An amortization period is the total time it takes to pay off a loan, and for business equipment loans it often falls in the 3 to 7 year range, while many residential mortgages run 15 to 30 years. It's one of the strongest levers you have to shape monthly cash flow, because stretching that payoff period usually lowers the payment but increases the total interest you'll pay over the life of the loan.

If you're reviewing financing offers right now, this is the point where many owners slow down. The approval feels like the hard part, but the actual financial consequence often sits in the repayment structure. Two loans can look similar on the surface and behave very differently once the payments start hitting your account each month.

That's why understanding what is amortization period matters so much. It tells you how long the debt is designed to be repaid, and that one detail affects whether the loan supports your working capital or squeezes it.

Table of Contents

- Your Loan Is Approved What Happens Next

- How Loan Amortization Works Principal vs Interest

- Amortization Period vs Loan Term Explained

- The Difference Between Loan and Accounting Amortization

- Sample Amortization Schedules for Business Loans

- How Amortization Impacts Your Cash Flow and Total Cost

- How to Choose the Right Amortization Period for Your Business

Your Loan Is Approved What Happens Next

You've got the approval email. The lender says the file looks good. Then the documents arrive, and suddenly the important questions aren't about getting the loan anymore. They're about how the loan is built.

Many business owners often focus on the rate and miss the structure. The amortization period is the total time the payments are spread over. In plain English, it's the runway your lender uses to calculate how quickly you pay back principal and interest.

That matters because your payment isn't just a bill. It's a monthly claim on your cash flow. A longer amortization period usually reduces payment pressure now, while a shorter one gets the debt off your books faster.

Why this term shows up in real business decisions

If you're financing equipment, expanding a location, or covering a short-term gap, the same question applies. How long should this debt stay in the business?

A useful way to think about it is this:

- Short runway: Higher payments, faster payoff, less financing drag over time.

- Long runway: Lower payments, more breathing room, but the debt stays with you longer.

- Wrong runway: Monthly payments may look manageable at first, but the structure can clash with your revenue cycle or the life of the asset.

For business borrowing, that last point is where expensive mistakes happen. Financing should fit the job. A truck, a kitchen buildout, and a working capital bridge don't all belong on the same repayment clock.

Practical rule: Match the repayment horizon to what the money is buying and how your business actually earns cash.

When owners ask what is amortization period, they're often really asking a better question underneath: “How will this loan behave after I sign?” That's the right instinct. Once funding lands, the payment structure becomes operational, not theoretical.

How Loan Amortization Works Principal vs Interest

Once the loan closes, your payment starts doing two jobs at the same time. One part covers interest, which is the lender's charge for the money you're using. The other reduces principal, which is the amount your business still owes.

That split changes over time.

At the start of the loan, the balance is at its highest, so the interest charge takes a larger share of each payment. As the balance comes down, the interest portion shrinks, and more of the same payment goes toward principal.

This is the part that often catches business owners off guard. You can make payments for months, stay perfectly current, and still see the balance drop more slowly than expected early on. Nothing is wrong with the loan. That is how amortization is designed to work.

What this looks like in real business borrowing

The pattern matters more when you compare the loan types you are considering.

With an SBA loan, the longer repayment structure usually keeps monthly payments lower, but a larger share of the early payments can go to interest because the balance stays outstanding longer. With an equipment loan, the schedule is often tighter, so principal may begin falling faster, which can make more sense when the asset has a defined useful life. With a short-term loan, payments are usually much heavier because the lender is compressing principal repayment into a much shorter window.

Same idea. Very different cash flow effect.

That is why amortization is not just a math detail. It shapes how much working capital stays in the business each month and how much total financing cost you carry over the life of the loan.

How to read an amortization schedule

An amortization schedule shows the loan one payment at a time. It tells you when each payment is due, how much goes to interest, how much goes to principal, and what balance remains after that payment.

When you review one, focus on four lines:

- Beginning balance: the amount used to calculate that period's interest

- Interest portion: the cost of carrying the loan for that payment period

- Principal portion: the amount that reduces what you owe

- Remaining balance: what stays on your books after the payment clears

If you want a simple way to plan your mortgage repayments effectively, a repayment calculator can help you see how payment length changes the mix of principal and interest. The same logic applies to business loans.

Why this matters before you sign

A payment amount by itself is incomplete. Two loans can have similar monthly payments and behave very differently underneath.

One may leave your balance falling slowly in the early years. Another may push down principal faster but put more strain on monthly cash flow. If you are choosing between SBA financing, equipment financing, or a short-term facility, the amortization schedule shows which trade-off you are making.

For a busy owner, that is the key takeaway. Principal versus interest is not accounting trivia. It tells you how fast the debt shrinks, how long interest keeps draining cash, and how much room your business keeps for payroll, inventory, hiring, and growth.

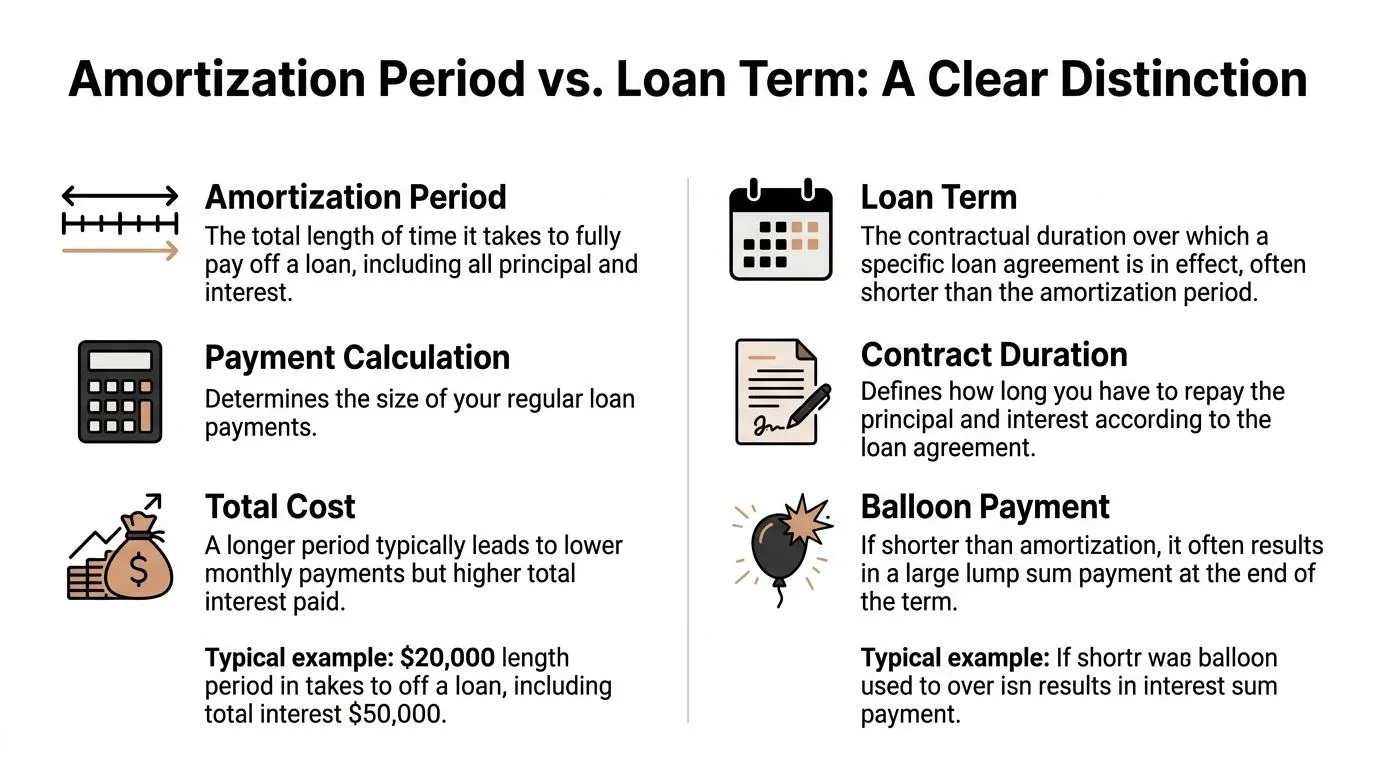

Amortization Period vs Loan Term Explained

This is the confusion point that trips up a lot of borrowers. Amortization period and loan term are related, but they are not the same thing.

A business lender may write a contract with one term and calculate payments using a different amortization period. If you treat those as identical, you can misread the deal.

The clean distinction

The clearest definition comes from BDC: the loan term is the period the lender is committed to specific agreement conditions, while the amortization period is the total time needed to fully repay principal and interest (BDC glossary definition).

Here's the side-by-side version:

| Concept | What it means | Why you care |

|---|---|---|

| Amortization period | Total payoff timeline | Helps determine your regular payment size |

| Loan term | Length of the current contract | Tells you when the agreement ends or must be renewed |

That distinction matters most in commercial lending, where contracts often don't run all the way to full payoff.

Why mismatches create risk

If the term is shorter than the amortization period, the payment may be calculated as if the loan will be repaid over a longer window. That can make the monthly payment easier to manage. But when the contract term ends, you may still owe a remaining balance.

That's where a balloon payment can enter the picture. You've been making scheduled payments, but the debt wasn't built to reach zero by the end of the contract. The leftover amount becomes a problem you must refinance, renew, or pay off.

A busy owner can miss this because the payment looks comfortable. The risk is hidden in the timing, not the amount.

Use this quick check when you review an offer:

- Same end date: If the term and amortization period line up, the loan is designed to be paid off within the contract.

- Different end date: If the amortization runs longer than the term, ask what balance remains when the term ends.

- Contract reset risk: Ask what happens at maturity. Renewal terms, refinance conditions, and cash payoff expectations should all be clear before signing.

If you don't know whether the balance reaches zero at the end of the contract, you don't yet know how the loan ends.

The Difference Between Loan and Accounting Amortization

The word “amortization” shows up in two very different conversations. Your lender uses it to describe how debt gets repaid. Your accountant uses it to describe how certain asset costs are recognized over time.

Those are not interchangeable ideas.

When your lender says amortization

In lending, amortization is about cash leaving the business. It affects your payment amount, your balance reduction, and your financing flexibility.

That's why operational leaders care about it. It changes what lands on your cash flow forecast every month. A longer loan amortization period may ease pressure on working capital, while a shorter one may clean up the balance sheet faster.

When your accountant says amortization

In accounting and tax, the word usually applies to intangible assets. Under IRS rules for Section 197 intangibles, assets such as goodwill, trademarks, and patents are assigned a fixed 15-year amortization period, regardless of their actual economic lifespan, according to Thomson Reuters' explanation of the rule (Section 197 amortization overview).

There's another important nuance. The same source explains that if an intangible asset has a legal life shorter than that standard, the shorter legal life controls. It also notes the straight-line formula often used for amortization: (Book Value – Salvage Value) / Number of Periods, and for intangibles the salvage value is typically $0.

That's very different from loan amortization. Accounting amortization is an expense recognition method. Loan amortization is a repayment structure.

If you manage asset-heavy operations, it helps to look at debt and balance sheet questions together. This guide to managing farm assets and liabilities is a useful example of how financing decisions connect to asset management, especially in businesses where equipment, land use, and borrowing all interact.

For the bookkeeping side, accurate entries matter just as much as the financing terms. A practical reference on how to do journal entries can help keep those records clean when loans and amortized assets are both in play.

Sample Amortization Schedules for Business Loans

Your loan options can look similar at approval and behave very differently once payments start. A $150,000 SBA loan, a $150,000 equipment loan, and a $150,000 short-term loan may all solve the same immediate funding need, but they create very different monthly obligations and very different total borrowing costs.

That is why sample amortization schedules matter. They show how each loan type spreads principal and interest over time, so you can judge the loan by its real effect on cash flow, not just by the approval amount.

Three common business loan patterns

| Loan type | Common use | Typical amortization profile | What that usually means for your business |

|---|---|---|---|

| SBA loan | Expansion, acquisition, large working capital projects | Often stretched over a longer repayment schedule | Lower monthly payments, but interest accrues over a longer period |

| Equipment loan | Vehicles, machinery, production tools | Usually structured to match the useful life of the asset | Payments are often easier to justify because the asset should still be producing value while you repay it |

| Short-term loan | Inventory, payroll gaps, urgent working capital | Compressed repayment schedule | Higher monthly pressure, but less time carrying the debt |

A good way to read this table is to ask one practical question: does the repayment clock match the job the money is doing?

For an equipment purchase, that match often matters most. A machine that supports production for years should not force such a heavy monthly payment that it strains operations before the machine has paid for itself. The loan should fit the earning life of the asset as closely as possible.

Short-term financing works differently. It acts more like a bridge than a long-haul truck. You use it to cover a gap, solve a timing issue, or grab a quick opportunity. Because the payoff window is tighter, the schedule puts more pressure on monthly cash flow.

SBA loans often sit on the other end of the spectrum. They are commonly used for projects that take time to generate returns, such as buying a business, opening a new location, or funding a broader expansion plan. A longer amortization schedule can give you room to grow into the payment.

What a sample schedule helps you see

A sample amortization schedule is useful because it answers questions owners usually do not ask until after closing:

- How much of each payment goes to interest early on?

- How fast does the principal balance fall?

- Does the payment fit my slow months, not just my strong months?

- Will this debt still be on the books when I want to finance the next stage of growth?

If you want to pressure-test those numbers before you commit, this guide on how to calculate the real cost of a small business loan without the headache can help you compare offers beyond the advertised payment.

A practical filter for reviewing loan schedules

| Question | Why it matters |

|---|---|

| What is the money buying? | Long-lived assets usually support longer amortization better than short-lived needs. |

| When will the investment start producing cash? | If revenue shows up later, a tight repayment schedule can create stress early. |

| How predictable is your monthly income? | Businesses with uneven cash flow have less room for aggressive payments. |

| What will this payment limit? | A loan payment that looks manageable on paper can still reduce hiring, inventory purchases, or marketing capacity. |

The strongest schedule is the one that lets the loan do its job without crowding out the rest of the business. That is the true test.

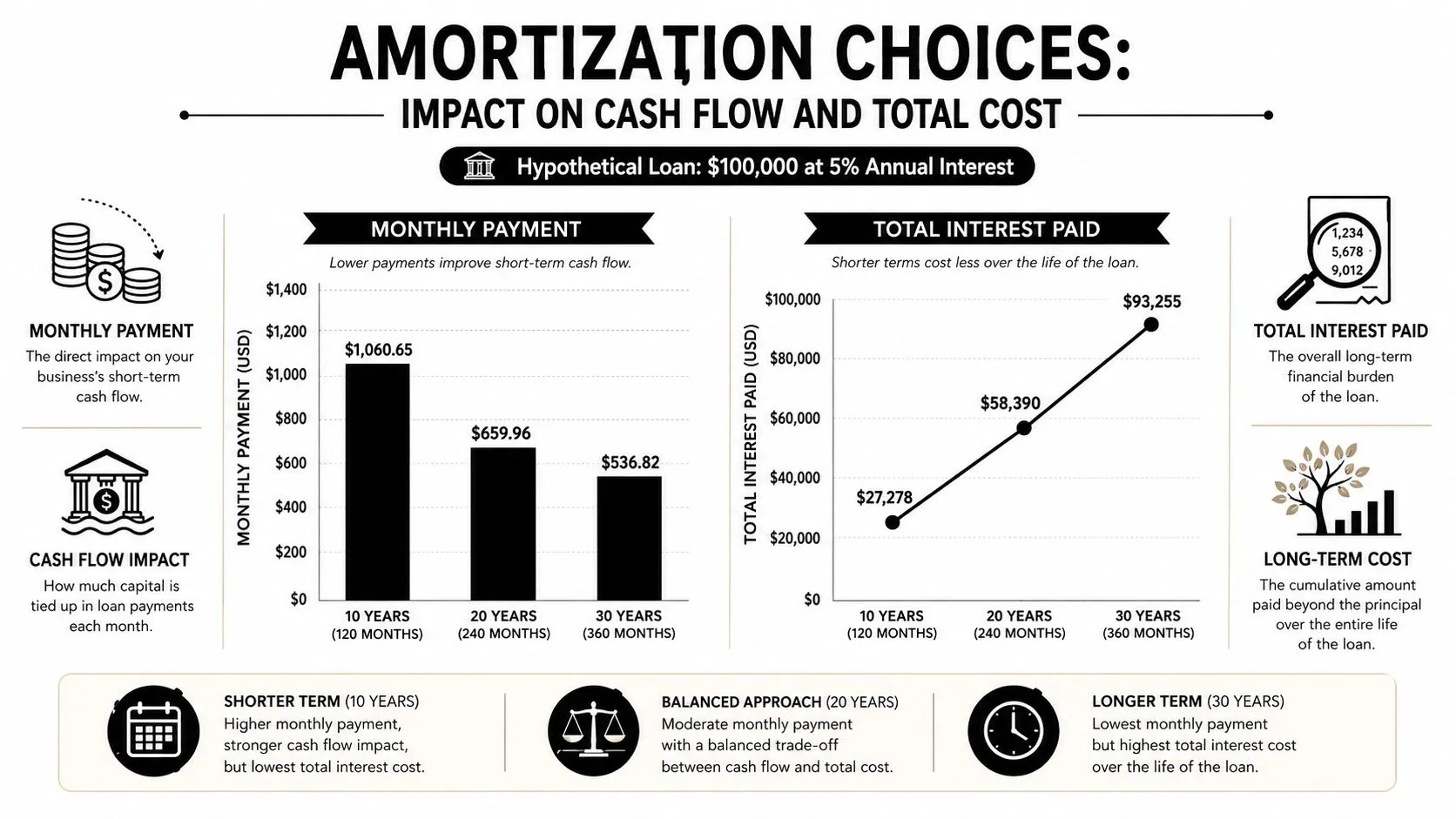

How Amortization Impacts Your Cash Flow and Total Cost

Your loan closes. The money hits your account. Now the critical question emerges. Will this payment schedule help the business grow, or will it crowd out inventory, hiring, marketing, or your cash reserve?

That is why amortization matters.

A longer amortization period usually gives you a lower monthly payment, which can make the loan easier to carry during uneven months. The tradeoff is simple. Because you repay the balance more slowly, more interest builds up over time, and the total cost of the loan rises.

The tradeoff every owner is making

Amortization works like stretching the same expense over a different length of time. Spread it out, and each month feels lighter. Compress it, and each payment gets heavier, but you get rid of the debt faster and usually pay less overall.

For a business owner, that tradeoff is not abstract. It shows up differently depending on the loan type under consideration:

- SBA loans often use longer amortization periods, which can preserve working capital and reduce pressure on monthly cash flow.

- Equipment loans often sit somewhere in the middle, especially when the equipment is expected to produce income over several years.

- Short-term business loans usually push repayment into a much tighter window, which can raise the payment sharply even if the approval process was fast.

The loan with the lowest payment is not automatically the best option. It may be the loan that keeps you in debt longer.

What this means for cash flow

Cash flow problems usually come from timing, not theory. If revenue arrives after payroll, after rent, and after vendors need to be paid, the size of your loan payment matters a great deal.

A longer amortization period can help if your business is opening a new location, building up inventory before a busy season, or waiting for a project to start producing revenue. Lower required payments leave more room for day-to-day operations while the investment has time to work.

A shorter amortization period can make sense when cash flow is steady and margins are healthy. In that case, higher payments may be manageable, and the reward is a lower total borrowing cost.

The practical question is this. Do you want to optimize for monthly flexibility, total cost, or a balance of both?

Why total cost can surprise owners

Many owners compare loan offers by monthly payment first because that number feels immediate. That is understandable. Monthly payments affect this month's budget.

But total cost tells you what the loan will really take from the business over time. A lower payment can be helpful, especially with an SBA loan or a longer equipment financing structure, yet it can also mean you are paying interest for much longer than expected. A short-term loan creates the opposite pressure. You may pay less interest in total if the rate and fees are reasonable, but the larger payment can strain cash flow right when the business still needs room to grow.

That is why strong loan decisions look at both numbers together.

Use this lens:

- Protect cash first if the business still needs liquidity for operations, hiring, or inventory.

- Reduce total interest first if revenue is predictable and the payment will not limit other priorities.

- Match repayment to the asset or goal so the debt does not outlast the benefit it was supposed to fund.

If you want a better way to compare offers beyond the stated rate and monthly payment, review this guide on how to calculate the real cost of a small business loan without the headache.

Owners usually understand why they borrowed. Trouble starts when the repayment schedule takes more cash out of the business, and for longer, than expected.

How to Choose the Right Amortization Period for Your Business

The right answer depends on what the business needs now, what the borrowed funds are supposed to accomplish, and how much payment pressure your operating model can handle. There isn't one perfect amortization period. There is only the one that best fits your timing, margins, and risk tolerance.

Choose longer when flexibility matters most

A longer amortization period can make sense when your first priority is preserving cash. That often applies when you're opening a new location, installing equipment that won't contribute immediately, or stepping into a project with a ramp-up period.

Choose that direction when:

- Revenue timing is uneven: If collections arrive in waves, lower fixed payments are easier to absorb.

- You still need capital after funding: Expansion projects rarely stop at the loan closing.

- The loan supports growth, not rescue: A lower payment gives the project time to work.

This isn't about being conservative. It's about respecting timing. A good business can still feel squeezed if the debt schedule demands results before the investment can reasonably produce them.

Choose shorter when cost control matters more

A shorter amortization period usually fits established businesses with stronger cushions. If revenue is predictable and you don't need maximum payment flexibility, faster payoff can improve long-term economics.

That tends to work well when:

- Margins are stable: You can absorb a higher payment without creating operational strain.

- The business is already scaled: You're not relying on the loan to fund several moving parts at once.

- You want the debt gone quickly: Less time outstanding usually means less interest paid over the life of the loan.

This approach also creates cleaner optionality later. When you reduce debt faster, you may free up borrowing capacity for future opportunities.

Questions to ask before you sign

Before you accept any offer, ask questions that connect the loan to operations:

How much payment room do we really have each month?

Don't answer from optimism. Answer from your actual cash conversion cycle.Does the repayment period match the use of funds?

A long-lived asset and a temporary cash need shouldn't automatically share the same repayment horizon.What happens if growth takes longer than expected?

Stress-test the payment against a slower ramp, not just the best-case plan.Will this structure limit our next move?

A loan that solves today's issue but blocks tomorrow's flexibility may be poorly designed.

If you're weighing repayment options more broadly, this piece on how to choose the right business loan repayment terms without sinking cash flow adds a useful decision lens.

The strongest borrowers don't just negotiate rate. They negotiate fit. That means choosing an amortization period that supports the business you have now and the one you're building next.

If you're comparing loan options and want help matching repayment structure to your cash flow, Business Loan Warrior can help you review funding choices with more clarity. The goal isn't just to get approved. It's to secure financing with terms your business can carry and use for growth.