You close a strong month, book solid revenue, and still feel pressure on payroll, inventory, or vendor payments. That's the gap that catches a lot of growing companies. Sales happened, but cash hasn't landed.

That gap is where accounts receivable management either protects your business or strains it. If your team treats AR like simple bookkeeping, you'll keep chasing payments after problems show up. If you treat it like a working capital system, you'll collect faster, reduce friction with customers, and put yourself in a better position when you need financing.

For an SMB moving toward upper-mid-market complexity, that shift matters. The difference between a clean receivables process and a messy one isn't just administrative. It affects how confidently you can hire, how much cushion you have in a slow month, and how credible your business looks to lenders and financing partners.

Table of Contents

- Why AR Management Is Your Cash Flow Engine

- Building Your Foundational AR and Credit Policy

- Optimizing Your Invoicing and Collections Workflow

- Tracking the AR Metrics That Truly Matter

- When to Automate Accounts Receivable with Software

- Leverage Strong AR for Better Business Financing

Why AR Management Is Your Cash Flow Engine

A sale isn't cash. It's a promise to pay. Until that promise turns into money in your account, your business is funding the gap.

That's why accounts receivable management deserves executive attention. It sits between revenue and liquidity. Strong AR keeps payroll predictable, gives you room to buy inventory at the right time, and reduces the odds that you'll lean on expensive short-term capital just to bridge routine delays.

In practice, this isn't a small-volume clerical task. The average mid- to upper-mid-market AR team processes nearly 2,500 invoices per month, and firms with mature order-to-cash processes and AR software can achieve 30% faster cash conversion cycles and 50% fewer write-offs, according to Versapay's accounts receivable statistics. Those numbers explain why serious operators don't leave AR to disconnected spreadsheets and occasional follow-up emails.

Revenue on paper versus cash in hand

Owners often focus on margin, pipeline, and top-line growth. All of that matters. But if your receivables process is loose, growth can make pressure worse, not better.

A fast-growing company usually extends more credit, sends more invoices, handles more exceptions, and absorbs more customer-specific billing requirements. If those pieces aren't controlled, the finance team spends more time fixing preventable problems than collecting cash.

Strong AR doesn't just reduce bad debt. It gives management control over timing, and timing is what keeps a growing business stable.

Why this matters before you need funding

Well-run receivables improve optionality. A clean AR operation can make internal cash flow stronger, but it also strengthens your position when you explore working capital solutions tied to invoices.

If you're already trying to improve cash flow in your business, AR is one of the first operating levers worth tightening. It's often faster to improve collections discipline than to renegotiate every vendor term or raise outside capital.

Building Your Foundational AR and Credit Policy

Most receivables problems start before the invoice goes out. They start when a business extends credit casually, gives unclear terms, or leaves exceptions to whoever wants to close the deal fastest.

A disciplined AR process begins with a formal credit policy. JPMorgan recommends setting credit terms at onboarding and sending accurate invoices immediately to reduce disputes and speed cash conversion. It also warns that manual processes increase human error, as outlined in JPMorgan's guide to accounts receivable management.

What your policy needs to cover

Your policy doesn't need to be long. It needs to be clear, enforceable, and used by sales, finance, and operations.

Include these essential elements:

- Customer approval rules: Define who can approve new credit, what documentation you require, and when an exception must go to leadership.

- Payment terms: State whether you use Net 30, Net 45, Net 60, deposits, milestone billing, or other structures by customer type.

- Credit limits: Set a ceiling for open exposure before new work, new shipments, or renewals require review.

- Invoice requirements: List the exact billing details needed, such as PO number, billing contact, legal entity name, delivery confirmation, and payment instructions.

- Late-payment procedure: Spell out reminder timing, escalation path, and who owns outreach at each stage.

- Dispute ownership: Identify who resolves pricing, service, quantity, or documentation disputes so they don't sit in limbo.

The trade-off in setting terms

Terms shape sales and risk at the same time. If you're too strict, you can slow new business. If you're too loose, you may win deals that strain cash and create collection work your team can't support.

A simple approach works well for SMBs:

| Policy area | Conservative approach | Flexible approach | Trade-off |

|---|---|---|---|

| New customers | Shorter terms or deposit | Standard credit terms early | Lower risk versus easier conversion |

| Large orders | Credit review before fulfillment | Faster release with limited review | More control versus faster sales cycle |

| Exceptions | CFO approval required | Sales-led exceptions | Better discipline versus more inconsistency |

Build the policy around actual behavior

A policy that lives in a PDF and nowhere else won't protect you. The strongest version sits inside your workflow.

That means your CRM, accounting system, or ERP should reflect approved terms, billing contacts, customer-specific requirements, and escalation notes. If sales promises one thing, fulfillment documents another, and accounting invoices a third, your collections team inherits avoidable friction.

Practical rule: If your collector has to ask, “What were the agreed terms?” after the invoice is sent, the process already failed upstream.

A simple credit policy checklist

Use this as a working draft for your business:

- Define who gets credit and who prepays.

- Assign standard terms by customer type or risk level.

- Set required billing fields before work starts.

- Cap open exposure with a review threshold.

- Create an exception path for strategic accounts.

- Document escalation steps for overdue invoices.

- Review customer history regularly and adjust terms when behavior changes.

Good AR collections feel easier when the setup is right. Bad AR collections usually trace back to weak setup, inconsistent terms, or poor documentation.

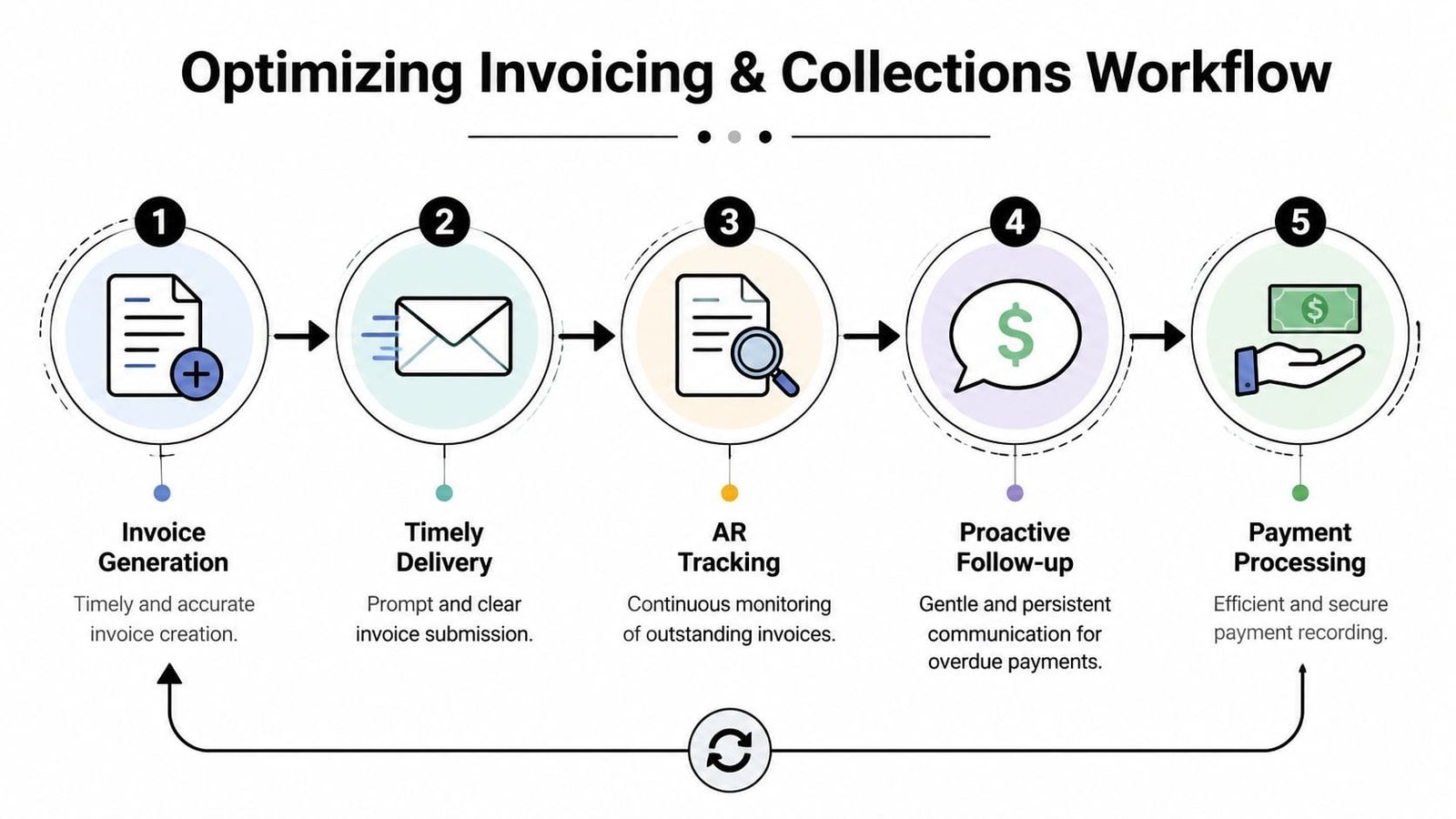

Optimizing Your Invoicing and Collections Workflow

A clean policy matters, but cash comes from execution. Your invoicing and collections workflow has to be repeatable, fast, and boring in the best way. If every invoice requires detective work and every overdue balance triggers a custom response, your team will stay reactive.

In the U.S., 39% of invoices are paid late, and businesses in the Americas can lose 51.9% of receivables that remain unpaid after 90 days, according to Sage's accounts receivable management data. That's why professional follow-up isn't optional.

Get the invoice right the first time

Many businesses blame customers for paying slowly when the invoice itself caused the delay. If the billing address is wrong, the PO number is missing, or the payment instructions are unclear, you're not in collections yet. You're still fixing billing.

Every invoice should include:

- Clear customer details: Correct legal entity, billing contact, and delivery location if relevant.

- Reference information: PO number, project code, contract reference, or service dates when the customer requires them.

- Simple due date language: Don't rely on vague terms alone. Show the actual due date on the invoice.

- Payment instructions: State accepted payment methods and where the customer should send remittance details.

- Support contact: Give customers one place to raise billing issues fast.

Use a time-based collections cadence

Collections work best when they feel routine, not emotional. The goal isn't pressure for its own sake. The goal is to keep the invoice visible and surface problems early.

A practical cadence for many SMBs looks like this:

- Before due date: Send a friendly reminder with invoice copy and payment options.

- On due date: Confirm the invoice is now due and invite the customer to flag any issue immediately.

- Shortly after due date: Follow up with a direct but professional note asking for payment status.

- As balances age: Move from reminder language to commitment language. Ask for a payment date, not just “an update.”

- For older items: Escalate internally and externally. Involve account management when the relationship matters.

“We're checking on invoice [number]. If payment is already in process, please share the scheduled date so we can update our records.”

Collections rule: Ask for a specific payment date. Open-ended requests create open-ended delays.

Sample outreach your team can copy

Pre-due reminder

Hi [Name], sharing invoice [number] ahead of the due date on [date]. I've attached the invoice for convenience. If your team needs any supporting documents to process payment, let us know now so there's no delay.

Past-due follow-up

Hi [Name], invoice [number] is now past due. Can you confirm payment status and the expected payment date? If there's a billing issue, send the details today and we'll route it to the right owner.

Escalation message

We haven't received payment or a firm status update on the overdue balance. Please confirm the payment date today. If there's a dispute, list each item holding payment so we can address it directly.

Separate promises from disputes

One of the most common mistakes in accounts receivable management is treating all overdue invoices the same. Some customers intend to pay but are slow. Others are blocked by an unresolved dispute. Those require different handling.

If the issue is documentation, fix it fast. If the issue is approval, identify the approver. If the issue is ability to pay, your team needs a different credit conversation. A collector who can't tell the difference will waste time sending reminders to invoices that can't move yet.

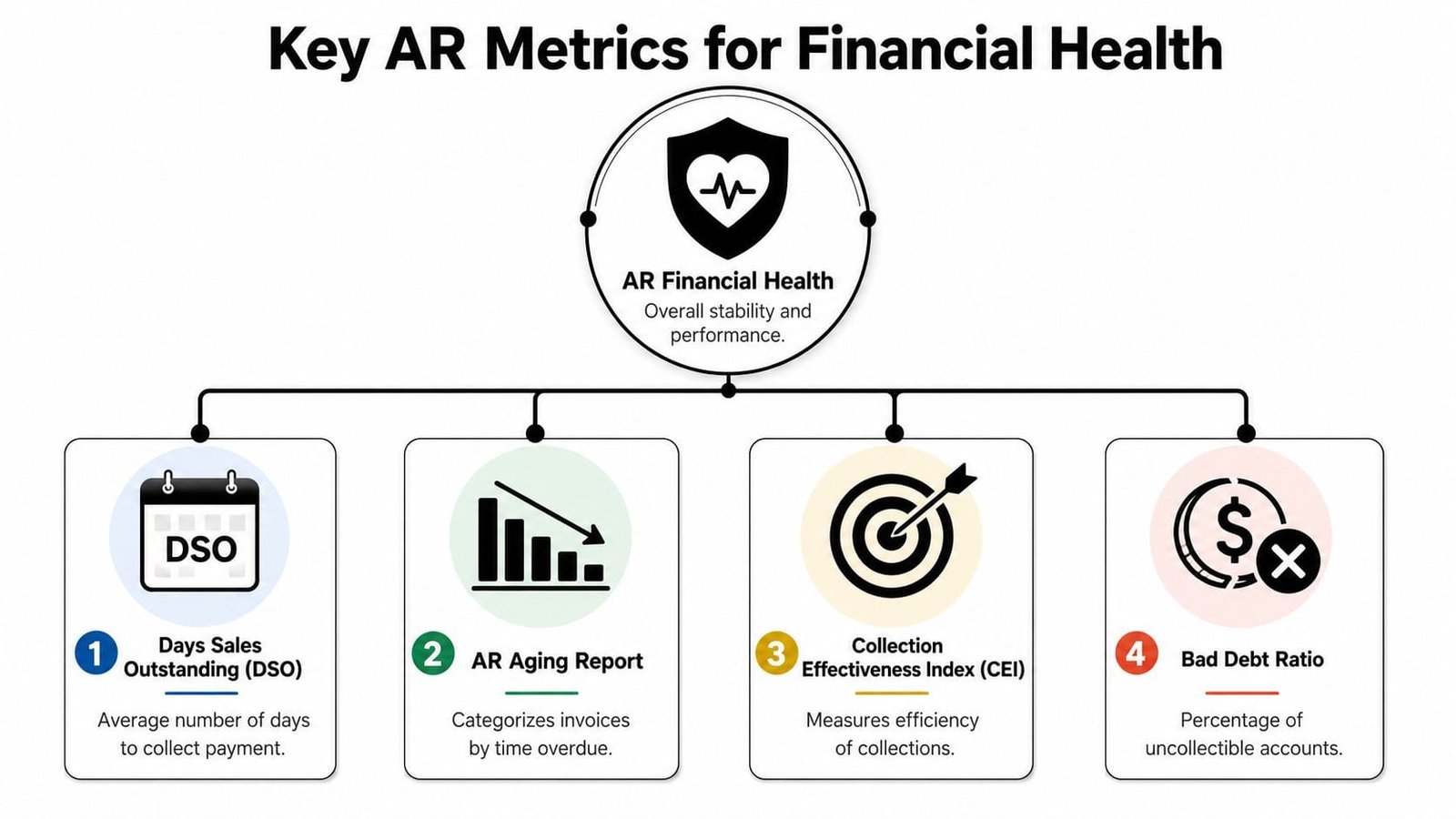

Tracking the AR Metrics That Truly Matter

Most owners have more reporting than they need and less clarity than they want. AR metrics should help you decide where cash is stuck, which accounts need attention, and whether the process itself is improving.

The most useful shift is to stop looking at receivables as one large balance. Break them into indicators that tell you what's current, what's slipping, and what's blocked by operational issues rather than customer unwillingness to pay.

Read DSO as a cash signal

Days Sales Outstanding, or DSO, tells you how long it takes to collect after a credit sale. The basic formula is:

DSO = (Accounts Receivable ÷ Total Net Credit Sales) × Number of Days

On its own, DSO isn't a verdict. It's a signal. A rising DSO often means one of three things: invoicing is delayed, collections are inconsistent, or disputes are slowing conversion from billed revenue to cash.

Use aging to direct action

Your aging report is where AR becomes operational. It sorts open invoices into time buckets so your team can prioritize effort.

If a customer always pays a little late but stays inside an acceptable pattern, that's different from a customer with invoices drifting into older buckets because of recurring billing disputes. Aging shows both patterns quickly.

For businesses preparing for credit review or financing, it also helps to understand how lenders read that report. A clean narrative around overdue balances matters. This guide on writing the AR aging narrative your lender wants to read is useful if you need to explain what's collectible versus what's at risk.

Aging becomes more powerful when you pair it with exception tracking. If a balance sits overdue because remittance can't be matched or a deduction hasn't been resolved, your issue isn't just collections. It's process quality.

The most actionable lever in AR is cash application and dispute control, because that determines how quickly billed revenue becomes usable cash. Best practice includes multiple payment rails and automated remittance capture, with benchmarks like 95%+ straight-through processing noted in HighRadius on accounts receivable management.

Here's a quick explainer before the table below.

Build a small dashboard your team will actually use

You don't need twenty KPIs. You need a handful that trigger action.

| KPI | What It Measures | How to Calculate | Why It Matters |

|---|---|---|---|

| Days Sales Outstanding (DSO) | Average time to collect after a sale | (Accounts Receivable ÷ Total Net Credit Sales) × Number of Days | Shows whether cash conversion is getting faster or slower |

| AR Aging Report | How long invoices have remained unpaid | Categorize open invoices by time bucket | Helps prioritize collections and spot risk concentrations |

| Collection Effectiveness Index (CEI) | How effectively the team collects eligible receivables | Use your internal CEI formula consistently each period | Isolates collections performance better than raw balance review |

| Bad Debt Ratio | Share of receivables that become uncollectible | Compare write-offs to credit sales using your finance policy | Shows whether credit quality and dispute control are weakening |

If DSO looks acceptable but old aging buckets are growing, don't relax. That usually means current volume is masking deeper collection problems.

A practical AR dashboard should be reviewed weekly by finance and regularly with sales or account management when customer behavior affects renewals, shipments, or service delivery.

When to Automate Accounts Receivable with Software

The right time to automate isn't when your team is completely overwhelmed. It's when manual work starts distorting cash flow, creating errors, or pulling skilled staff into repetitive follow-up instead of exception handling.

A lot of growing companies wait too long because spreadsheets still “work.” What they usually mean is that the process hasn't broken loudly enough yet. But the warning signs show up early. Invoices go out late. Collections notes live in inboxes. Customer promises aren't visible to the rest of the team. Cash application takes too long because remittance details arrive in different formats.

The operating model is changing quickly. 73% of finance leaders expect AI to be embedded in accounts receivable or collections workflows within the next three years, according to Sallyport Commercial Finance on mastering accounts receivable management. For SMBs, that doesn't mean you need a complex enterprise stack tomorrow. It means the old model of patching growth with more manual effort is getting harder to justify.

The manual breaking point

You should seriously evaluate automation when these conditions appear together:

- Invoice volume is climbing: The team spends too much time generating, checking, and resending invoices.

- Follow-up depends on memory: Collectors or bookkeepers decide what to chase based on inbox search rather than a work queue.

- Cash posting is delayed: Payments arrive, but matching and posting lags behind because remittance data is messy.

- Disputes disappear into email threads: Nobody can quickly tell what's unresolved or who owns the next step.

- Reporting takes manual assembly: Leadership gets AR visibility late, and by then the underlying issue is older and harder to fix.

What to automate first

You don't need to automate everything at once. Start with the pieces that remove friction from collection and visibility.

A sensible order for many SMBs is:

- Invoice generation and delivery from your accounting or ERP system.

- Automated reminder sequences tied to due dates and aging stages.

- Online payment options and customer-facing payment instructions to reduce payment friction.

- Cash application support so incoming payments are matched and posted faster.

- Dispute tracking with clear ownership and status.

That path usually creates more value than buying an advanced platform and turning on every feature immediately.

Where owners overdo it

Some businesses automate the customer-facing side and ignore the control side. That creates polished reminders but poor internal execution. Others push every account into the same automated sequence and damage relationships with valuable customers who need a more coordinated touch from sales or account management.

Automation should handle routine follow-up and repetitive matching. People should handle exceptions, customer context, and judgment calls.

The best software setup is the one your team will use every day. For some companies, that starts with stronger workflow inside QuickBooks, NetSuite, or another accounting platform. For others, a dedicated AR automation tool makes sense once invoice volume, payment complexity, and dispute handling outgrow basic accounting features.

If you're deciding whether the software cost is worth it, compare it against the cost of slower cash, preventable write-offs, and staff time spent cleaning up avoidable mistakes. That's the true comparison.

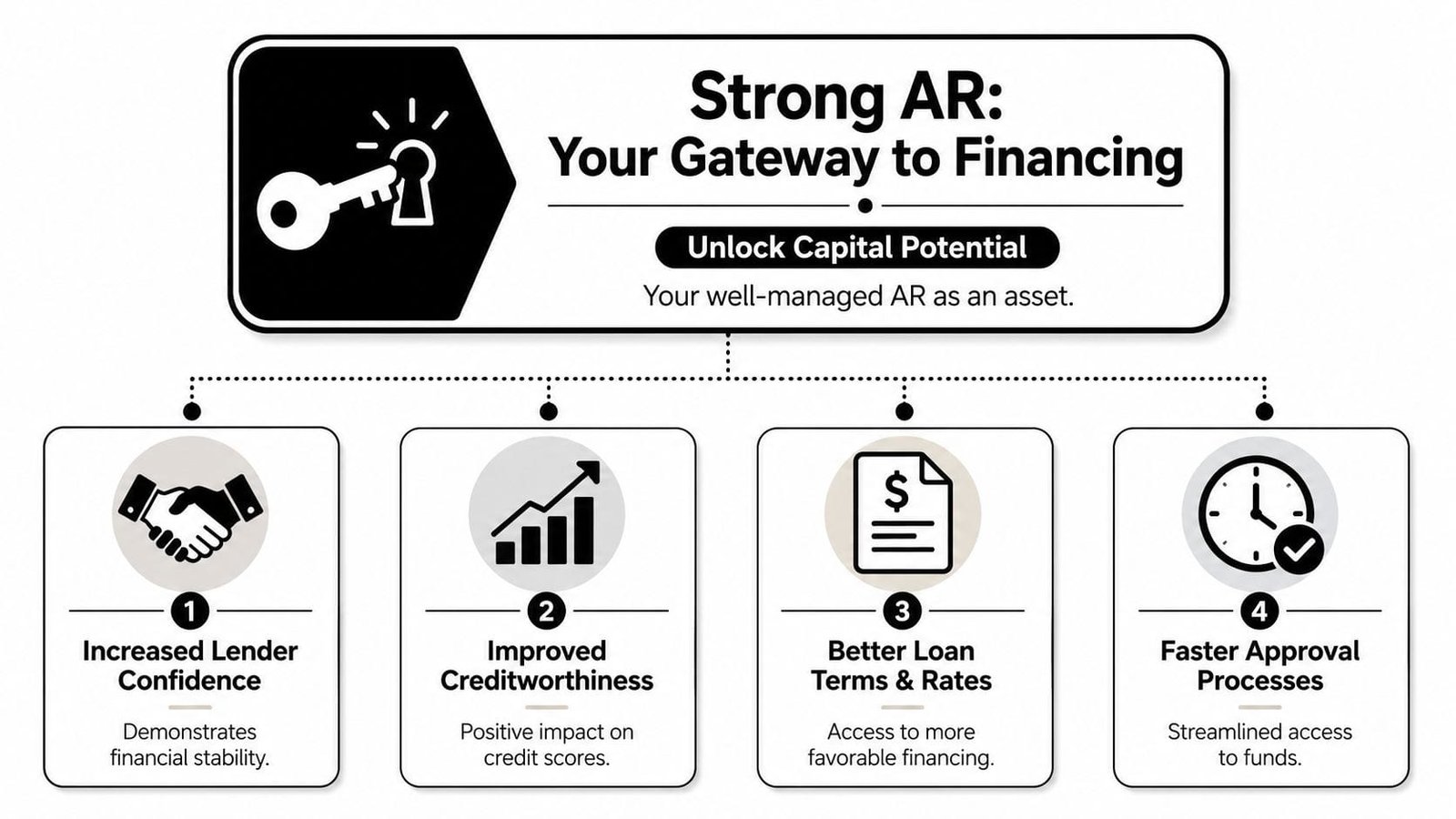

Leverage Strong AR for Better Business Financing

A familiar growth problem looks like this. Sales are up, payroll is due, inventory needs to be ordered, and too much cash is still sitting in invoices that should have been collected already. At that point, financing gets judged on the quality of your receivables, not just your revenue.

Receivables can support borrowing when they are current, documented, and collectible. If they are messy, aged, or tied up in disputes, they stop being a useful asset in a lender's eyes. That difference affects how much capital you can access, how quickly you can get it, and what it costs.

Lenders and finance partners review AR because it shows how your business converts sales into cash. They want to see whether customers pay on a predictable cycle, whether invoices are issued correctly, and whether your ledger matches reality.

What lenders want to see in receivables

A finance-ready AR file usually includes:

- Clean aging: Past-due balances are explained, with old invoices reviewed instead of ignored.

- Accurate billing records: Invoices line up with contracts, purchase orders, delivery records, and approval requirements.

- Collection visibility: Your team can show what is current, what is disputed, and what has a realistic path to payment.

- Customer concentration awareness: You know if too much of your receivables base depends on a small number of customers.

- Accurate cash posting: Payments are applied correctly, so reported AR is credible.

Many SMBs often get caught between basic bookkeeping and lender expectations. The books may be technically closed each month, but the AR support behind them is too thin for a credit decision. Strong AR closes that gap and gives your business more financing options.

Invoice financing versus factoring

Owners often group these together, but the trade-offs are different.

Invoice financing lets you borrow against eligible invoices while your business keeps control of the customer relationship and collection process. That usually works better for companies that want to smooth cash timing without changing how customers interact with them.

Factoring involves selling invoices to a third party at a discount in exchange for faster cash. That can help when liquidity matters more than margin, or when internal collections are weak, but it changes the economics and can affect the customer experience.

The right choice depends on your gross margin, customer quality, concentration, dispute levels, and how much control you want to keep. If you are comparing options, review how accounts receivable financing works for business owners before cash pressure forces a rushed decision.

How to make your AR finance-ready

If outside capital may be part of your plan, prepare your receivables before you need funding:

- Reduce invoice errors: Missing documentation and billing disputes lower the value of the receivable.

- Keep aging notes current: Be ready to explain older balances customer by customer.

- Document payment behavior: Separate chronic slow payers from good customers dealing with one-off issues.

- Clear unapplied cash fast: Misposted receipts make the whole AR file harder to trust.

- Review eligibility early: Not every invoice or customer will qualify, so test fit before a cash crunch.

Well-run AR does more than improve reporting. It strengthens your borrowing position, shortens diligence, and gives you better odds of getting financing that matches how your cash moves.

If your business needs working capital tied to invoices, Business Loan Warrior can help you explore funding options through one no-fee application. You can check pre-approval without affecting credit, compare custom offers, and find financing that fits how your receivables move.