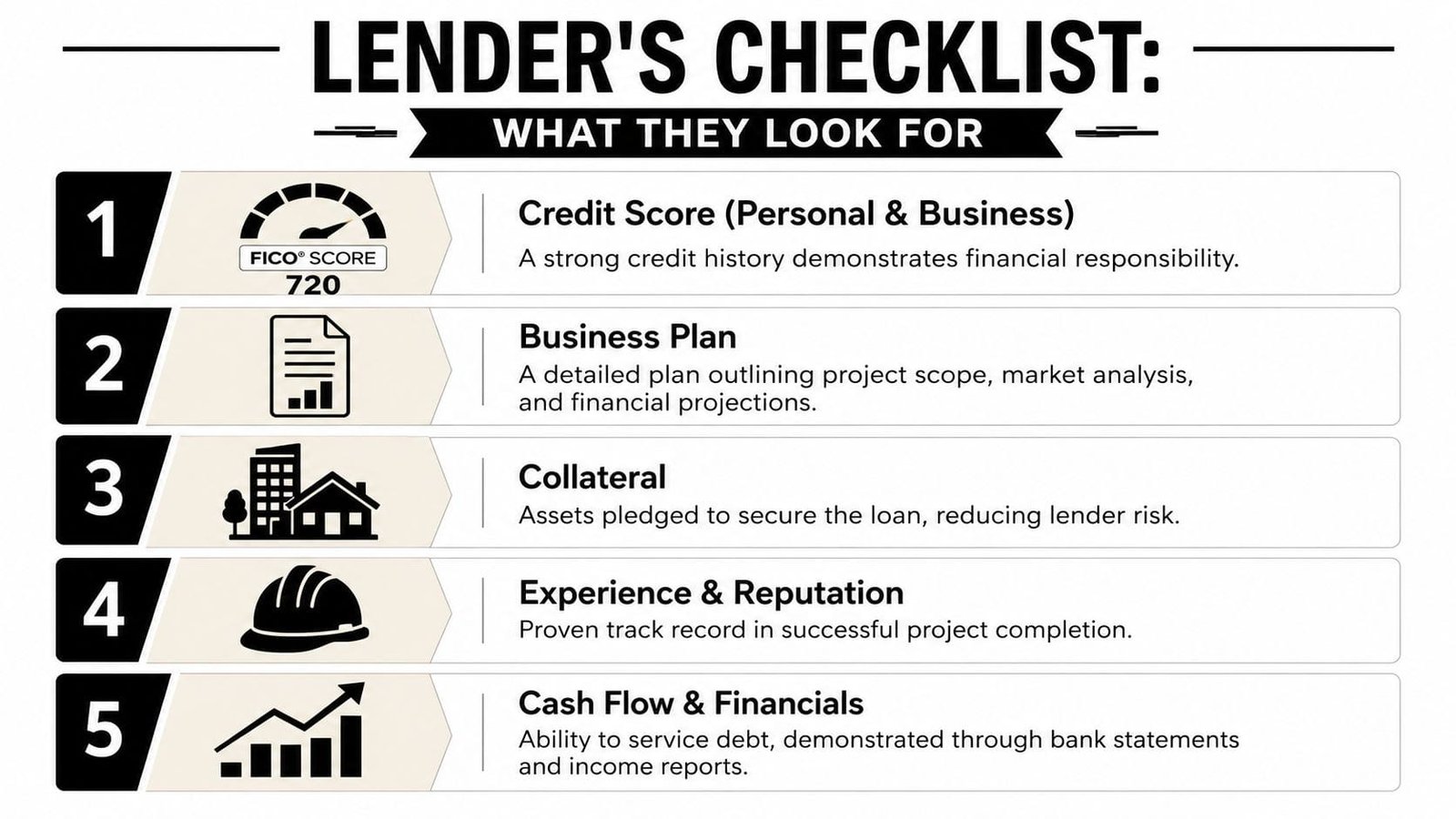

Most owners think lenders start with the building. They don't. They start with risk. Then they decide whether your company, your project, and your paperwork reduce that risk enough to approve the request.

For commercial construction loans, lenders often want a minimum down payment of 20%, though some require 30% to over 40%. Underwriters also commonly look for a maximum debt-to-income ratio of 40% to 45% and a minimum credit score between 660 and 720, according to FNBOK's guide to construction business loan requirements.

A quick visual summary helps:

What underwriters check first

A lender is asking three plain questions.

Can this borrower repay?

They look at credit, financial statements, existing debt, and available liquidity.Can this team finish the project?

They review contractor experience, schedules, plans, permits, and cost detail.If the job runs into trouble, what protects the lender?

They assess collateral, borrower equity, and the expected value of the completed project.

That means a strong file isn't just a strong tax return. It's a file where the numbers, scope, and execution plan all agree with each other.

Underwriter mindset: If your budget, timeline, and contractor story don't line up, the lender assumes the field will be harder than the paper.

This video gives a decent overview of how lenders think about business financing and approval standards:

What makes a file stronger

Good applications feel boring to an underwriter. That's a compliment. They are complete, consistent, and easy to verify.

- Clean financials: Separate business and personal records. Make cash movement easy to follow.

- Detailed job package: Include plans, permits, budget assumptions, vendor quotes, and a realistic schedule.

- Experience proof: Show similar completed work, not just ambition.

- Contingency thinking: Explain how you'll handle cost pressure, delays, or change orders.

- Equity clarity: Document where the down payment comes from and that it is available.

If you're tightening up your planning before applying, these Growth 4 Trades business strategies are a useful reference for turning a rough contractor plan into lender-ready material.

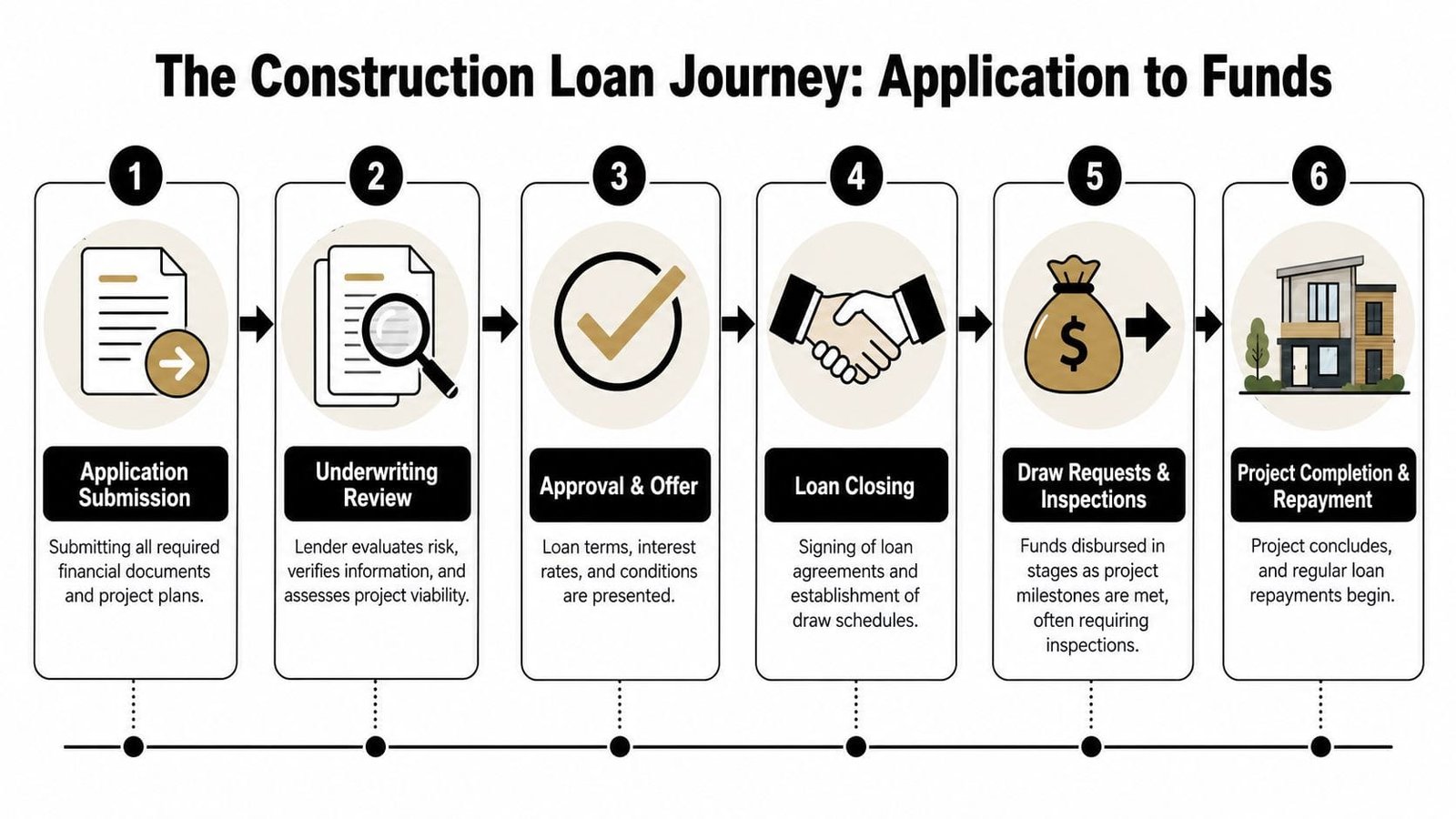

Navigating the Application and Draw Process Timeline

You win a solid job, line up subs, and order materials. Then cash tightens before the first large customer payment hits. That gap is where the construction loan timeline starts to matter, because approval and draws rarely move at the speed of your payroll, supplier terms, or progress billing cycle.

Underwriting for a construction loan often stretches across several weeks, and complex commercial files can take longer. The Mortgage Bankers Association outlines the broader commercial real estate loan closing process and the many third-party reviews that can slow funding, including appraisal, environmental, legal, and documentation steps, in its overview of why commercial real estate loans can take time to close. For contractors, that delay matters because expenses usually start showing up before loan proceeds do.

What happens between application and closing

The lender is checking more than your credit and tax returns. It is trying to confirm that the project can be built as proposed, within budget, and with enough controls to release funds in stages without creating repayment problems later.

Files usually stall for practical reasons:

- Plans and budget do not match: The scope in the drawings does not line up with the cost breakdown.

- Permits are still pending: The lender will not fund against a schedule that starts before approvals are in place.

- Entity and contract details are unclear: Ownership, guarantors, GC responsibility, and subcontractor roles need to be documented cleanly.

- Insurance or licensing is incomplete: A small paperwork gap can hold up a large closing.

- No contingency explanation: Lenders want to see how you will handle overruns, delays, and change orders without draining working capital.

The fix is simple, but not easy. Treat the loan package like a job closeout file. If a third party can review it in one sitting and understand who is doing what, when money is needed, and what backs up each cost, the process usually moves better.

How draw requests work in the field

After closing, the pressure shifts from approval to execution. A draw is a reimbursement and control process tied to completed work, not a blank check for upcoming costs. That distinction catches a lot of contractors off guard, especially if they are used to owner deposits or faster receivable cycles.

A typical draw cycle looks like this:

- A defined phase of work is completed.

- You submit the draw package. That often includes invoices, lien waivers, photos, schedule updates, and a summary of stored materials if the lender allows them.

- The lender or inspector confirms progress.

- Funds are released based on verified completion.

Paperwork usually determines whether money shows up on time. I see more draw delays caused by missing waivers, unsigned change orders, and outdated cost reports than by actual jobsite underperformance.

If your team has not worked from staged disbursements before, review a sample construction loan draw schedule before closing. It gives your project manager, bookkeeper, and owner a shared picture of when to request funds and what support each draw needs.

One more point matters here. Draw friction gets worse when the job budget is too tight from the start. If you need to create more room in the numbers before funding, these strategies for construction cost reduction can help you identify savings without weakening execution.

The True Cost of a Construction Loan

A lot of contractors focus on rate first, then get surprised by the bill that shows up around the rate. I see it often. A loan that looks cheap on page one can put real pressure on margin once draw fees, inspections, holdbacks, legal costs, and extra interest from schedule slippage start stacking up.

For construction, cost is not just a pricing question. It is a cash flow question.

If your job bills monthly but payroll runs every week, the wrong loan structure can hurt even if the stated rate looks reasonable. SBA loan pricing is generally tied to the base rate plus an allowed spread, and the SBA publishes those limits in its 7(a) loan program terms. Bank construction pricing varies by lender, project risk, collateral, and how the draws are set up, so the term sheet matters more than any broad rate range you see in a roundup article.

Rate is only one part of the price

The actual cost usually shows up in five places.

- Upfront cash required: Down payment, equity injection, and closing costs all hit before the project starts producing cash.

- Third-party charges: Appraisals, title work, legal review, and inspections are common and often paid whether the job runs smoothly or not.

- Draw-related costs: Some lenders charge per draw, limit draw frequency, or require inspections before every release.

- Interest structure: Interest-only on disbursed funds can help early, but the benefit shrinks if draws are delayed or the schedule drifts.

- End-of-term risk: A short maturity, refinance requirement, or balloon payment can create a problem right when you expected relief.

Variable rates need special attention. They may start lower, but a long build cycle changes the math fast. If the project runs past schedule, you are not only carrying job costs longer. You may also be carrying them at a higher rate.

What the loan feels like in the field

This is the part generic loan articles usually miss. Contractors do not experience financing as an APR. They experience it through timing.

A lender that reimburses slowly can force you to cover labor and materials longer than planned. A lender that requires extra documentation for every draw can tie up your bookkeeper and PM when they should be closing change orders and keeping production on track. A loan with modest fees but rigid draw rules can cost more in practice than one with a slightly higher rate and a cleaner disbursement process.

That trade-off is real. Cheaper money is not always cheaper execution.

How to compare offers without fooling yourself

Skip the lowest-rate contest. Review the offer the same way you review a subcontract. Look at what it costs, how it performs under stress, and what happens when the job does not go exactly to plan.

Use a short checklist:

- How much cash has to go in before the first advance?

- Which fees are paid at closing, and which show up during the build?

- How often can you draw, and what triggers inspection charges?

- Is the rate fixed or variable?

- How much interest reserve, if any, is built into the structure?

- What happens if there is a change order, delay, or cost overrun?

- Does the loan mature before the project is fully stabilized or paid out?

One practical test helps. Ask the lender to walk through a delayed draw, a two-week inspection lag, and a schedule extension. Their answer tells you more than the headline rate.

If you want to protect margin before financing starts, these strategies for construction cost reduction can tighten the budget and reduce how much the project needs to carry in borrowed funds.

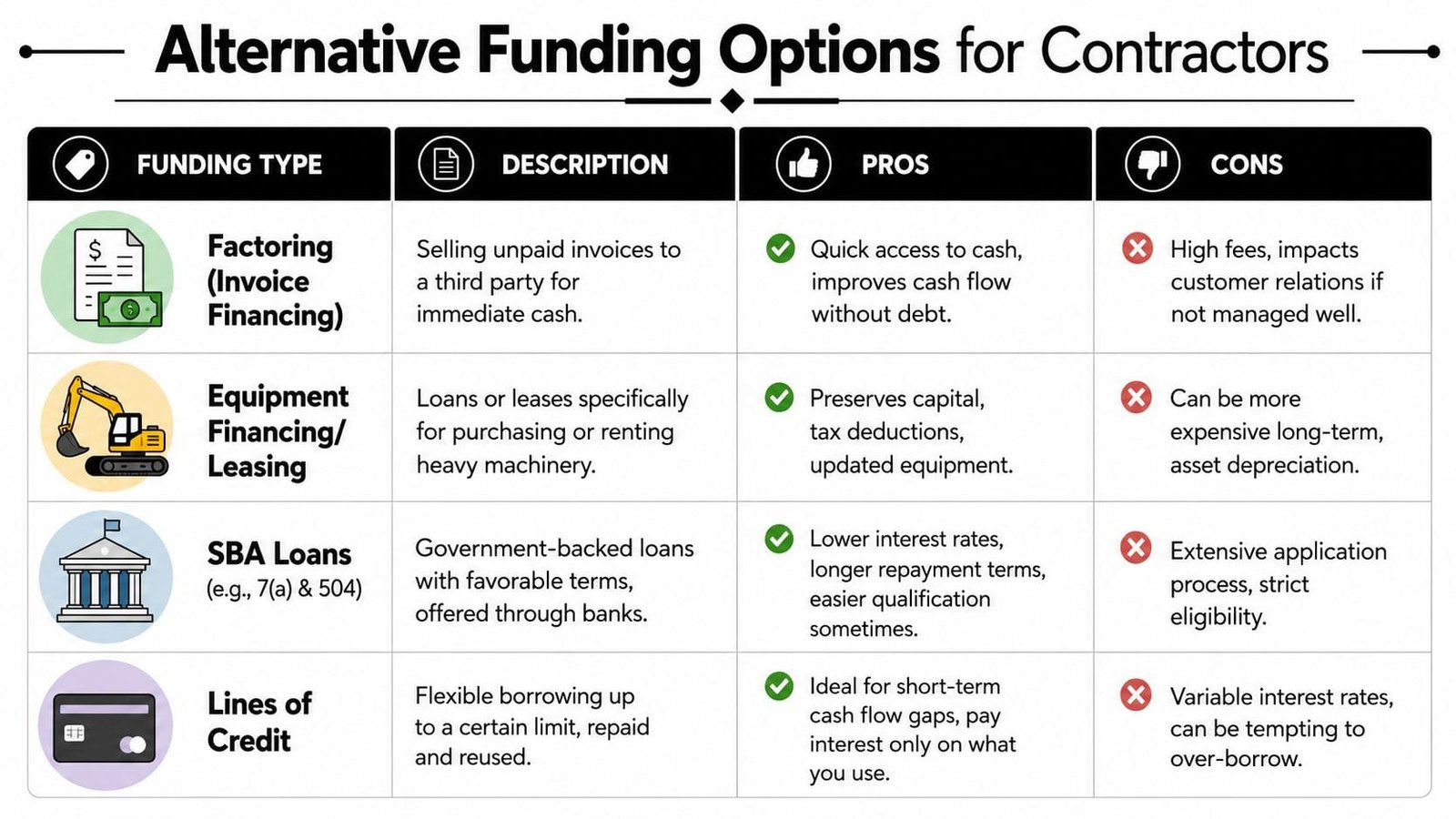

Alternative Funding for Contractor Cash Flow

The biggest blind spot in most articles about construction business loans is simple. They talk about funding the project and ignore funding the company while the project is underway.

That gap matters because progress billing rarely lines up neatly with payroll, materials, and vendor terms. In one discussion of contractor finance, the point was put bluntly: banks and contractors with progress billing often don't fit well together. The same source notes that 40% of construction firms face payment delays, which is why revenue-based financing and other cash flow tools deserve serious attention in this industry, as discussed in this video on contractor cash flow and progress billing challenges.

Why progress billing creates financing gaps

You can be fully booked and still cash-poor. That's the contractor version of looking busy while the checking account tightens.

The mismatch usually shows up in a few places:

- Receivables are large but slow: You have approved work in the pipeline, just not cash in hand yet.

- Labor is weekly and fixed: Payroll doesn't wait for owner paperwork.

- Material suppliers want certainty: They may not care that your invoice is in review.

- Multiple jobs overlap: One delayed payment can pressure three active projects.

A contractor with strong receivables can still be a weak fit for a traditional bank line if the lender doesn't understand how progress billing actually works.

How to build a practical capital stack

The best solution is often a mix, with each tool handling one problem well.

- Line of credit for short gaps: Good for payroll, minor overruns, and temporary timing issues. Best when the gap is short and predictable.

- Equipment financing for iron and vehicles: Keep machine purchases separate from operating cash so a loader doesn't eat the money needed for labor.

- SBA financing for broader business growth: Useful when the need is larger, more strategic, and you can tolerate the process.

- Invoice or receivables-based funding: Often the cleanest answer when the issue is approved work that hasn't been paid yet.

- Revenue-based financing: Can help when cash flow is real but uneven, especially if traditional bank underwriting doesn't fit your billing cycle.

This is the key practical point. A construction loan funds a build. It doesn't automatically solve the day-to-day working capital stress that comes with running a contractor business. Owners who separate project finance from operating liquidity usually make better decisions under pressure.

If you're weighing construction business loans against lines of credit, receivables funding, SBA options, or equipment financing, Business Loan Warrior is a practical place to start. You can review funding paths for your situation, compare options without turning the process into a full-time job, and find a structure that fits the way contractors get paid.