You're probably dealing with one of two situations right now. Sales are solid, but cash timing is messy. Or an opportunity just showed up, inventory at a discount, a marketing push that can scale, a repair you can't postpone, and you need flexible capital without making an expensive mistake.

That's where the business line of credit vs credit card decision gets real. Both give you revolving access to funds. They are not interchangeable.

One is built for day-to-day spending speed. The other is built for deliberate cash flow management. If you use the wrong one, you raise your cost of capital, clutter your repayment cycle, and sometimes damage your credit profile without realizing it until the next renewal or underwriting review.

Table of Contents

- Choosing Your Flexible Funding Tool

- At a Glance How They Fundamentally Differ

- A Detailed Breakdown of Cost and Fee Structures

- Impact on Your Operations and Business Credit

- Strategic Use Cases When to Use Which Tool

- Your Decision Framework and How to Apply

Choosing Your Flexible Funding Tool

Most owners don't ask this question when business is calm. They ask it when timing gets tight.

A supplier wants payment before receivables clear. Payroll hits before a large customer pays. A seasonal business needs stock now, not after the busy window passes. In those moments, flexibility matters more than theory. But the wrong tool can turn a short-term need into a long-term drag on margins.

The reason credit cards dominate is simple. They're easier to use in practice. According to the Federal Reserve's 2025 Small Business Credit Survey, 56% of U.S. employer firms used business credit cards regularly in 2023, compared with 34% that used business lines of credit, which makes cards the most widely adopted small business financing tool (Federal Reserve SBCS data). That adoption gap says more about convenience than strategy.

What owners usually get wrong

Many successful operators treat both products as “extra liquidity.” That's too loose. A credit card is usually best for routine operating purchases, especially when your team needs to move fast and your accounting team wants clean merchant-level expense data. A line of credit is usually better for uneven working capital needs that don't fit neatly into a card transaction.

Use the distinction this way:

- Use a credit card when the expense is frequent, smaller, and likely to be paid off quickly.

- Use a line of credit when the need is larger, cash-based, irregular, or tied to timing gaps.

- Avoid using either as a substitute for a long-term capital solution if the underlying need isn't short term.

Bottom-line view: convenience explains why credit cards are common. Cost control explains why better-run businesses often add a line of credit before they actually need one.

The best borrowers don't ask, “Which one should I get?” They ask, “Which tool fits this specific use of capital?” That's the right question because access to revolving credit only helps if it protects margin, preserves optionality, and doesn't create avoidable pressure on your balance sheet.

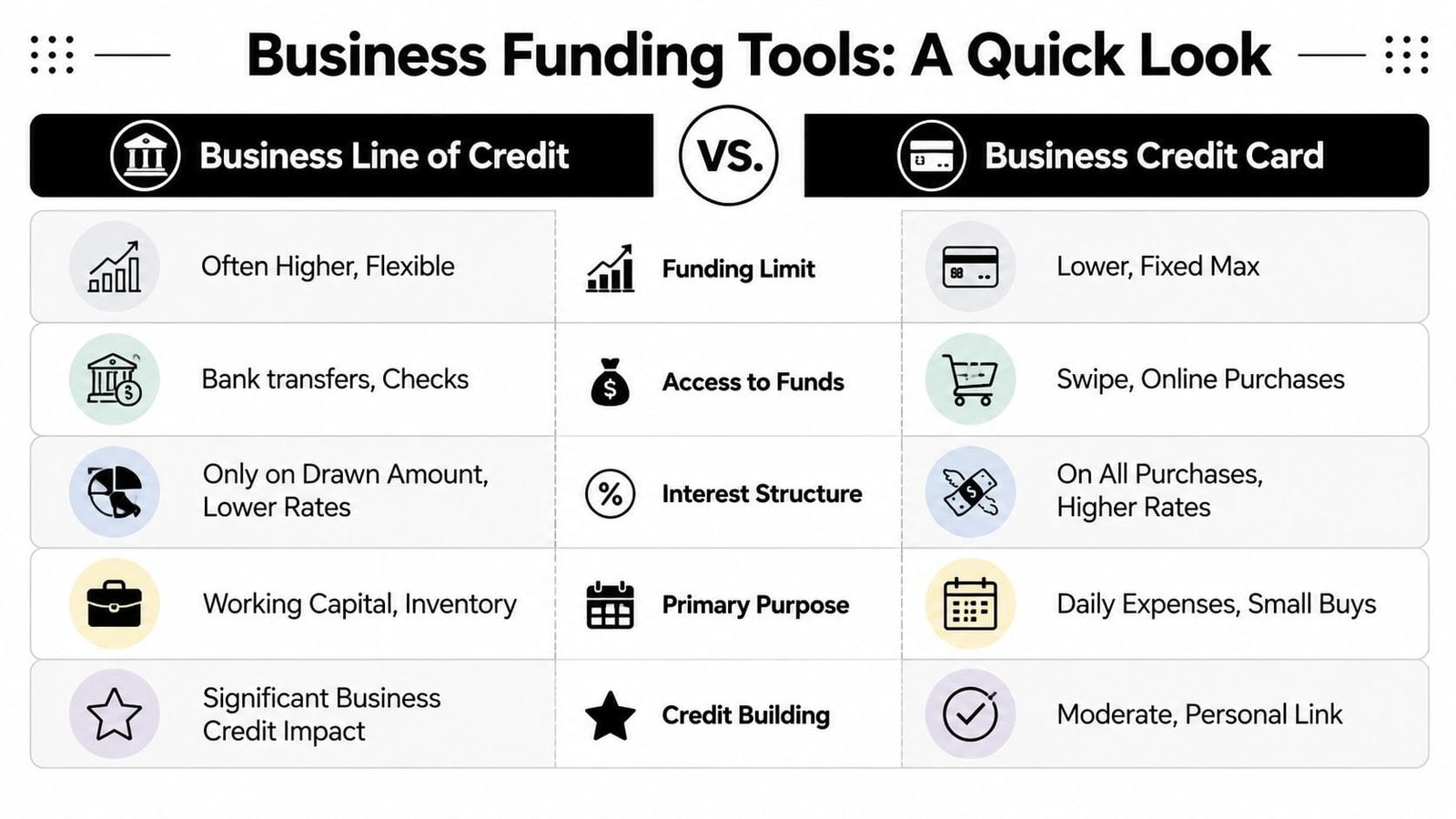

At a Glance How They Fundamentally Differ

Here's the cleanest way to look at a business line of credit vs credit card. One gives you a pool of capital you draw from when needed. The other gives you a payment instrument you can use immediately at the point of sale.

| Decision factor | Business line of credit | Business credit card |

|---|---|---|

| How you access funds | Draw funds into your business account or through lender access methods | Swipe, tap, or use online for purchases |

| Best fit | Working capital, vendor payments, inventory, payroll timing | Daily expenses, travel, subscriptions, small recurring purchases |

| Funding capacity | Often much higher | Usually lower |

| Interest structure | Interest starts on draws right away | Grace period may apply if paid in full |

| Operational style | Deliberate borrowing | Fast transactional spending |

The money moves differently

A line of credit is closer to a working capital reserve. You draw what you need, when you need it, then repay and redraw as cash flow changes. That structure is why it fits inventory buys, payroll support, and vendor invoices better than a card does.

A business credit card is built for transaction speed. It's better for software, flights, fuel, office purchases, and all the small recurring charges that pile up across departments. If you need a refresher on the mechanics, this breakdown of how a business line of credit works gives a practical overview of the draw-and-repay cycle.

The repayment logic is not the same

The biggest structural difference isn't just access. It's how borrowing starts costing you money.

Business lines of credit typically come with higher limits and lower APRs than business credit cards. Lines often range up to $500,000 or more, while cards usually cap around $50,000 to $100,000. For qualified borrowers, line of credit APRs generally range from 6% to 12%, while business credit card APRs often span 16% to 34% (Lendio comparison).

That doesn't automatically make a line cheaper in every case. If you pay a card in full inside the billing cycle, the cost can be minimal or even avoided on purchases. If you carry balances, especially on larger amounts, the math usually flips hard in favor of the line.

If the expense will sit on your books beyond the next statement cycle, a line of credit usually deserves first look.

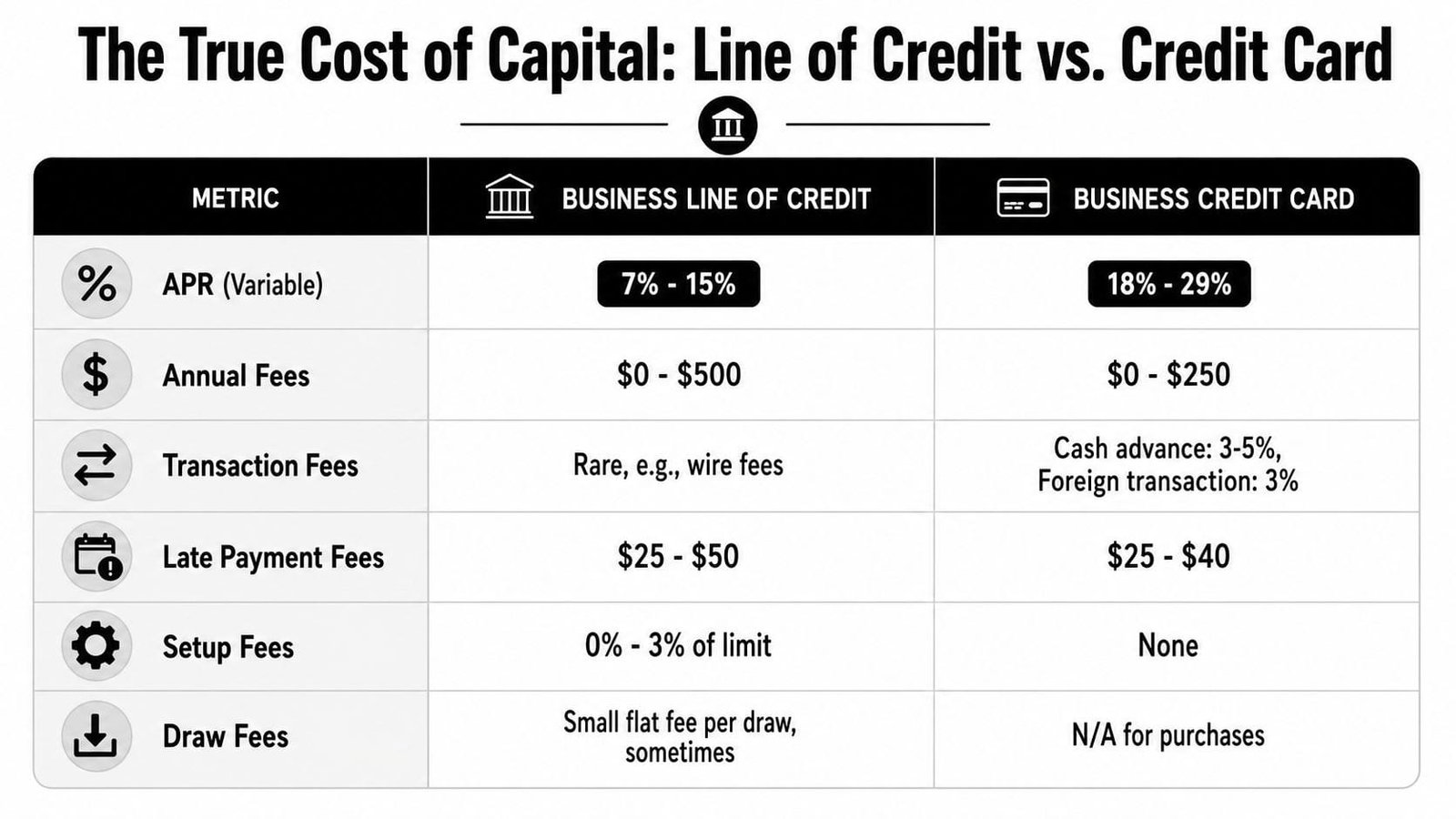

A Detailed Breakdown of Cost and Fee Structures

Most owners stop at APR. That's not enough.

The true comparison in a business line of credit vs credit card decision is total cost of capital, not advertised rate. You need to examine interest, timing of accrual, transaction friction, and the fees that show up whether you use the product heavily or barely touch it.

APR matters but it is not the full cost

The average rate for commercial business lines of credit in Q3 2025 ranged from 6.99% to 7.38% for fixed-rate lines and 7.63% to 7.91% for variable-rate lines, while business credit cards commonly exceed 20% APR (Bankrate reporting on the Small Business Lending Survey). On rate alone, the line wins for carried balances.

But cards have one major pricing advantage. They can offer a grace period on purchases if you pay in full. That feature changes the economics for disciplined operators. A line of credit does not usually give you that breathing room. Interest starts when you draw.

That means the honest cost question is this:

- Will you revolve a balance? Use the lower-rate product.

- Will you pay in full each cycle? The card can be more efficient.

- Will you need cash, not merchant card acceptance? The line is operationally stronger even before rate enters the picture.

If you want a cleaner framework for evaluating all borrowing costs, this guide on how to calculate the real cost of a small business loan is worth reviewing before you sign anything.

Fee creep changes the answer

Here's the part many comparison articles miss. Lines of credit can look cheap on rate and still disappoint on total cost.

Some lenders charge annual fees, origination fees, draw fees, and maintenance fees. The fee structure matters most when your usage is light or occasional. If you open a line “just in case” and barely use it, those charges can eat away at the pricing advantage you thought you were getting.

The verified data specifically notes a recent shift in line-of-credit pricing. In 2024 to 2025, some major lenders introduced or increased annual fees in the $95 to $175 range and maintenance fees up to 0.25% of the line amount, even when no funds are drawn, according to the verified lender fee summary provided in the source material (Wells Fargo business line fee reference).

That changes the decision in a practical way:

| Cost issue | Business line of credit | Business credit card |

|---|---|---|

| Base APR on carried balance | Usually lower | Usually higher |

| Grace period on purchases | No | Often yes if paid in full |

| Cash access for operations | Strong | Usually expensive or awkward |

| Non-interest fees | Can include annual, draw, origination, maintenance | Often simpler, though cash advances can be costly |

| Best cost profile | Larger or longer short-term borrowing | Fast purchases repaid quickly |

What smart owners actually compare

Don't compare products with one question. Compare them with five.

- How long will the balance stay outstanding? Longer carry usually favors the line.

- Is the expense payable by card? If not, the card may not be useful in practice.

- Will the lender charge fees even when unused? That matters for standby facilities.

- Will you take cash from the card? That's often where card pricing gets ugly.

- Do rewards distract from financing cost? They often do.

Practical rule: rewards are nice. Lower borrowing cost is better. Never let cashback justify carrying an expensive revolving balance.

A business credit card is a strong spending tool. A line of credit is a stronger funding tool. If you blur those jobs, you usually overpay.

Impact on Your Operations and Business Credit

The wrong choice doesn't just cost more. It also changes how your business behaves.

A card encourages speed. That's useful when your team books travel, pays SaaS vendors, buys digital ads, or handles routine branch-level expenses. A line of credit forces more deliberate borrowing because each draw feels like financing, not spending. That difference sounds small. It isn't.

Operational fit affects discipline

Good operators match the product to the workflow.

Cards are excellent for distributed spending because they create a clean purchasing lane. Team members can buy what they need inside policy. Accounting gets merchant data. You also have a built-in opportunity to avoid interest by paying the statement balance in full. That's why disciplined finance teams spend time leveraging credit card grace periods instead of just chasing rewards.

Lines of credit fit a different operating pattern. They work better when finance controls the draw, allocates the funds to a specific need, and repays based on receivable timing, inventory turnover, or expected project cash flow. That's more controlled, but it also means the line can become a pressure valve for weak forecasting if management gets lazy.

Utilization can hurt faster than owners expect

This is the issue most owners underestimate.

According to the Small Business Credit Survey data cited in the verified source material, 38% of small business owners reported credit score declines due to high revolving debt utilization, and lines of credit were often seen as more volatile because draw patterns can spike unexpectedly (Bankrate summary of line of credit pros and cons).

Here's why that matters in practice. A line can look harmless when it sits unused. Then a large draw lands right before reporting. Utilization jumps. Your business suddenly looks like it's carrying more debt than it did the month before, even if the draw was tactical and temporary.

A card can cause the same issue, but monthly card balances are often easier to forecast and manage because spending cadence is more regular. For many companies, line utilization is lumpier. Lumpiness creates surprises. Surprises create underwriting questions.

A revolving facility isn't just liquidity. It's part of your credit profile every time it reports.

The broader distinction between business credit and personal credit matters here too. Owners often focus on approval and ignore reporting behavior until renewal season. By then, the file already tells a story. High, irregular utilization can make a healthy business look stressed.

What to watch operationally

- Monitor reporting timing: Don't assume a temporary draw is invisible.

- Match the tool to the expense type: Transaction-heavy spend belongs on cards. Cash-based timing gaps often belong on the line.

- Set internal utilization guardrails: Finance should know what level triggers concern before the lender does.

- Review behavior, not just balances: Repeated emergency draws often point to forecasting problems, not just funding needs.

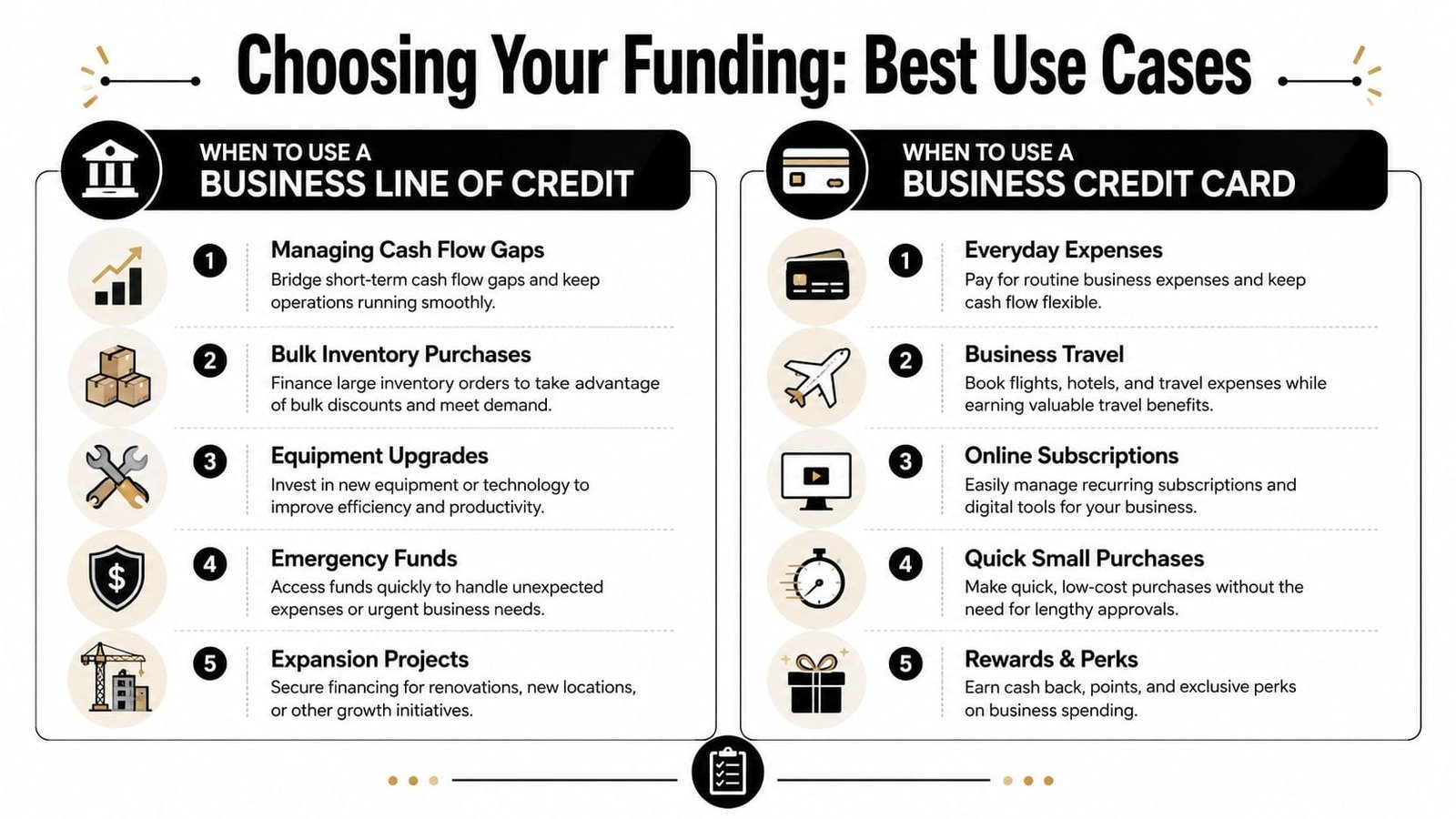

Strategic Use Cases When to Use Which Tool

The decision becomes straightforward. Don't choose based on product labels. Choose based on the job.

Use a credit card for controlled operating spend

A business credit card is the right tool when speed, merchant acceptance, and short repayment cycles line up.

Use it for software subscriptions, online advertising, travel, fuel, office supplies, and recurring vendor charges that can be cleared inside the billing cycle. That's where the grace-period structure has value. Verified guidance notes that business credit cards can provide interest-free grace periods, typically 21 to 30 days, when balances are repaid in full, while lines of credit begin accruing interest immediately on draws (SoFi comparison details).

Use the card when the expense behaves like an operating expense, not a financing event.

A few situations clearly favor the card:

- Recurring software bills: Clean automation and easy reconciliation.

- Travel and entertainment: Simple employee use and centralized oversight.

- Small fast purchases: No draw request, no separate cash movement.

- Short-cycle spend: Best when you know repayment is coming before the statement due date.

This quick explainer adds a useful visual overview:

Use a line of credit for cash based needs

A line of credit is the better instrument when the money needs to move into your operating account and then out to payroll, suppliers, or vendors who aren't set up for card payments.

That includes:

- Inventory buys: Especially when you need quantity now and repayment will track sell-through.

- Payroll bridging: The card is a poor substitute for payroll funding.

- Vendor invoices: Direct cash obligations usually belong on the line.

- Emergency operating needs: Repairs, disruptions, or timing gaps that require cash flexibility.

The key difference is that with a line, you pay interest only on the amount you use. That makes it more efficient for episodic larger needs than trying to force everything through a card program.

Use both when the business is sophisticated enough

Many established companies should stop framing this as an either-or choice. They need both, with clear rules.

Use the card for transaction-heavy spend that should be cleared quickly. Keep the line for working capital gaps, inventory swings, and larger tactical draws. Separate the two in your internal finance policy so nobody uses a card for disguised term borrowing or taps the line for sloppy routine spend.

If you expect to carry the balance, don't put it on the card just because the transaction is easy.

That rule alone prevents a lot of bad decisions.

Your Decision Framework and How to Apply

If you strip away marketing language, the decision comes down to fit, cost, and control.

A simple decision matrix

Use this matrix to decide quickly:

| If your priority is | Better tool |

|---|---|

| Everyday operating purchases | Business credit card |

| Large irregular cash needs | Business line of credit |

| Fast merchant payment convenience | Business credit card |

| Lower cost on carried balances | Business line of credit |

| Short-term spending repaid within the cycle | Business credit card |

| Payroll, inventory, vendor cash obligations | Business line of credit |

Now pressure-test the answer with these questions:

- How will the funds be used? Merchant purchase or operating cash?

- How long will repayment take? Days and weeks, or longer?

- Do fees change the economics? Especially for low-use standby lines.

- Will utilization spike at a bad time? If yes, manage draws carefully.

- Does your team need access, or does finance need control? Those are different operating needs.

If you're a more experienced borrower, use a blunt standard. A card is for spending. A line is for financing. Keep those functions separate unless you have a specific reason not to.

What to prepare before you apply

The businesses that get the best outcomes usually show up organized.

For either product, lenders or issuers will care about the same broad themes: cash flow quality, repayment capacity, and credit history. For a line of credit, expect a closer look because the lender is often taking more risk and offering more flexibility. For a card, the process is often lighter, but that doesn't mean the decision is casual.

Before applying, gather:

- Recent business financials: Clean numbers matter more than stories.

- Bank activity history: Lenders want to see how cash moves.

- Entity documents and ownership details: Keep legal and operating records current.

- A clear use-of-funds explanation: Especially for a line of credit.

- Internal repayment plan: Know how the balance gets cleared before you borrow.

Also decide in advance how you'll manage the account after approval. That part gets neglected. Set spending authority, define who can draw, establish repayment triggers, and decide what utilization level you won't exceed unless management signs off.

Borrowing discipline starts before approval. The lender just documents it.

The right product supports growth. The wrong one taxes it. If the expense is routine and short-lived, the card usually wins. If the need is larger, cash-based, or likely to remain outstanding, the line is usually the smarter instrument.

If you're ready to compare funding options without wasting time on a dozen separate applications, Business Loan Warrior gives you a practical path forward. You can check options through one no-fee application, review customized offers, and move toward a line of credit or other financing that fits your cash flow strategy instead of forcing your business into the wrong product.