You've probably got a stack of transactions already. A few customer payments, a supply purchase, maybe a bank loan that just hit the account, and now your bookkeeping software wants a journal entry. That's the moment many owners freeze. They understand the business activity, but the accounting side feels like a separate language.

It isn't. Journal entries are just the written record of what happened financially.

When you learn how to do journal entries, you're not memorizing accounting trivia. You're building the records that turn bank activity into financial statements someone can trust. That matters when you're trying to manage cash, file taxes cleanly, or hand a lender a set of books that doesn't raise questions.

Table of Contents

- Understanding Debits Credits and the Accounting Equation

- A Repeatable Workflow for Creating Journal Entries

- Everyday Journal Entries for Small Businesses

- Recording Loans Payroll and Other Complex Entries

- Common Journal Entry Mistakes and How to Avoid Them

- From Accurate Entries to Business Funding

Understanding Debits Credits and the Accounting Equation

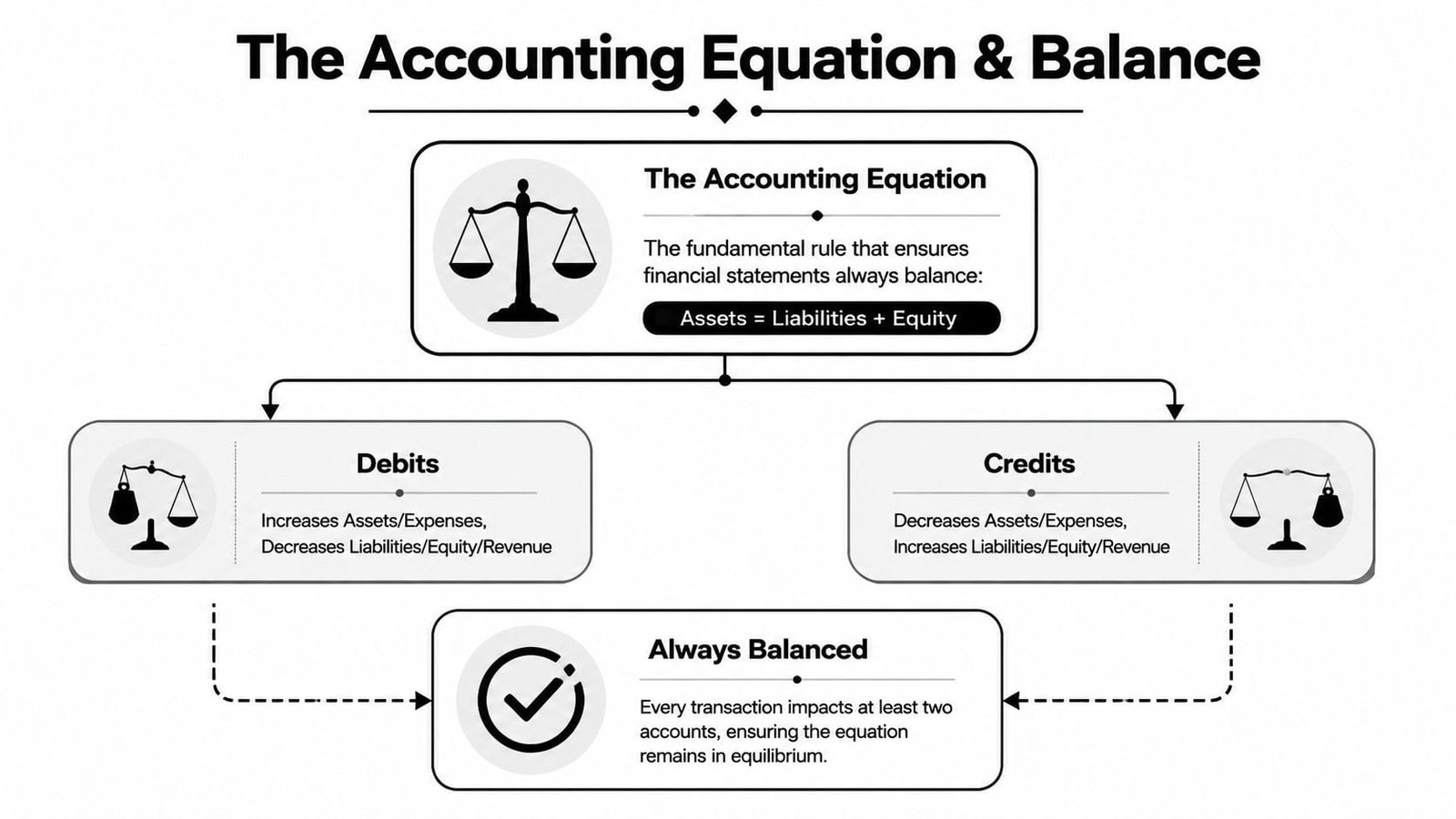

Double-entry bookkeeping is old, but it's still the standard because every entry affects at least two accounts and must keep the accounting equation balanced. Standard journal entry practice also requires the transaction date, affected accounts, debit and credit amounts, and a short description, with total debits equaling total credits before posting to the ledger, as outlined in Clio's journal entry guide.

Why every entry has two sides

Think of your books like a balanced scale. If one side moves, the other side has to move too. Money doesn't just appear in accounting. It comes from somewhere, goes somewhere, or changes form.

If you buy equipment with cash, one asset goes down and another asset goes up. If you take out a loan, cash increases but so does a liability. If an owner takes money out of the business, cash drops and equity changes. That's the whole idea behind the accounting equation:

| Part of the equation | What it means |

|---|---|

| Assets | What the business owns |

| Liabilities | What the business owes |

| Equity | The owner's claim on the business |

The phrase that trips up most owners is debit and credit. In normal conversation, credit sounds good and debit sounds like money leaving. In accounting, those words don't mean good or bad. They describe which side of the entry you're using.

Practical rule: Don't ask whether debit means increase or decrease until you know the account type. The account type decides everything.

The debit and credit cheat sheet

Here's the version I give new clients because it's the easiest one to memorize:

| Account type | Debit | Credit |

|---|---|---|

| Assets | Increase | Decrease |

| Liabilities | Decrease | Increase |

| Equity | Decrease | Increase |

| Revenue | Decrease | Increase |

| Expenses | Increase | Decrease |

That chart is why a cash purchase feels backwards at first. Cash is an asset, so reducing cash is a credit. Supplies may be an expense or asset depending on how you track them, so recording the other side depends on what was bought.

A better way to learn how to do journal entries is to stop thinking in abstract terms and ask two plain-English questions:

- What changed in the business

- Which accounts hold those changes

For example:

- Customer paid cash for a sale means cash increased and revenue increased.

- You paid the electric bill means an expense increased and cash decreased.

- The bank funded your loan means cash increased and loan payable increased.

If the entry doesn't tell a clear business story, it probably isn't ready to post.

Once you understand that each transaction has two financial effects, debits and credits stop feeling mysterious. They become a sorting system.

A Repeatable Workflow for Creating Journal Entries

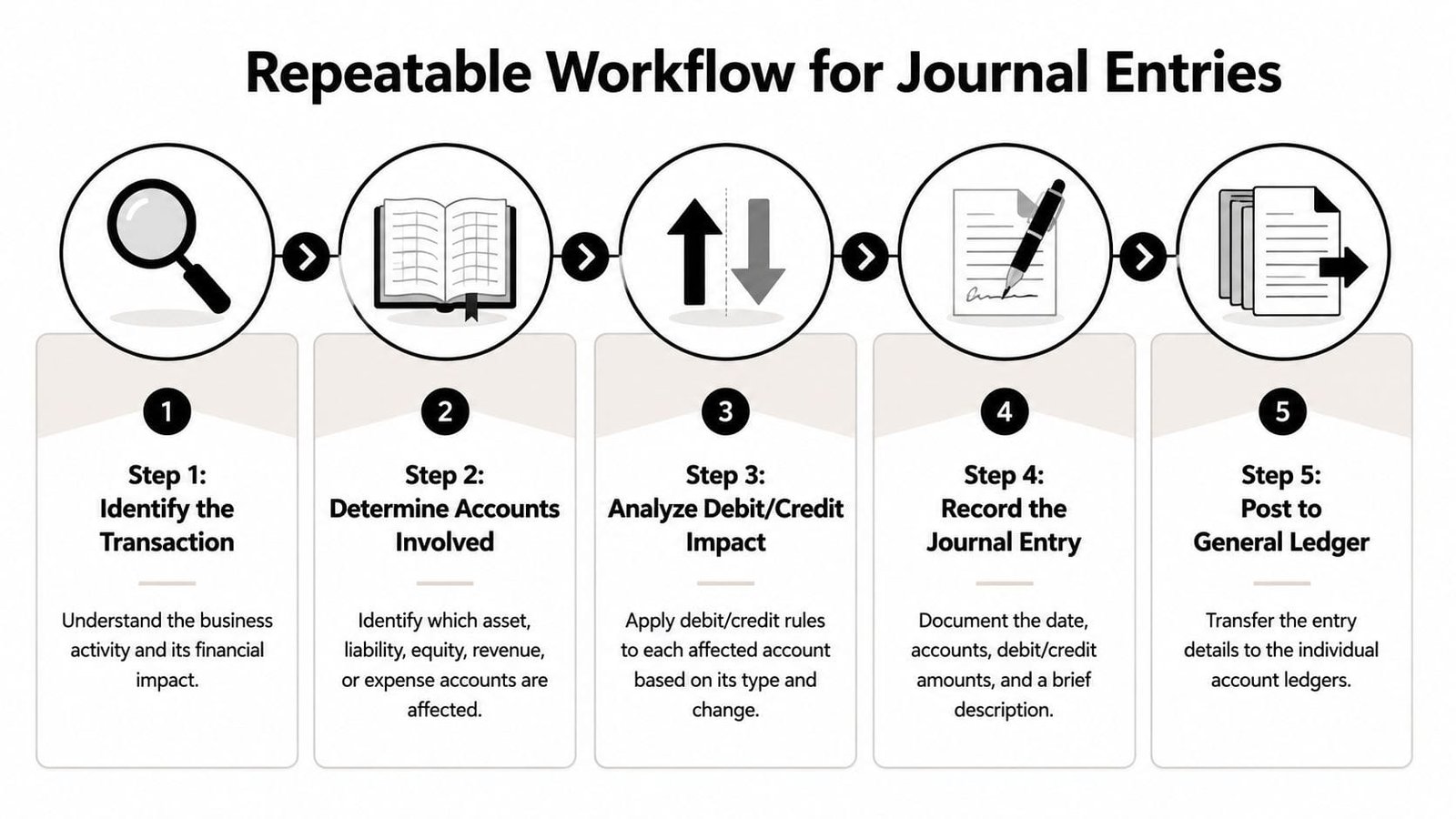

Most bookkeeping errors don't come from hard accounting. They come from rushing. A repeatable workflow fixes that.

For higher-volume businesses, standard practice starts with sorting transactions, assigning a unique reference number and date, identifying the affected accounts, and entering debits and credits that net to zero before approval and posting to the general ledger. Chronological recording and documented reviewer sign-off strengthen that process, as described in Nutrient's journal entry workflow overview.

Start with proof not memory

Never build an entry from memory if a source document exists. Use the invoice, receipt, loan statement, payroll report, bank memo, or bill. That document tells you what happened, when it happened, and often how it should be classified.

A practical workflow looks like this:

- Identify the transaction. Read the document until you can explain the event in one sentence.

- Choose the date. Use the date that fits the accounting event, not just the date you happen to be entering it.

- Pick the accounts. Name every account touched by the transaction.

- Apply the debit and credit rules. Use the account type chart from above.

- Check that the entry balances. If debits and credits don't match, stop there.

Software follows this same logic. For example, Oracle NetSuite's statistical journal process requires users to enter an Entry No., Date, line-item Account and Amount, click Add for each line, and Save to complete the entry. Its documentation also states that the Amount field must be 0 or a positive number so the related statistical account updates correctly, with an Absolute Update option available for one or more statistical accounts at the same time, according to Concentrus on NetSuite statistical journals.

A short walk-through helps:

Build the entry so someone else can follow it

A good journal entry isn't just balanced. It's readable months later.

Include these basics every time:

- Reference number: Something unique you can trace back to support.

- Clear account names: Don't hide transactions in vague buckets.

- Short description: Explain what happened in ordinary language.

- Attached backup: Keep the receipt, statement, or invoice with the entry.

Here's what works in practice. “Loan payment for April per bank statement” is useful. “Bank transaction” is not. Clean descriptions save time when your CPA asks questions, when you're reconciling, and when a lender wants to understand unusual activity.

Everyday Journal Entries for Small Businesses

The fastest way to learn how to do journal entries is to work through common transactions. Once you see the pattern a few times, the logic repeats.

Cash sale

A customer pays at the time of sale. The business receives cash and earns revenue at the same moment.

The thought process is simple. Cash went up, so debit Cash. Revenue went up, so credit Sales Revenue.

Journal entry

| Account | Debit | Credit |

|---|---|---|

| Cash | XXX | |

| Sales Revenue | XXX |

Sale on credit

You send an invoice, but the customer hasn't paid yet. The business still earned revenue, but instead of cash, you now have a receivable.

That means Accounts Receivable increases and Sales Revenue increases.

Journal entry

| Account | Debit | Credit |

|---|---|---|

| Accounts Receivable | XXX | |

| Sales Revenue | XXX |

If you're still getting comfortable with receivables, this guide to accounts receivable management helps connect the entry to actual collection habits.

A credit sale is where many owners first see why accounting isn't the same as bank activity. You can earn revenue before cash arrives.

Buying supplies with cash

You buy office or shop supplies and pay immediately. In many small businesses, those purchases are recorded directly to Supplies Expense. In others, they may go into a supplies asset account first and get adjusted later. The right choice depends on how detailed your bookkeeping needs to be.

For a basic month-to-month system, the entry often looks like this:

| Account | Debit | Credit |

|---|---|---|

| Supplies Expense | XXX | |

| Cash | XXX |

The business story is plain. You gave up cash and got business use from the supplies.

Paying a utility bill

A monthly utility payment usually increases an expense and decreases cash. If the bill relates to the current period and you're paying it now, the entry is straightforward.

Journal entry

| Account | Debit | Credit |

|---|---|---|

| Utilities Expense | XXX | |

| Cash | XXX |

That's not a glamorous entry, but these routine expenses shape your monthly profit. If they're misclassified or dated wrong, your reporting gets noisy fast.

Quick reference for common business transactions

| Transaction Type | Account Debited (Increase) | Account Credited (Decrease/Increase) |

|---|---|---|

| Cash sale | Cash | Sales Revenue |

| Sale on credit | Accounts Receivable | Sales Revenue |

| Buy supplies with cash | Supplies Expense | Cash |

| Pay utility bill | Utilities Expense | Cash |

A useful habit is to narrate each entry before recording it. Say it out loud if you need to. “We earned revenue and got paid now.” “We incurred an expense and paid cash.” “We sold the work, but payment is still outstanding.” If you can state the business event clearly, the accounts usually follow.

Recording Loans Payroll and Other Complex Entries

Many business owners find this aspect challenging. The hard part isn't entering a simple sale. It's recording transactions where one payment affects multiple accounts.

A common gap in beginner guidance is real-world entries like loan payments, especially separating principal from interest. That blind spot matters because financing is common in growing businesses, as noted in Enerpize's guide to journal entries.

Loan proceeds and loan repayments

When loan funds hit your bank account, many owners mistakenly book the full amount as revenue. It isn't revenue. You didn't earn it. You borrowed it.

Recording loan proceeds

| Account | Debit | Credit |

|---|---|---|

| Cash | XXX | |

| Loan Payable | XXX |

That entry says cash increased, but so did what the business owes.

Repayments are more nuanced. A loan payment usually contains at least two parts:

- Principal, which reduces the liability

- Interest, which is the borrowing cost and belongs in expense

That means one cash payment may need a split entry.

Recording a loan payment

| Account | Debit | Credit |

|---|---|---|

| Loan Payable | XXX | |

| Interest Expense | XXX | |

| Cash | XXX |

The split should come from the lender's statement or amortization schedule, not a guess. If you want a broader view of how installment borrowing works in practice, this instalment loan playbook gives useful context.

Field note: If you post the whole payment to interest expense, your liability stays too high. If you post the whole thing to loan payable, your profit looks better than it should. Both errors create trouble later.

Payroll depreciation and owner draws

Payroll has the same pattern. One payroll run can affect wage expense, tax liabilities, benefit liabilities, and cash. Even in a simple setup, don't treat payroll as just “money out of the bank.” The cleaner approach is to use the payroll report and record the expense and withholdings based on that support.

A simplified payroll entry might look like this:

| Account | Debit | Credit |

|---|---|---|

| Wages Expense | XXX | |

| Payroll Tax Expense | XXX | |

| Cash | XXX | |

| Payroll Liabilities | XXX |

Depreciation is different because no cash moves when you record it. You're recognizing that a long-term asset provides value over time rather than all at once.

A basic depreciation entry is:

| Account | Debit | Credit |

|---|---|---|

| Depreciation Expense | XXX | |

| Accumulated Depreciation | XXX |

Owner draws also confuse newer owners, especially in single-owner businesses. If the owner takes money out, that usually isn't a business expense. It's a reduction in owner's equity.

Owner draw entry

| Account | Debit | Credit |

|---|---|---|

| Owner Draw | XXX | |

| Cash | XXX |

The practical lesson across all these entries is the same. Follow the economic reality of the transaction, not just the bank feed label. The bank only shows cash movement. Your books need to show what that cash movement meant.

Common Journal Entry Mistakes and How to Avoid Them

A common first-month problem looks like this. The books balance, the bank account ties out, and the profit still comes out wrong. That usually happens because the entry was posted to the wrong account, dated in the wrong month, or written so vaguely that nobody can tell what happened.

A good review habit catches those errors before they spread into your financial statements. Inkle's journal entry guidance recommends checking each entry back to support, confirming debits equal credits, and adding a clear explanation of what happened. That last step matters more than many owners expect, especially once you start recording loan activity, owner transactions, and corrections after month-end.

The traps that catch smart owners

Balanced entries still fail all the time. A loan payment can be posted entirely to loan payable and still balance. It is still wrong if part of that payment was interest. An owner draw can be buried in expense accounts and still balance. It is still wrong because it distorts profit.

Weak descriptions create a different kind of mess. “Transfer,” “adjustment,” or “misc expense” forces future-you to reopen bank statements, emails, and receipts just to understand what you already entered once. If a lender asks how cash moved, or you need to explain a drop in profit, those vague memos slow everything down. Clear descriptions make the books usable, not just balanced.

Date errors are another expensive mistake. If a vendor bill belongs in June but gets recorded in July, June profit looks better than it was and July looks worse. The same issue shows up with corrections. Once a month is closed, fix prior-period problems through a documented adjusting entry instead of quietly editing old transactions. That keeps your reports consistent and your audit trail intact.

Software can make this worse. Bank feeds are helpful, but the bank date is not always the accounting date.

A review routine that saves cleanup time

Before posting an entry, run through this short check:

- Match the numbers to support. Use the invoice, receipt, statement, loan amortization schedule, or payroll report.

- Ask what really happened. Cash moved, but what was the business event behind it?

- Read the memo line. If an outside bookkeeper or lender could not understand it, rewrite it.

- Confirm the date. Post it to the month you want your financial statements to reflect.

- Watch for multi-line entries. Loan repayments, payroll, and accruals often need more than a simple debit and credit.

One more practical rule. Review unusual entries before month-end close, not six weeks later. The source documents are easier to find, and the reason for the transaction is still fresh.

That discipline pays off in your reports. Clean entries produce cleaner profit numbers, which makes it easier to explain performance and calculate metrics like net income for your financial statements.

From Accurate Entries to Business Funding

A lender asks for your last three months of financials. On the surface, the sales look fine. Then the questions start. Why does the loan balance on the balance sheet not match the statement? Why are owner draws mixed into operating expenses? Why does one month show unusually high profit right before a financing request?

Clean journal entries shape the financial statements lenders read, and the entries that matter most are often the ones basic guides barely touch. A growing business usually has more than sales and bills. It has loan proceeds, repayments split between principal and interest, equipment purchases, payroll liabilities, and money moving between the business and the owner. If those entries are posted clearly, a lender can follow the story. If they are muddy, the numbers lose credibility.

That is why accurate bookkeeping affects funding in a very practical way. Good entries make reconciliations easier. Reconciled accounts produce financial statements a lender can trust. Trust shortens the back-and-forth during underwriting.

I see this most often with debt and owner activity. A loan deposit recorded as income makes revenue look inflated. A full loan payment posted to interest expense understates profit and leaves the liability wrong. An owner draw buried in wages or office expense makes the business look less stable than it is. None of those mistakes are hard to fix. They do create avoidable questions during a credit review.

Profit also needs to hold up under scrutiny. If you want a clearer view of the number lenders focus on, review this guide on calculating net income from your financial statements.

The standard is simple. Record what happened, use the right accounts, and keep enough detail in the memo so an outside reviewer can follow the entry without guessing. That discipline gives your books weight when it is time to ask for money.

If you are preparing for funding and want a lender that understands how operating businesses really work, Business Loan Warrior is worth a look. It helps small businesses explore financing options through a single application, with tools that make the path from review to funding easier to manage.