You submit a loan application, feel good about the numbers, then the lender comes back with the sentence nobody wants to read: they need stronger support on the file. Sometimes that means more income documentation. Sometimes it means more time in business. Often, it means they want a cosigner.

That moment can feel personal, but it usually isn't. Lenders are trying to reduce risk, and a cosigner can turn a weak or borderline application into an approvable one. The problem is that most advice stops at “ask a parent or close friend,” which isn't enough if your network is small, your relationships are complicated, or you want to handle the process without damaging trust.

A better approach is practical. You need to know who to ask, how to ask, what lenders look for, what warning signs to avoid, and how to protect the person helping you after they sign. That's how to find a cosigner responsibly, not just quickly.

Table of Contents

- Why You Might Need a Cosigner and What It Means

- Understand the Cosigner's Full Responsibility First

- Identifying and Vetting Potential Cosigners

- How to Prepare and Pitch Your Cosigner Request

- Finalizing the Loan and Protecting Your Cosigner

- What to Do When You Cannot Find a Cosigner

Why You Might Need a Cosigner and What It Means

A cosigner usually enters the picture when your application is close, but not strong enough on its own. That can happen if your credit history is thin, your income doesn't support the payment comfortably, your business cash flow is uneven, or your lender wants stronger backup on the file.

For a small business owner, this often happens during growth. You may have revenue coming in, customers paying, and a real use for capital, but the lender still sees a risk gap. A cosigner can help bridge that gap.

The key mindset shift is this. A cosigner is not a character reference. A cosigner is a financial backstop whose credit and finances help support your approval.

What a cosigner changes

When a lender allows cosigners, they're looking at more than your profile alone. They may consider the additional strength of the cosigner's credit, income, and overall financial stability. According to South Carolina Student Loan guidance on finding a cosigner, applicants should look for someone with good-to-excellent credit and solid finances, and success rates increase significantly when the cosigner has a credit score of 620 or higher for conventional loans.

That doesn't mean any person with decent credit will work. The right cosigner is someone who is both qualified and personally realistic about the responsibility.

A strong cosigner can improve approval odds. A poorly chosen cosigner can create stress, conflict, and a loan that shouldn't have been made in the first place.

When a cosigner is a smart move

A cosigner makes sense when:

- Your repayment plan is solid: You can afford the loan, but your profile doesn't fully show it yet.

- The loan has a clear purpose: Equipment, working capital, expansion, or refinancing high-cost debt are easier to explain than vague “business needs.”

- The relationship can handle candor: If you can't discuss risk, timing, and payment expectations openly, don't ask.

A cosigner is best used as a strategic tool. Not a shortcut, and not a last-minute panic move.

Understand the Cosigner's Full Responsibility First

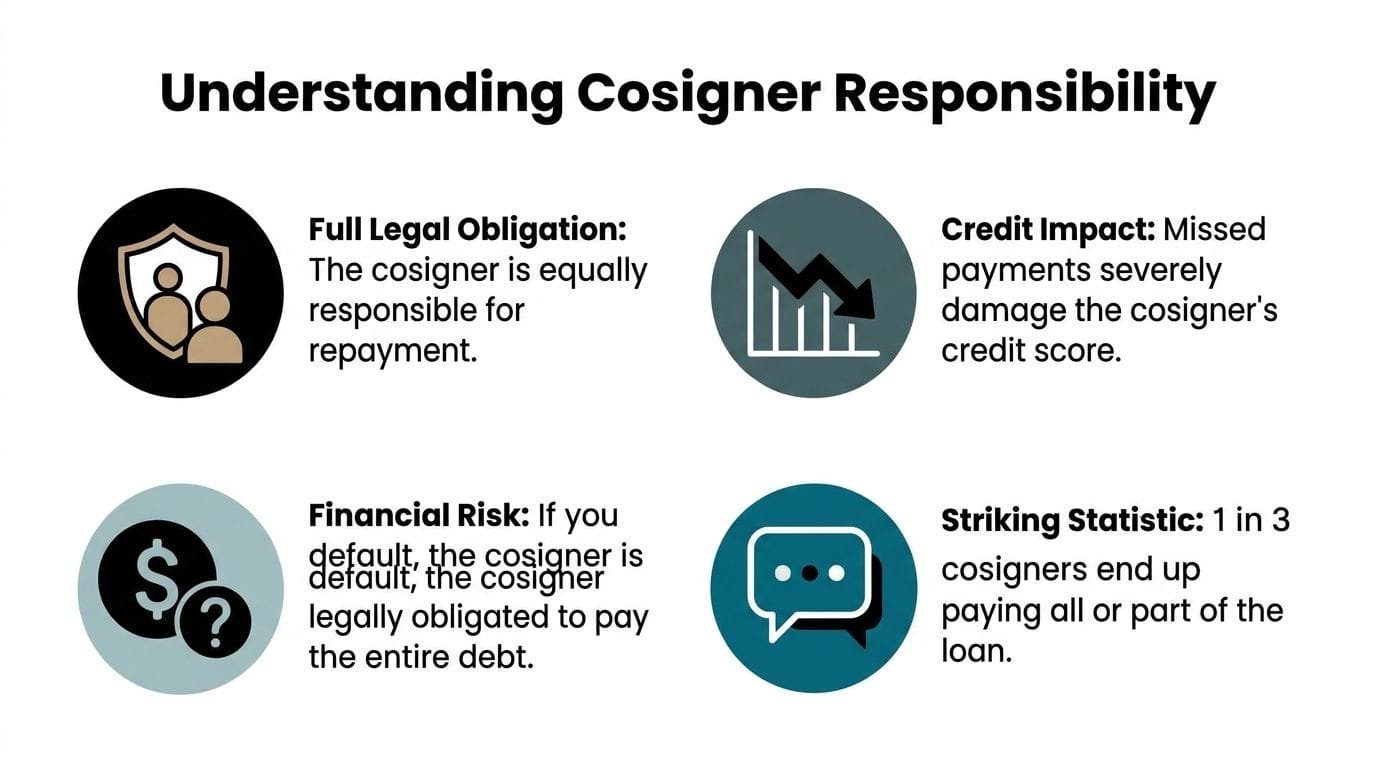

Before you ask anyone for help, get clear on what you're asking them to take on. Most borrowers explain the upside. Better approval odds, maybe better terms, faster funding. What gets skipped is the burden.

That's a serious mistake. The Federal Trade Commission says 68% of cosigners in the U.S. report being unaware of their full liability until they are contacted about a defaulted loan, according to its cosigning loan FAQ.

What the cosigner is actually agreeing to

If someone cosigns, they are not “supporting your application” in a casual sense. They are agreeing to be legally responsible for the debt if you don't pay.

That means a missed payment can affect them, not just you. It can also affect their ability to take on other borrowing because the loan may appear as an obligation connected to their credit profile.

If you want a plain-English legal overview, it helps to understand how guaranty agreements affect financial obligations. The details vary by lender and loan structure, but the practical point is simple. Signing creates enforceable responsibility.

Why transparency improves your odds

Borrowers sometimes try to soften the conversation. They say things like, “You'd probably never have to do anything,” or “This is just to help me get over the line.” That language usually backfires because it sounds evasive.

A stronger approach is direct:

- Tell them the full risk: If you fail to pay, they can be expected to pay.

- Explain the credit process: The initial rate check may be a soft pull that doesn't affect their credit score, as noted in the South Carolina Student Loan guidance already cited above.

- Acknowledge credit exposure: If you've never had to manage the consequences of late payments, review how late payments affect your credit score before you involve someone else's credit in the process.

Practical rule: Never ask for a cosignature until you can explain the worst-case scenario without minimizing it.

People say yes more often when they trust the borrower understands the stakes. Mature borrowers don't sell the dream. They present the facts, explain the plan, and leave room for an honest no.

Identifying and Vetting Potential Cosigners

Many individuals start with the wrong question. They ask, “Who likes me enough to help?” The better question is, “Who is both personally appropriate and financially qualified?”

That change matters. A willing person who can't meet lender standards won't help. A financially strong person who doesn't fully trust your repayment habits can damage the relationship even if they say yes.

Build the right short list

Start with a private list of people who have a reason to want you to succeed and enough financial stability to be considered. The South Carolina Student Loan guidance already referenced recommends focusing on family members, close friends, or mentors with good-to-excellent credit and solid finances. It also notes that a credit score of 620 or higher is a useful benchmark for conventional loans.

In practice, your list might include:

- A parent or sibling: Often the most common option, especially if they already understand your finances.

- A long-time friend: Best when the relationship is stable and both sides communicate well under stress.

- A business mentor: Sometimes the most rational option because the conversation stays more factual and less emotional.

- A spouse or partner: This can work, but only if both of you are aligned on household cash flow and risk tolerance.

Rocket Mortgage notes that some loan types have specific requirements, including 620 for conventional mortgages and 680 for jumbo loans, in its guide to cosigning a mortgage loan. Even outside mortgages, the lesson holds. Lenders usually want a cosigner whose credit profile clearly strengthens the file.

Choosing Your Cosigner Family vs. Friend

| Consideration | Asking a Family Member | Asking a Friend |

|---|---|---|

| Emotional history | Shared history can create trust, but it can also revive old tensions | Friends may bring less baggage, but the ask can feel more awkward |

| Financial visibility | Family may already know your income and debt habits | You may need to explain more from scratch |

| Boundaries | Expectations can get fuzzy if nobody puts terms in writing | Friends often do better with explicit boundaries |

| Risk to the relationship | Holiday-table conflict is real if payments slip | A friendship can end quickly if trust breaks |

| Ease of saying no | Some relatives feel pressured even when they shouldn't agree | Friends may feel freer to decline |

Ask the person who can make a calm decision, not the person most likely to feel guilty.

Red flags when someone offers to cosign for a fee

If you're researching how to find a cosigner online, you'll run into “services” and individuals who promise fast approval. Be careful.

Rocket Mortgage warns that cosigners who offer large upfront fees or guarantee approval for everyone are red flags. That's enough reason to walk away. A real cosigner is taking risk. They are not selling approval like a product.

If you want to verify who you're dealing with before entering any sensitive financial arrangement, a practical screening step is reviewing a 2026 background service comparison to understand the kinds of checks available. Use that kind of resource to think through due diligence, not to replace common sense.

What usually works:

- trusted personal relationships

- documented financial discussions

- lender confirmation that cosigners are allowed

What usually doesn't:

- strangers offering approval

- pressure to pay upfront

- anyone promising “guaranteed” outcomes

How to Prepare and Pitch Your Cosigner Request

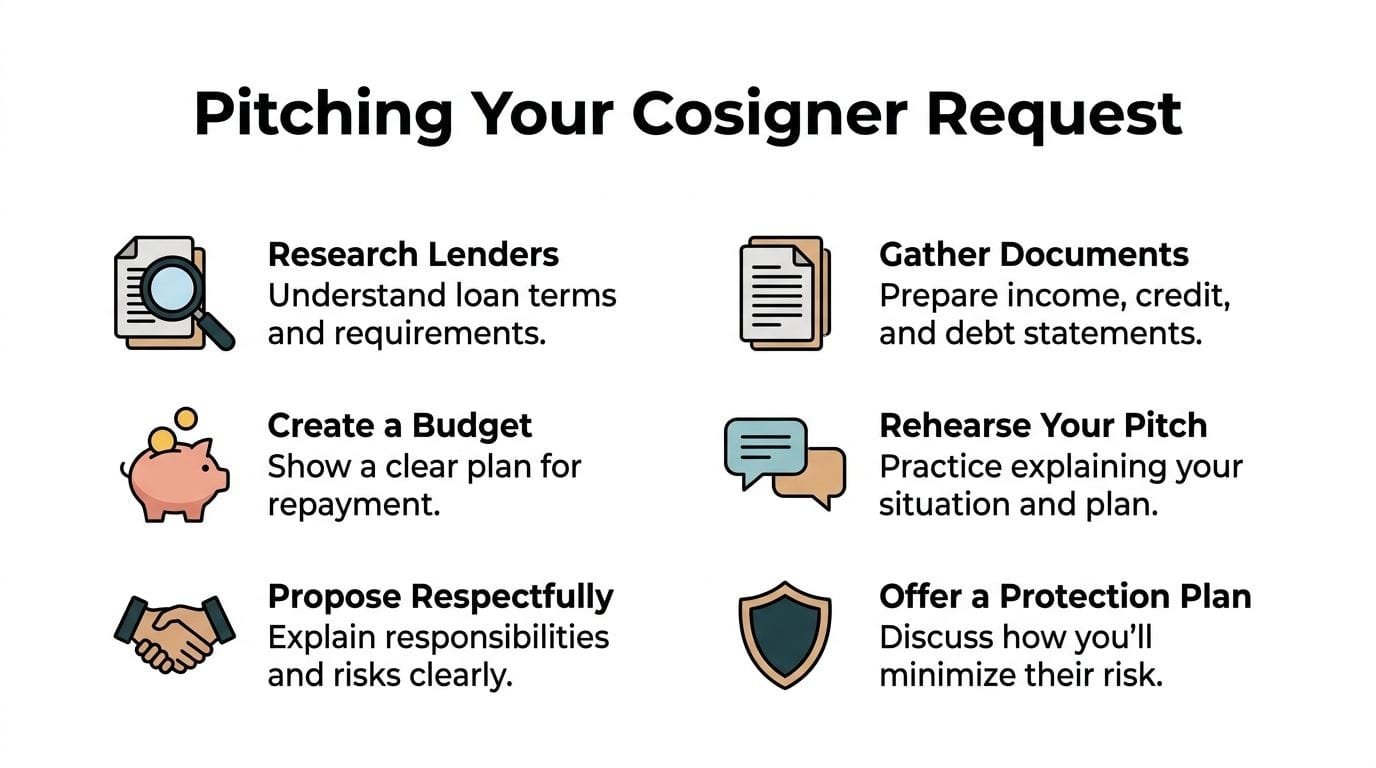

The ask should feel like a loan presentation, not a favor request delivered over text. If you show up unprepared, the other person has to do all the risk analysis themselves. Many will not.

Start by assembling your materials before you schedule the conversation.

Build a cosigner proposal before you ask

Bring order to the discussion with a short packet, digital or printed. It doesn't need to look fancy. It needs to answer the questions a careful cosigner will have.

Include these items:

Loan purpose

Explain exactly why you need the money. “Working capital” is less persuasive than “inventory for seasonal demand,” “equipment replacement,” or “debt consolidation to stabilize payments.”Requested terms

Show the lender type, estimated loan amount, expected payment range, and whether the lender allows cosigners. Don't assume all lenders do. The South Carolina Student Loan guidance cited earlier notes that not all lenders accept cosigners, so confirm eligibility before collecting paperwork.Your repayment plan

Spell out where the payment will come from. Revenue, retained cash, contract income, or payroll from another source. If your answer is vague, your request is weak.Current financial snapshot

Prepare recent pay stubs if applicable, proof of identity, and any other documents the lender may require from both parties. That same South Carolina Student Loan guidance specifically mentions gathering documentation like pay stubs and proof of identity for both borrower and cosigner.Your risk controls

Show what you'll do if cash flow gets tight. That might mean cutting discretionary expenses, drawing from savings, or paying this obligation before lower-priority spending.

This video gives a useful overview of how people approach the conversation in real life.

How to handle the conversation well

Ask for time to talk privately. Don't spring it on someone during a family dinner or in the middle of a workday. Give them room to think.

A simple opening works best:

I'm applying for a loan for a specific purpose, and the lender may require a cosigner. I want to show you the exact terms, the repayment plan, and the risks before you decide anything.

That script works because it signals respect. You're not asking for blind trust. You're offering clarity.

A few practical rules help:

- Lead with the risk early: Don't hide responsibility until the end.

- Use real documents: Verbal reassurance is weaker than a clear budget and loan summary.

- Invite hard questions: If they ask about late payments, income drops, or exit plans, that's a good sign.

- Accept no cleanly: If they decline, thank them and leave it there. Pressure destroys trust.

Some borrowers talk too much when they get nervous. The strongest pitch is usually the shortest one that answers the real risks.

What often gets a yes is not persuasion. It's preparation. People are more comfortable helping when they see you've already done the uncomfortable work yourself.

Finalizing the Loan and Protecting Your Cosigner

Once someone agrees, slow down and tighten the process. Approval isn't the finish line. At this point, borrowers either protect the relationship or create problems that last for years.

What both of you should do before signing

Read the lender's application and disclosures together. Confirm whether the first credit check is a soft pull, what documents are needed, and whether there are any conditions for future release. Don't rely on assumptions from another lender or another loan type.

Then create your own written side agreement. South Carolina Student Loan guidance recommends a formal document outlining payment deadlines, emergency savings plans, and communication protocols to prevent disputes. That's smart advice even when the cosigner is a parent or long-time business contact.

Your side agreement should cover:

- Due dates and payment method: Who pays, when, and from which account.

- Notification rules: When you'll tell the cosigner about any problem.

- Emergency backup: What happens if income drops unexpectedly.

- Exit goal: Refinancing, payoff, or another release strategy if available.

Set up protection after closing

The most overlooked part of how to find a cosigner is what happens after the loan funds. Protection is operational, not emotional.

Rocket Mortgage notes that for auto loans, each additional cosigner increases the incidence of default, and it recommends that lenders send monthly statements to the cosigner so they can intervene early in its previously cited guide. The practical takeaway is clear. More complexity usually increases risk, and silence makes problems worse.

Use that lesson immediately:

- Request duplicate monthly statements if available: The cosigner should see activity without having to chase you.

- Check in before there's a problem: A short monthly update protects trust.

- Keep reserves: Rocket Mortgage also recommends emergency savings equal to at least one loan payment in the same guide.

- Avoid stacking obligations carelessly: If you're trying to reduce personal exposure in other areas, study alternatives such as a business loan without personal guarantee before taking on new commitments.

The healthiest cosigner relationship is boring. Payments clear on time, statements match expectations, and nobody is surprised.

What to Do When You Cannot Find a Cosigner

Sometimes there is no one to ask. Not no one you trust. No one.

That situation is more common than a lot of financial advice admits. According to the source provided for this topic, 12% of U.S. adults ages 18 to 34 report being estranged from all family, which highlights how often “just ask family” fails as advice in real life, as noted in this discussion of where to find cosigners.

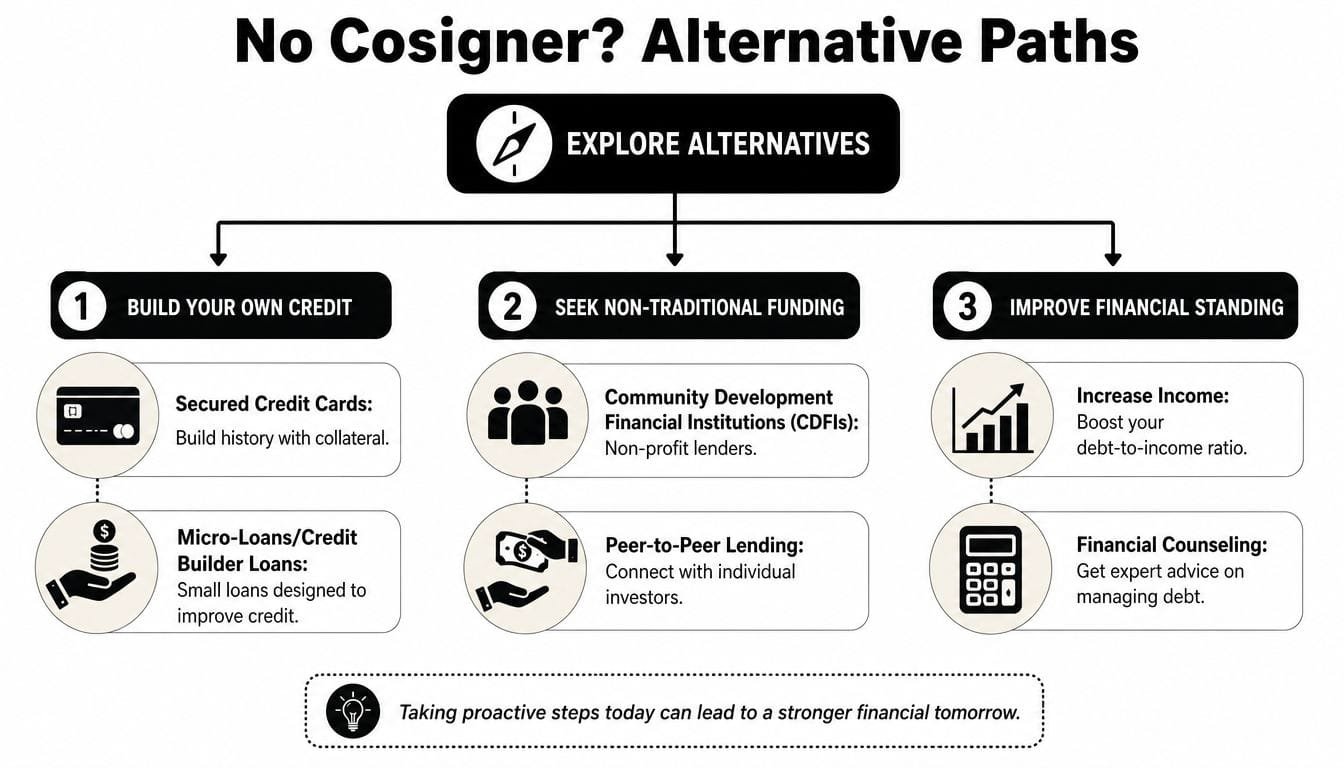

Alternatives if no one can sign with you

You still have options. They're different from a cosigned loan, but they can move you forward.

- Secured borrowing: If you have an asset the lender accepts, collateral can reduce the need for a cosigner.

- Credit union products: Some credit unions offer flexible small-dollar or credit-building loans that help you strengthen your profile over time.

- Community-based lending: Community nonprofit housing programs and other mission-driven lenders may serve borrowers who don't fit standard assumptions.

- Employment or income-based underwriting: Some lenders focus more on verified cash flow than on whether another person will sign with you.

If your credit file is the main obstacle, a better next move may be improving the application and coming back stronger. For borrowers working through damaged credit, these proven ways to secure small business funding even with bad credit can help you evaluate other funding paths.

How to improve your file for a later approval

If you can wait, use the time well.

Focus on the things lenders care about most:

- steadier income documentation

- lower existing debt pressure

- cleaner payment history

- stronger cash reserves

- clearer business use for the funds

No cosigner doesn't mean no path. It usually means your path is slower and more documentation-heavy.

A declined application with no cosigner can still be useful. It tells you what the lender didn't like. Fix that issue first, then reapply with a better file instead of repeating the same request.

If you need funding and want to explore options without turning your search into a hard-credit scramble, Business Loan Warrior gives business owners a practical place to compare paths, check pre-approval without affecting credit, and evaluate funding solutions that fit the actual condition of the business today.