Your revenue may be up, orders may be steady, and the business may look healthy from the outside. But one bad loan can still choke the operation. I see this most often when an owner took fast money during a tight stretch, then months later realizes the payment is eating margin, limiting hiring, and turning every week into a cash management exercise.

That's where a business loan refinance stops being a finance buzzword and becomes a practical operating decision. You're not just replacing debt. You're trying to buy back breathing room, simplify payments, and make the capital structure fit the business you have now, not the one you had when you were under pressure.

A good refinance can help. A bad one just reshuffles the pain.

Table of Contents

- Is Your Business Loan Holding You Back?

- When Does a Business Loan Refinance Make Sense?

- Your Business Loan Refinance Options

- The Step-by-Step Refinance Process

- How to Compare Refinancing Offers Like a Pro

- Sample Refinance Scenarios and Calculations

- Business Loan Refinance FAQs

Is Your Business Loan Holding You Back?

A business owner takes a short-term loan to cover payroll, inventory, or a rough patch. At the time, it works. Funds hit fast, the immediate problem gets solved, and the company keeps moving.

Six months later, the business has improved. Sales are better. Operations are tighter. But the debt still reflects the old emergency. The payment is too aggressive, the lender sweep is too frequent, or the rate is too expensive for where the business stands today.

That's the refinance conversation.

A business loan refinance means replacing an existing business debt with a new financing structure that better matches current cash flow, collateral, credit quality, and growth plans. Sometimes the goal is a lower rate. Sometimes it's a longer amortization. Sometimes it's getting out of a daily or weekly repayment cycle that's draining working capital.

If your debt service is crowding out inventory purchases, marketing, hiring, or seasonal prep, the loan may be doing more harm than good. In that case, refinancing becomes part of a broader working capital strategy for businesses, not just a hunt for cheaper money.

A healthy business can still carry unhealthy debt.

Owners get into trouble when they treat every refinance offer as a win. It isn't. The best refinance improves flexibility and total cost. The weak one only gives temporary payment relief while locking you into more fees, a longer payoff period, or new restrictions.

When Does a Business Loan Refinance Make Sense?

Refinancing is common, but it isn't the main reason most businesses seek funding. In the Federal Reserve's 2023 Small Business Credit Survey, 24% of businesses seeking financing were doing so to refinance or pay down debt, according to this small business lending trends summary citing Fed survey data. That matters because refinance demand tends to move with the rate environment and with what else the business needs, such as working capital or expansion funding.

The signs that justify a refinance review

A refinance usually deserves a hard look when the current debt no longer fits the operating reality of the business.

- Your payment frequency is hurting cash flow: Daily or weekly debits can squeeze payroll, vendor timing, and inventory buys even when revenue is stable.

- You took emergency debt and now qualify for better terms: Businesses often accept expensive capital during a pinch, then become stronger borrowers later.

- You have multiple debts pulling in different directions: One term loan, one card balance, and one short-term advance can create a messy payment calendar.

- Your current loan has restrictive features: Variable pricing, aggressive covenants, blanket liens, or lender control over receivables can limit normal operations.

- You need maturity extension: Sometimes the goal isn't lower cost right away. It's reducing near-term pressure so the company can execute.

A practical refinance should solve an identifiable problem. If you can't name the problem in one sentence, you probably aren't ready.

Practical rule: Refinance because the structure is wrong, not because a lender says you're prequalified.

When refinancing is the wrong move

Owners often fall into a trap. The new monthly payment looks better, so they assume the refinance is smart. That's not enough.

Don't refinance if the new deal only works because the term stretches so far that the total repayment rises meaningfully. Also don't refinance if the old loan carries a prepayment penalty large enough to wipe out the benefit. Another bad reason is using a refinance to avoid fixing weak pricing, poor collections, bloated overhead, or declining margins. Debt can support a business model. It can't rescue a broken one.

A refinance also may not make sense if you expect to pay off the current debt quickly from incoming receivables, a pending sale, or a seasonal spike. In that case, adding new fees can be counterproductive.

The best timing tends to come when the business is stable enough to qualify for stronger terms, but before the existing debt causes operational damage.

Your Business Loan Refinance Options

Not every refinance product solves the same problem. A lot of owners compare lenders before they've compared structures. That leads to the wrong decision fast.

For established companies with stable earnings, the menu has widened. In the private credit market, direct lenders have moved further down-market, and analysis cited by ABF Journal notes that lower middle market borrowers under $20M EBITDA still pay yields about 50 to 75 basis points higher than upper middle market borrowers. That same analysis points to refinance opportunities for smaller borrowers that can replace expensive debt with lower-cost senior-secured structures as lenders compete for their business, as discussed in this ABF Journal analysis of direct lending moving down-market.

Which product fits which problem

Term loan refinance

This is the standard choice when you want a predictable payment and a fixed payoff path. It works well for replacing short-term online loans, consolidating a few balances, or moving from variable payment pressure to a set monthly obligation.

SBA refinance

An SBA-backed structure can be useful when you need longer repayment terms and a cleaner debt package. This is often where owners look when they want to consolidate older business debt into something more manageable. If you want a deeper look at fit and timing, this guide on SBA loan refinancing for existing small business debt is useful.

Line of credit refinance or balance takeout

This can make sense when the problem is revolving debt that never gets paid down. It's less about one-time debt replacement and more about regaining control over short-term borrowing.

Equipment refinance

If a vehicle, machine, or production asset has value and the note is expensive, equipment refinancing can isolate that debt and match it to the life of the asset. This works best when the equipment is central to revenue and in strong condition.

MCA buyout or refinance

This is the trickiest category. A merchant cash advance can create severe cash flow drag because repayment often hits constantly. Replacing it with a term loan can help, but only if the new lender fully pays off the MCA and the new structure doesn't pile on fees that erase the benefit.

Comparing Business Loan Refinance Options

| Refinance Option | Typical Interest Rate | Best For |

|---|---|---|

| Term loan | Varies by lender, credit profile, collateral, and term | Replacing short-term debt with fixed payments |

| SBA loan | Often lower-cost relative to many nonbank products, subject to eligibility and fees | Long-term debt consolidation and lower monthly burden |

| Line of credit | Varies, and total cost depends on draw usage and fees | Flexible short-term access, not always ideal for full consolidation |

| Equipment refinance | Varies based on asset value and borrower strength | Isolating equipment debt and matching repayment to asset use |

| MCA refinance or buyout | Usually lower-cost than an MCA if structured well, but heavily fee-sensitive | Escaping high-cost daily or weekly repayment pressure |

| Senior-secured or unitranche private credit | Pricing depends on EBITDA stability, leverage, and lender appetite | Established businesses seeking to replace more expensive debt structures |

One mistake I see often is using a line of credit to solve a term debt problem. If the debt needs a clear amortization schedule, revolving credit can keep the balance alive longer than intended.

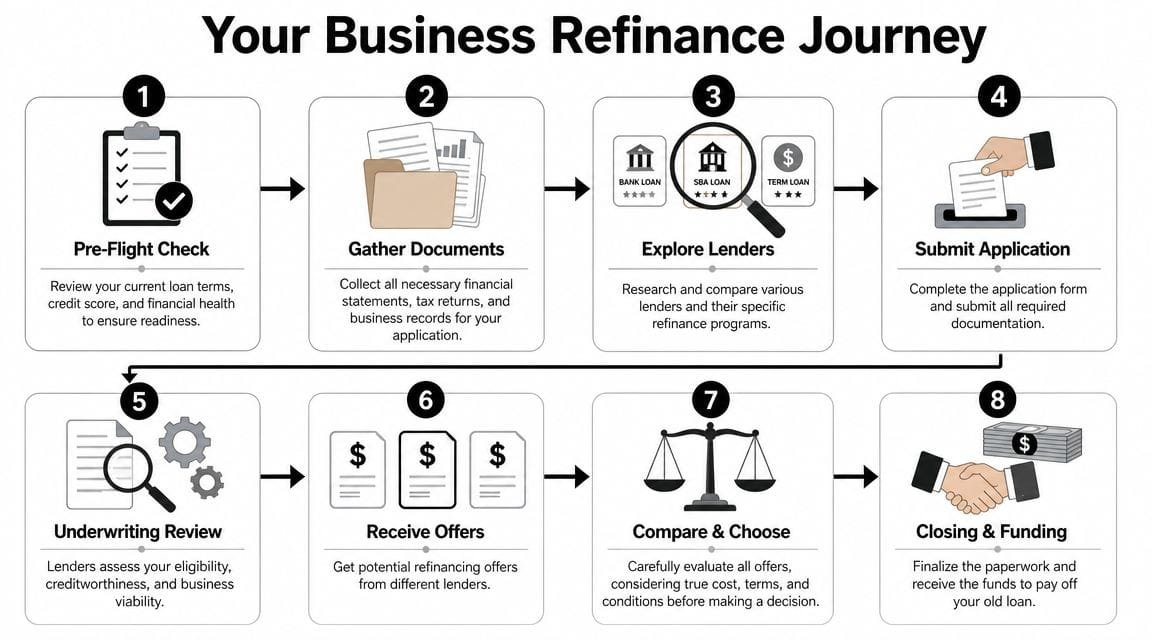

The Step-by-Step Refinance Process

A refinance gets easier when you treat it like a transaction review, not a rescue mission. Owners who rush usually miss fees, payoff mechanics, or documentation issues that slow closing.

Start with the current debt, not the new offer

Before you apply anywhere, gather the documents on the debt you already have. That means promissory notes, payoff letters if available, account statements, and any contract language on prepayment, renewals, liens, or confessions of judgment if relevant.

Then pull together the lender-facing file:

- Current financials: Recent P&L, balance sheet, and business bank statements.

- Tax documents: Business returns and, where required, owner returns.

- Debt schedule: Every existing balance, payment amount, maturity, and collateral tie.

- Ownership records: Formation docs, IDs, and any operating agreement.

- Use-of-proceeds explanation: Even for a refinance, lenders want to know what the new structure accomplishes.

This prep matters because underwriting usually moves faster when the lender can see both the problem and the proposed fix.

What underwriting usually looks for

Lenders generally care about a few practical issues. Can the business support the new payment? Has performance stabilized? Are deposits consistent? Is there enough credit quality or collateral support to justify replacing the old debt?

For a refinance, underwriters also look at behavior on the current obligations. A borrower who has managed expensive debt responsibly can still look strong. A borrower who stacks lenders, misses drafts, or can't explain cash flow swings creates friction immediately.

Clean files close faster. Missing statements, unclear ownership, and outdated debt schedules slow deals more than most owners expect.

Some platforms simplify this stage by using one application to present the file to multiple lender types instead of forcing the owner to restart the process each time. That helps when the business might fit an SBA structure, a conventional term lender, or a specialty lender depending on the debt being replaced.

Closing without surprises

The final stage is where details matter most. Don't assume the lender wires excess funds to you. In many refinance transactions, funds go directly to the payoff lender. Confirm the exact payoff amount, whether it's valid through a specific date, and whether any UCC release or lien termination will follow automatically.

Review these items before signing:

- Rate structure: Fixed, variable, or factor-based economics.

- Fees: Origination, underwriting, legal, servicing, and broker compensation if applicable.

- Prepayment terms: Some loans become attractive only if you hold them long enough.

- Collateral package: Make sure you understand what assets are tied up.

- Repayment frequency: Monthly and weekly are not the same experience in practice.

A smooth close usually comes down to discipline, not luck.

How to Compare Refinancing Offers Like a Pro

Most bad refinance decisions start with one sentence. “The payment is lower.”

That sentence causes a lot of expensive mistakes because a lower payment doesn't automatically mean a lower borrowing cost. The Consumer Financial Protection Bureau notes that refinancing can lower monthly payments while increasing total interest if the payoff period is stretched. That's why a serious comparison has to include effective APR, origination fees, and prepayment penalties, not just the scheduled payment. This point is captured in this discussion of refinancing cost pitfalls and product comparison gaps.

Why monthly payment can mislead you

If one lender offers a shorter term with a higher payment and another offers a much longer term with a lower payment, many owners instinctively prefer the lower payment. That's understandable. Cash flow matters.

But you need to ask four harder questions:

- What is the full amount I will repay if I carry this loan to maturity?

- What fees come out of proceeds at closing?

- What does it cost to exit early?

- Am I fixing the debt, or only delaying the pressure?

That last question matters most with MCA buyouts, revenue-based financing takeouts, and loans marketed mainly on speed. A refinance that gives temporary relief but leaves you paying heavily for longer isn't relief. It's postponement.

If a lender talks only about affordability and avoids total repayment, slow the conversation down.

The side-by-side checklist that matters

When I compare offers, I want them normalized on one sheet. Same columns. Same assumptions. No marketing language.

Use this checklist:

- Net proceeds received: How much goes to your old lender, and how much gets carved out for fees.

- Repayment method: Daily ACH, weekly ACH, monthly ACH, invoice sweep, or standard amortization.

- Total scheduled repayment: What you pay if the loan runs full term.

- Prepayment logic: Simple interest, fixed total payoff, declining payoff, or penalty schedule.

- Collateral and guarantees: Blanket lien, specific asset lien, personal guarantee, or combinations.

- Operational restrictions: Covenants, deposit account requirements, or reporting obligations.

A useful benchmark is to compare each offer against your current debt, not against the lender's sales pitch. If the refinance doesn't improve at least two meaningful points, such as total cost, payment pressure, maturity, lien complexity, or predictability, it may not be worth doing.

For context on how rates fit into that broader view, this breakdown of current business loan interest rate considerations is a good reference point. Rate matters, but rate alone isn't the decision.

A quick visual can also help if you're sorting through offers with different structures.

One more caution. Don't compare an SBA loan, a bank term loan, and an MCA buyout as if they're interchangeable just because they all “refinance debt.” They solve different problems, move at different speeds, and impose different closing standards.

Sample Refinance Scenarios and Calculations

The cleanest way to judge a refinance is to run the math from the borrower's seat.

Scenario one the MCA escape

A business took a $50,000 merchant cash advance with a 1.4 factor rate. That means the contracted payback is $70,000.

Now compare that with a refinance into a 3-year term loan at 15% APR.

The MCA question starts with repayment pressure. Even without getting into a specific remittance schedule, the owner knows the obligation is heavy and front-loaded in real operating life. The term loan changes the structure. Payment becomes predictable, the payoff path is clearer, and the borrower can evaluate the debt with standard amortization logic instead of factor-rate marketing.

What matters here is not pretending every term loan beats every MCA. The primary question is whether the refinance lowers total cost after origination charges, whether the MCA payoff includes any extra fees, and whether the business will keep the new loan long enough for the refinance to make sense.

A successful MCA refinance usually solves two problems at once. It lowers cash flow stress and replaces opaque pricing with transparent amortization.

Scenario two the debt consolidation reset

A company is carrying three obligations:

- $100,000 equipment loan

- $25,000 line of credit balance

- $15,000 business credit card balance

That's $140,000 of combined debt, spread across different payment dates, likely with different pricing logic and different lender rights.

If that borrower refinances into a single SBA 7(a) loan, the immediate gain may be simplification. One note. One payment. One maturity. Better visibility into debt service planning. For many operators, that alone is meaningful because the finance burden isn't just the interest expense. It's the constant administrative drag and the risk of one payment getting mistimed.

The calculation framework should look like this:

- Add up the full payoff amount for all three debts.

- Add any closing and origination costs on the new loan.

- Compare the new scheduled repayment against the combined scheduled repayment of the old debts.

- Test whether the monthly savings come from a better structure, or only from extending the term.

In both scenarios, the right answer comes from total cost of capital, not from the most appealing headline payment.

Business Loan Refinance FAQs

Does refinancing hurt credit

It can affect credit because lenders may review personal credit, business credit, or both during underwriting. The more important question is whether the refinance strengthens the business after closing. If the new structure improves repayment consistency and reduces stress on cash flow, the long-term effect can be positive. What hurts borrowers more often is repeated shopping without a clear target product.

Can you refinance with weak credit

Yes, sometimes. But the options narrow and the trade-offs get sharper. Owners with weaker credit often need to lean more on business performance, deposits, receivables, equipment value, or a clear explanation for past issues. In practice, weak credit doesn't automatically kill a refinance. It usually changes the lender mix and the pricing.

Is refinancing the same as consolidation

Not exactly. Refinancing means replacing existing debt with new debt on different terms. Consolidation means combining multiple debts into one. A single transaction can do both, but they're not identical ideas. You can refinance one loan without consolidating anything, and you can consolidate several balances into one note that still isn't cheaper if the structure is weak.

How soon can you refinance a business loan

It depends on the current lender's payoff rules, any prepayment charges, your recent payment history, and whether the business now qualifies for a better structure. Some loans are worth reviewing early because they were meant as emergency financing, not long-term capital. Others should be left alone until the economics improve. The best time to revisit the debt is when your business profile has strengthened enough to create a real negotiating advantage.

A good business loan refinance doesn't just lower pressure this month. It should make the business easier to run next quarter, next season, and next year.

If you want to review refinance options without bouncing from lender to lender, Business Loan Warrior gives business owners one no-fee application to check pre-approval, compare funding paths, and sort through debt-consolidation or refinance choices with more clarity. It's a practical way to see whether replacing your current loan improves total cost, cash flow, and flexibility before you commit.