Your sales report looks healthy. Your bank account doesn't.

That gap is where most small business stress lives. Payroll is due Friday, two large customers still haven't paid, inventory arrived earlier than expected, and a lender asks for updated financials right when cash feels tightest. On paper, the business is doing well. In real life, it feels like you're financing everyone else.

That's why working capital management matters so much. If you've ever asked, what is working capital management, the practical answer is simple: it's the discipline of making sure money moves through your business fast enough to support operations, absorb surprises, and make you look stronger to lenders.

Busy owners often focus on revenue, margins, and growth. Lenders look at those too, but they also study how well you manage short-term cash pressure. A company with solid sales and sloppy cash timing can still look risky. A company with tighter control over receivables, payables, and inventory often looks more fundable.

Table of Contents

- Why Revenue Is High But Cash Is Low

- Understanding Your Businesss Financial Engine

- The 5 Key Metrics That Tell Your Cash Story

- Actionable Strategies to Optimize Your Cash Flow

- Working Capital Management in Your Industry

- How Working Capital Determines Your Loan Readiness

- Get Your Business Funding Ready Today

Why Revenue Is High But Cash Is Low

You finish a strong month, see the sales numbers, and assume cash should be comfortable. Then payroll hits, suppliers need payment, rent clears, and the bank balance feels tighter than it should. That gap frustrates a lot of owners because the business looks healthy on paper while cash says something else.

The problem is usually timing.

Revenue records a sale when the work is done or the product ships. Cash only shows up when the customer pays. In the meantime, your money is often tied up in unpaid invoices, inventory sitting on shelves, or payment terms that favor customers more than they favor you. For owners focused on optimizing Shopify brand cash, this shows up fast during inventory buys, discount pushes, and seasonal ramps.

The money exists, but it is stuck in the cycle

I see this often with growing companies. Sales go up, but so do receivables, stock levels, and short-term obligations. The business is producing revenue, yet the cash is still traveling through the system.

A profitable company can still run short month to month.

That distinction matters to your lender and to your day-to-day operations. If cash is tied up for 45, 60, or 90 days, you may need outside financing to cover expenses you already earned your way into. That often means borrowing to bridge a gap created by operations, not by weak demand.

Here is what that usually looks like in practice:

- Open invoices keep piling up: You earned the revenue, but customers have not paid yet.

- Inventory is moving too slowly: Cash is sitting in product instead of covering obligations.

- Vendor and payroll deadlines arrive first: Money goes out on schedule, while customer payments come in late.

- Growth adds pressure: Higher sales can increase the amount of cash trapped in receivables and inventory.

If receivables are causing the squeeze, collections work is usually the fastest place to improve cash flow. This guide to accounts receivable management lays out practical ways to speed up payments without putting customer relationships at risk.

Why lenders focus on this gap

Lenders do not give much credit for revenue alone if liquidity is weak. They look at whether your business can convert sales into usable cash fast enough to cover debt payments, payroll, inventory purchases, and normal operating shocks.

Strong working capital management gives them a better answer. It shows that your business is not just generating sales. It is controlling the pace of cash in and cash out. That can improve your loan eligibility, reduce perceived risk, and put you in a stronger position when terms are on the table.

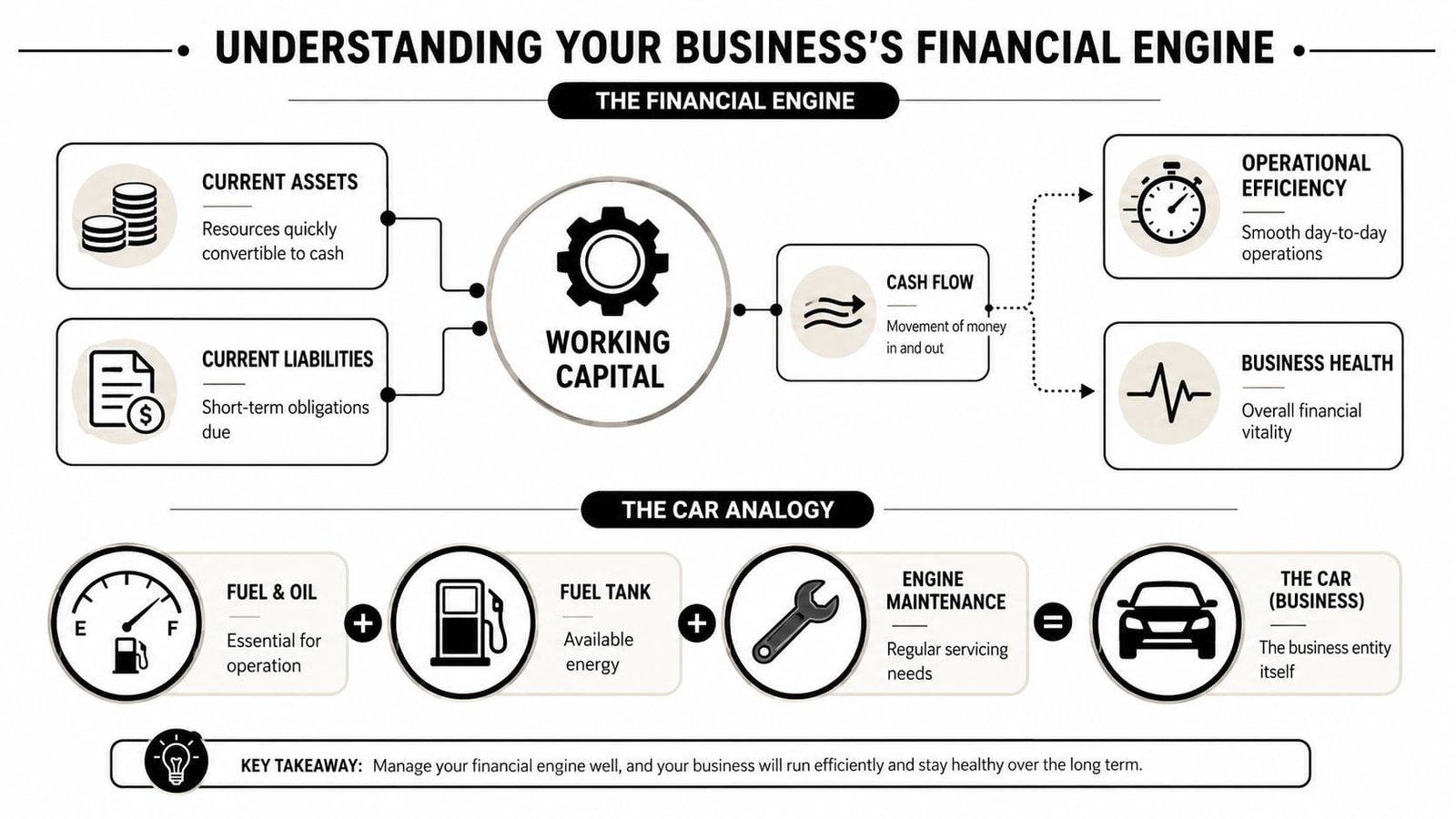

Understanding Your Businesss Financial Engine

To manage working capital well, treat it as the operating system behind your day-to-day cash decisions, not just a line on the balance sheet.

The formula that matters

The formula is simple. Working Capital = Current Assets – Current Liabilities. Current assets include cash, accounts receivable, and inventory. Current liabilities include accounts payable and short-term debt, as explained in this overview of working capital for small business owners.

What that formula answers is practical: after paying the bills coming due soon, how much room does the business have to keep operating without strain?

That answer affects more than daily comfort. It shapes whether you can buy inventory at the right time, cover payroll without scrambling, and show a lender that your business can absorb normal delays without missing a debt payment.

Working capital moves every day

Owners get into trouble when they treat working capital like a fixed score. In real businesses, it shifts constantly. Customer payments land early or late. Inventory turns fast or sits too long. Supplier bills hit before receivables clear.

That is why the key question behind "what is working capital management" is operational. How well do you control the timing gap between cash going out and cash coming back in?

If that gap stays tight, the business usually funds more of its own growth. If it stretches, outside financing starts covering ordinary operations instead of expansion. Lenders notice that difference immediately. A business that manages timing well looks safer than one with the same revenue but constant cash pressure.

A shorter cash conversion cycle can also strengthen your borrowing position, because it shows that cash does not stay trapped for long.

Good working capital is about control

Strong working capital does not always mean a large cash balance. In many cases, it means cash keeps circulating with discipline.

Here is what lenders and advisors want to see:

- Receivables convert on time: customers pay within terms, and overdue balances get attention quickly.

- Inventory earns its place: stock supports sales without tying up cash in slow-moving items.

- Payables are timed with intent: bills are paid according to plan, preserving vendor trust while protecting liquidity.

Practical rule: Ask how fast cash returns after you spend it, not just how much cash is in the account today.

That Revenued summary also notes that effective working capital management can reduce borrowing needs when receivables, payables, and inventory are handled efficiently. For a small business owner, that often means fewer short-term cash squeezes and a stronger case when applying for financing.

Why lenders care about your financial engine

Lenders do not underwrite profit alone. They assess how your business handles pressure between sale and collection.

If cash gets stuck in receivables or inventory, debt payments look riskier. If cash moves through the business in a predictable way, lenders have more confidence in repayment. That can improve loan eligibility and put you in a better position on rates, terms, and loan size.

Ultimately, the question "what is working capital management" is about the daily system that keeps your business liquid, stable, and financeable.

The 5 Key Metrics That Tell Your Cash Story

Most owners don't need fifty financial ratios. They need a short list that tells the truth about cash. These five metrics do that. They also happen to be the numbers many lenders and credit teams notice first.

A quick view of the key measures

| Metric | Formula | What It Measures | Healthy Benchmark |

|---|---|---|---|

| Current Ratio | Current Assets ÷ Current Liabilities | Ability to cover short-term obligations | 1.5 to 2.0 is typically healthy |

| Quick Ratio | (Current Assets – Inventory) ÷ Current Liabilities | Immediate liquidity without relying on inventory | Higher is generally stronger qualitatively |

| DSO | Accounts Receivable ÷ Credit Sales × days in period | How long customers take to pay | Lower is better qualitatively |

| DPO | Accounts Payable ÷ Cost of Goods Sold or purchases × days in period | How long you take to pay suppliers | Managed strategically, not maximized blindly |

| Inventory Turnover | Cost of Goods Sold ÷ Average Inventory | How efficiently inventory converts to sales | Higher turnover is generally stronger qualitatively |

Current ratio tells lenders whether you can breathe

The current ratio is the first checkpoint. It compares current assets to current liabilities. According to eCapital's working capital benchmark guide, a healthy working capital ratio is typically between 1.5 and 2.0, and ratios below 1.5 can signal liquidity risk.

That ratio matters because it's easy to interpret. If it's weak, lenders worry that ordinary operating obligations could crowd out loan repayment. If it's much higher than necessary, they may ask whether assets are sitting idle instead of generating returns.

Quick ratio strips out the least liquid piece

Inventory can be valuable, but it isn't always fast cash. The quick ratio removes inventory and asks a sharper question: if you had to cover short-term obligations using the assets closest to cash, could you?

For service firms, this ratio can be especially revealing because inventory is minimal. For product-based businesses, it can uncover an uncomfortable truth. A balance sheet can look healthy only because inventory is carrying the weight.

If your current ratio looks fine but your quick ratio looks thin, inventory may be hiding the problem.

DSO, DPO, and inventory turnover show operational discipline

Days Sales Outstanding (DSO) measures how long it takes to collect from customers. If it drifts upward, cash gets trapped in receivables. You may still post revenue, but your bank account won't feel it.

Days Payables Outstanding (DPO) measures how long you take to pay suppliers. Longer payment terms can support liquidity, but only if they're negotiated and intentional. Stretching vendors informally can damage supply relationships and create risk just when you need reliability.

Inventory turnover shows whether stock is moving or sitting. Slow turnover ties up cash and usually creates second-order problems: markdowns, storage pressure, and lower flexibility.

A useful deeper read is this article on turning your cash conversion cycle into a borrowing base advantage. It connects these operating metrics to how lenders evaluate collateral quality and cash efficiency.

What a lender sees behind the formula

Lenders don't read these numbers in isolation. They read them as behavior.

- A weak current ratio suggests limited room for error.

- A rising DSO suggests collections may be loose or customers may be stressed.

- An inflated DPO can mean smart payment management, or it can mean the business is delaying bills because cash is tight.

- Sluggish inventory turnover can signal poor forecasting, weak demand, or purchasing habits that lock up cash.

That's why these metrics matter more than broad statements like “sales are up.” The ratios tell the cash story behind the sales story.

Actionable Strategies to Optimize Your Cash Flow

Improving working capital usually comes down to three levers. Collect cash faster. Hold cash a little longer where appropriate. Stop unnecessary cash from sitting in stock.

Speed up receivables without creating friction

Receivables are often the cleanest place to improve quickly. Many owners tolerate slow payment because they don't want to appear aggressive. That usually backfires. Clear invoicing and consistent follow-up feel professional, not hostile.

A few tactics work well:

- Invoice immediately: Don't wait until week's end or month's end if the work is done now.

- Make payment easy: Include payment links, ACH options, or card options where appropriate.

- Offer selective early-payment incentives: Use them on large or chronically slow accounts when the economics make sense.

- Set credit boundaries: New customers don't always earn generous terms on day one.

For owners who want more tactical ideas on managing small business cash flow, that guide covers practical habits that help reduce cash surprises.

Control payables strategically

The goal isn't to pay everyone as late as possible. The goal is to pay according to negotiated terms while preserving liquidity.

Good payable management looks like this:

- Know your actual due dates. Too many businesses pay from habit instead of schedule.

- Segment vendors. Critical suppliers deserve tighter attention than low-risk vendors.

- Negotiate before you need help. Suppliers are more flexible when your account is current.

- Protect key relationships. Cheap liquidity from delaying the wrong vendor can become very expensive later.

Reduce cash trapped in inventory

Inventory is where optimism often turns into a cash problem. Owners buy for the sales they expect, not the sales pattern they can support. The answer isn't always cutting stock hard. It's buying with more precision.

That can include tighter reorder points, better forecasting by SKU, and a willingness to clear slow-moving items before they become dead weight. The right level depends on your business model, but the principle is universal: inventory should support sales, not drain flexibility.

Businesses that manage idle assets tightly can become more profitable and easier to finance at the same time.

That view is backed by National Center for the Middle Market research, which found that middle-market firms actively optimizing working capital to reduce idle assets achieved 12–15% higher cash-on-cash returns. That matters because it pushes against the old belief that more working capital is always safer.

The metric that ties it together

The big-picture measure is the cash conversion cycle, often shortened to CCC. It captures how long cash stays tied up between paying for operations and collecting from customers. Lower is better because cash comes back faster.

A short explainer is worth watching if you want the mechanics in plain language:

Some owners hear “low working capital” and assume danger. Sometimes it is danger. Sometimes it's a sign the business runs tightly and reinvests cash quickly. The difference is control. If low working capital comes from discipline, lenders may see efficiency. If it comes from chaos, they see distress.

Working Capital Management in Your Industry

Working capital doesn't feel the same in every business. The mechanics are universal, but the pressure points change by industry.

Restaurants live and die by timing

A restaurant can post strong weekend sales and still feel cash strain by Tuesday. Food inventory is perishable, labor is constant, and vendor payments don't pause just because a few slow weekdays hit. In that environment, working capital management means tight purchasing, close menu engineering, and watching waste as carefully as revenue.

A healthy restaurant operator usually reviews inventory movement constantly, not casually. If one ingredient sits too long, cash spoils along with it. If supplier terms are too tight, one slow week can create a real liquidity pinch.

Retailers get squeezed by shelves and seasons

Retail businesses often carry the most visible form of trapped cash. It's sitting in boxes, on racks, or in back-room stock. Seasonal buys make this harder. You need enough inventory to catch demand, but every extra unit delays cash conversion.

A retailer with discipline treats inventory like an investment portfolio. Fast sellers get priority. Slow movers get cleared. Purchasing adjusts to real sell-through, not just the hope that the season will bail out the buy.

In retail, excess inventory often looks like preparedness until the bank balance says otherwise.

Service firms usually struggle with receivables

Consultancies, agencies, contractors, and other service businesses typically don't have a warehouse problem. They have an invoicing and collections problem. Work gets delivered. Approval takes time. Billing gets delayed. Payment follows even later.

That means a service firm can look excellent on a profit and loss statement while staying under pressure in the checking account. The businesses that handle this well usually tighten scope approvals, bill milestones promptly, and avoid letting one large client dictate payment behavior for the whole company.

Same principle, different bottleneck

Across industries, the question is the same: where does cash get stuck first?

- Restaurants often need sharper control of perishables and daily cash commitments.

- Retailers usually need better inventory discipline and seasonal planning.

- Service businesses often need stronger invoicing rhythm and collection follow-through.

Once you identify the bottleneck, working capital management stops being abstract. It becomes an operating habit tied directly to survival, flexibility, and financing strength.

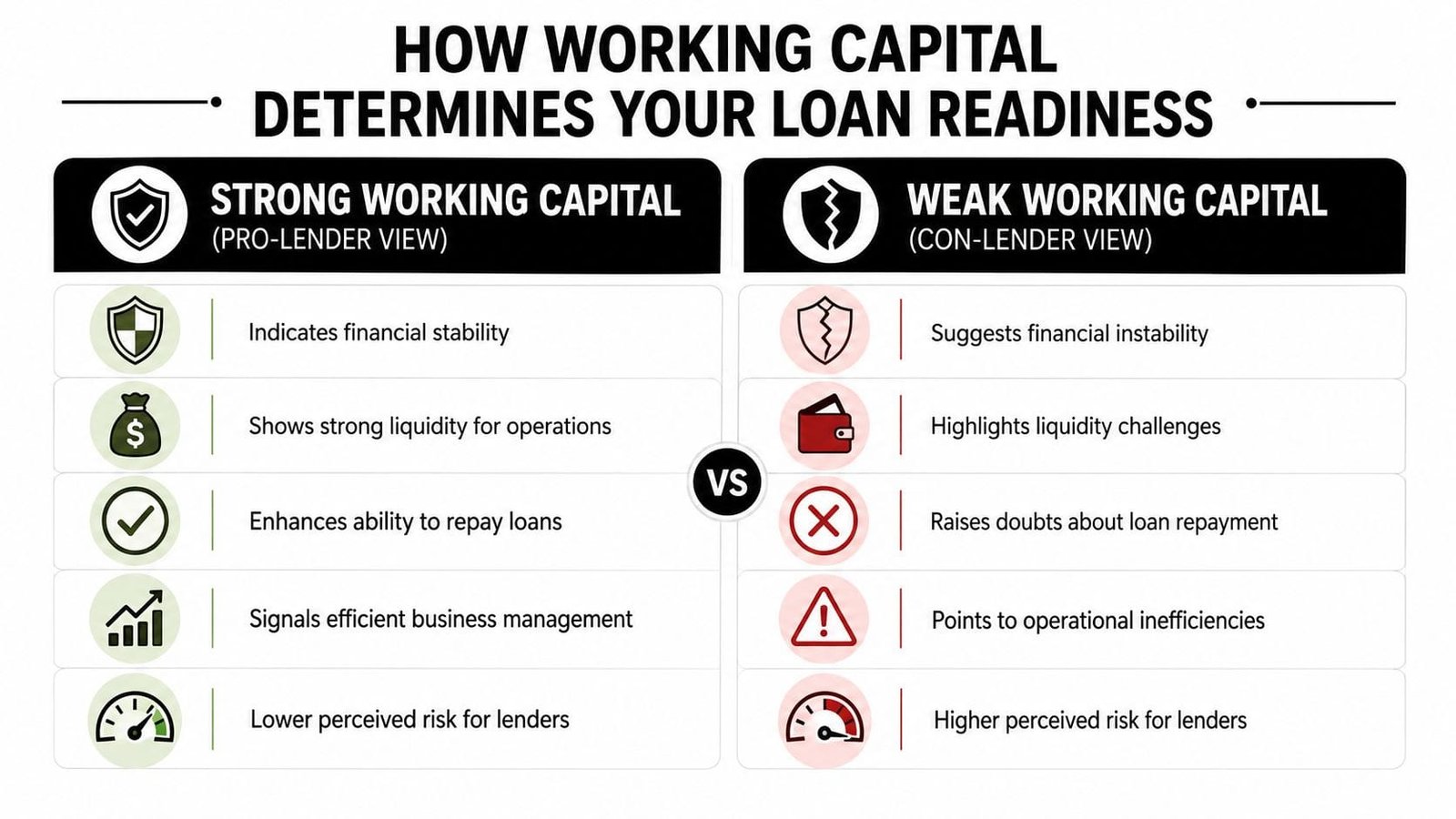

How Working Capital Determines Your Loan Readiness

A business can post strong sales, show a profit, and still make a lender uneasy. The reason is simple. Loans get repaid with cash, not with revenue on paper.

That is why working capital sits so close to the center of underwriting. Lenders want to see whether your business can cover payroll, suppliers, taxes, and debt payments without running short whenever timing slips. If receivables are aging, inventory is slow to turn, or payables are constantly under pressure, approval gets harder and pricing usually gets worse.

Strong working capital changes the lender conversation

Strong working capital signals control.

A lender reads it as evidence that management understands the operating cycle and has enough cushion to handle normal disruptions, like a late customer payment or a surprise vendor bill, without immediately depending on new debt. That lowers perceived risk. Lower risk often leads to a better conversation about structure, rate, term length, and borrowing capacity.

Weak working capital creates the opposite impression. Even if the business is profitable, the lender sees a company that may struggle to absorb routine timing gaps. As noted earlier, poor control of working capital can raise borrowing costs. The impact of that higher cost is significant. It does not just raise monthly payments. It also cuts into profit, reduces flexibility, and can make the next financing request tougher to support.

What lenders often flag

In credit review, a few warning signs come up again and again:

- Low liquidity: little room to handle payroll, vendors, and loan payments at the same time

- Slow collections: too much cash is stuck in overdue invoices

- Inventory drag: money is tied up in stock that is not converting quickly enough

- Reactive payables: bills are being stretched because cash is tight, not because terms are being managed strategically

If you want a practical benchmark, this guide explains what's a healthy working capital ratio and how it affects your loan approval.

Better working capital can improve terms, not just approval odds

Owners often treat loan readiness like a paperwork exercise. Lenders treat it like a cash discipline test.

I have seen two businesses with similar revenue get very different loan offers because one collected faster, carried cleaner inventory levels, and managed short-term obligations with a plan. The numbers told a clearer repayment story. That is what lenders want.

When your cash flow habits support your financial statements, the application gets easier to defend. You are no longer asking the lender to trust projected growth alone. You are showing that the business already converts operations into usable cash, which puts you in a stronger position to get approved and negotiate better terms.

Get Your Business Funding Ready Today

If your cash feels tight despite solid sales, don't start with more debt. Start with better working capital control.

Use a short checklist:

- Calculate your current position: Review current assets, current liabilities, and your working capital ratio.

- Pick one pressure point: Focus on receivables, payables, or inventory first. Don't try to fix everything at once.

- Track the right metrics consistently: Watch trends, not just month-end snapshots.

- Prepare your lender story: Be ready to explain how cash moves through the business and what you've improved.

Owners who do this before applying usually walk into the financing process with cleaner numbers, better answers, and fewer surprises.

If you want a faster way to check your options and present a cleaner funding profile, Business Loan Warrior helps small businesses explore customized financing through one no-fee application, track progress in a secure dashboard, and move toward funding with clearer visibility into approvals and repayment.