You probably already have a number in your head for what your business is worth.

Maybe it's based on years of effort. Maybe it's tied to what a competitor sold for. Maybe it's the sale price you think would make stepping away feel worthwhile. But if a lender, investor, partner, or buyer asked you to support that number today, many owners would pause.

That pause is where business valuation services become useful. Not as a paperwork exercise. Not as something you only do when an attorney or accountant forces the issue. A solid valuation gives you a working map of your business. It shows what drives value, what drags it down, and where the gap sits between what the company is worth now and what you want it to be worth later.

For companies trying to grow, refinance, bring in investors, buy another business, or prepare for an eventual exit, that map matters.

Table of Contents

- Your Business Is Valuable But What Is It Actually Worth

- What Business Valuation Services Really Provide

- The Three Core Business Valuation Methods Explained

- Key Triggers When You Absolutely Need a Formal Valuation

- Your Step by Step Valuation Preparation Checklist

- How to Choose the Right Business Valuation Provider

- Using Your Valuation to Drive Strategic Decisions

Your Business Is Valuable But What Is It Actually Worth

A business owner can know a company has real value and still struggle to prove it.

Take a common situation. You've built a service business with loyal customers, experienced managers, a recognizable local brand, and strong relationships with vendors. Revenue comes in consistently. The team solves problems without you touching every decision. You know that isn't an average company.

Then a bank asks for support behind your expansion request. Or a buyer asks what you're basing your asking price on. Or a partner wants to buy in. Suddenly, “I know what this place is worth” isn't enough.

Value felt versus value documented

Owners usually feel value in places the financial statements don't fully capture at first glance. They see reputation, trust, recurring customer behavior, operational know-how, and a team that keeps the machine moving. Those are real advantages.

But outside parties need those advantages translated into a defensible opinion of value. They want something that can stand up to questions, documentation review, and negotiation. That's where business valuation services help. They convert instinct into analysis.

A valuation doesn't create value. It makes existing value visible.

Why this matters before a transaction

Many owners first think about valuation when a deal is already on the table. That's often late. At that point, the number becomes a source of pressure instead of a planning tool.

A professional valuation gives you a clearer answer to practical questions:

- Can a lender support the financing request? Your value story affects confidence.

- Is your target sale price realistic? A buyer will test every assumption.

- Are you underpricing the business? Owners often miss the worth of systems, goodwill, and management depth.

- Are you overestimating it? Personal attachment can distort expectations.

That clarity helps you negotiate from evidence instead of emotion.

What Business Valuation Services Really Provide

A formal valuation is less like a calculator and more like a full diagnostic exam for your company.

A valuation is a financial physical

When a physician does a physical, they don't guess based on how you look walking into the room. They check history, run tests, review patterns, and look for risks. Business valuation services work much the same way.

A provider reviews your financial records, operating model, contracts, customer concentration, leadership structure, and industry position. For regulatory purposes, defensible valuations require three to five years of audited financial statements, tax returns, management projections, and customer contracts, and incomplete records can limit the valuation methods available, according to Sofer Advisors' guide to business valuation services.

That matters because a good report doesn't just hand you a number. It shows how the appraiser got there, what assumptions they used, and where your business looks strong or exposed.

The standard of value changes the answer

One of the easiest places for owners to get confused is the standard of value.

If you ask, “What is my business worth?” the honest follow-up is, “Worth to whom, and for what purpose?” The answer changes the framework.

Under Fair Market Value, the appraiser looks at what a willing buyer and willing seller would agree to, without special strategic benefits built into the price. Under Investment Value, the analysis considers what the business may be worth to a specific buyer who could gain synergies from the acquisition. That difference can materially change the result. In the Sofer Advisors guide, Investment Value can be 15–25% higher because it includes strategic value for a particular buyer.

Here's the practical takeaway:

- Fair Market Value fits many tax, legal, and general transfer situations.

- Investment Value matters when a specific buyer could combine your company with theirs and realize additional value.

- Purpose drives method. The same company can produce different valuation conclusions depending on the assignment.

Practical rule: Never discuss a valuation number without also discussing the purpose behind it.

That's why a serious valuation feels detailed. It isn't overkill. It's the difference between a rough estimate and an opinion that can hold up with a lender, buyer, or regulator.

The Three Core Business Valuation Methods Explained

If you've ever wondered how an appraiser lands on a number without pulling it out of thin air, the answer is structure.

Professional business valuation services are expected to reconcile three generally accepted approaches: income, market, and asset-based. The IRS requires consideration of all three unless there's a specific reason to exclude one, as noted in the business valuation standard summary.

How appraisers think about value

The simplest way to understand the methods is to compare them to familiar decisions.

The income approach asks, “What are this business's future cash flows worth today?” Think of a rental property. A buyer doesn't only care what the building cost years ago. They care about the income it can produce going forward. In a business valuation, that often means a Discounted Cash Flow analysis, where projected future cash flows get translated into present value based on business-specific risk.

The market approach asks, “What are similar businesses selling for?” This works like pricing a house by looking at neighborhood comparables. Appraisers look at market evidence such as transaction multiples, including EV/EBITDA multiples, then assess how your business compares in quality, scale, risk, and profitability. If you've ever read about commercial real estate valuation methods, the logic will feel familiar because both rely heavily on comparables and context.

The asset-based approach asks, “What is the net value of what the business owns after liabilities?” This is the balance-sheet view. It's often most useful when a company holds significant tangible assets, or when earnings alone don't tell the full story.

Comparison of Business Valuation Methods

| Method | Core Concept | Best For |

|---|---|---|

| Income approach | Values the business based on expected future cash flow converted to present value | Companies with reasonably forecastable earnings and a clear operating model |

| Market approach | Uses pricing evidence from comparable companies or transactions | Businesses in active markets where useful comparison data exists |

| Asset-based approach | Values assets minus liabilities to estimate net worth | Asset-heavy companies or situations where underlying assets matter more than earnings |

A good appraiser doesn't blindly choose one and ignore the others. They weigh each approach based on the facts.

For example, a profitable service firm with strong future earnings may lean heavily on the income and market approaches. A company with specialized equipment, real estate, or large hard assets may require much more attention to the asset-based approach. A distressed business may need an entirely different balance of emphasis.

What confuses many owners is that the methods can produce different answers. That isn't a flaw. It's part of the process. The appraiser's job is to reconcile those answers into a final conclusion that fits the business and the purpose of the assignment.

The final number matters. The logic behind the number matters more.

That logic becomes especially important when you're sitting across from a lender, buyer, or attorney who will ask why the report says what it says.

Key Triggers When You Absolutely Need a Formal Valuation

Some events make a formal valuation hard to avoid. Others should make you want one long before anyone asks.

The obvious trigger points

A formal valuation usually moves from “nice to have” to necessary when ownership, financing, or legal rights are on the table.

Common examples include:

- A pending sale or acquisition: You need a pricing anchor before serious negotiations begin.

- A major financing request: Lenders want a clearer picture of enterprise strength and repayment context.

- A partner buy-in or buyout: A documented value helps keep the discussion grounded.

- Estate, tax, or succession planning: Ownership transfer works better when the numbers are supported.

- A dispute or legal proceeding: Informal estimates rarely survive scrutiny.

When one of those events appears, time pressure usually follows. That's why last-minute valuations often feel stressful. Owners are trying to answer strategic questions while also reacting to deadlines.

Why waiting creates a value gap problem

The more useful question is not “When am I forced to get a valuation?” It's “When does a valuation provide me with an advantage?”

One strong answer is: well before your planned exit.

According to Windes on business valuation services, many owners wait until the final year of an exit plan instead of starting at the beginning of a five-year window, even though an initial valuation can reveal the Value Gap between current value and desired sale price and define the actions needed to close it.

That gap is where strategy lives.

If your target sale number depends on stronger margins, less owner dependence, better contract quality, or reduced customer concentration, you need time to improve those factors. In many cases, those changes can't be rushed in the final stretch.

A valuation done early gives you a practical list of problems to solve:

- Owner dependence: Does too much value sit in your personal relationships?

- Weak documentation: Are contracts, reporting, or processes too informal?

- Customer mix risk: Would a buyer worry about concentration?

- Management depth: Can the business operate smoothly without you every day?

If acquisition is part of your growth plan, financing strategy also enters the picture. A business that understands its current value often makes better decisions around deal structure and capital needs. For owners evaluating expansion by purchase rather than organic growth, this guide to business acquisition loan options can help frame the financing side of that conversation.

The key mindset shift is simple. A valuation isn't just for documenting a deal. It helps shape a better deal years before it happens.

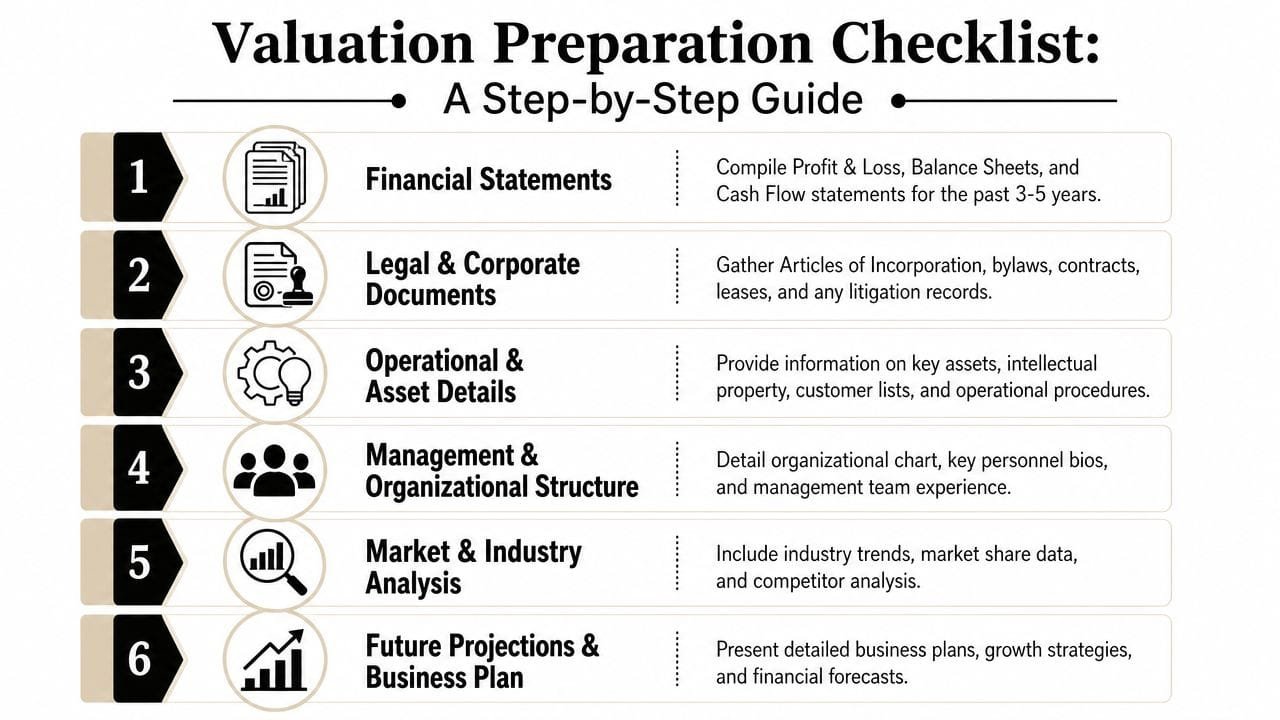

Your Step by Step Valuation Preparation Checklist

A valuation can only be as strong as the records behind it. If your files are scattered, your contracts are half-organized, and your projections live in someone's inbox, the appraiser has less to work with.

That doesn't just slow the process. It can limit how fully your business gets understood.

Get the documents together first

Start with the basics, then go broader.

Historical financials

Pull together profit and loss statements, balance sheets, cash flow statements, and tax returns. Clean, consistent reporting helps the appraiser see patterns instead of chasing explanations.Corporate and legal records

Include formation documents, ownership records, leases, loan agreements, vendor agreements, customer contracts, and any litigation history. If a contract is important to future cash flow, it belongs in the file.Asset details

Build a list of equipment, vehicles, inventory, intellectual property, software, and any other major operating assets. Include anything that gives the business a durable edge.Management information

Show who runs what. Organizational charts, role descriptions, and key employee backgrounds help explain whether the company depends on one owner or has real operational depth.

For owners trying to tighten the financial side before starting this process, it's often useful to review a broader financial health assessment for small businesses so the records tell a cleaner story.

Tell the business story clearly

This is the part many owners underestimate.

A valuation doesn't stop at documents. The appraiser also needs context. Why do customers stay? What makes margins stronger than a competitor's? Which systems reduce risk? Where is growth likely to come from? If goodwill and human capital drive value in your business, someone needs to explain how.

Use this simple prep list:

- Clarify customer relationships: Show how sticky the customer base is and what protects retention.

- Explain leadership depth: Identify managers who carry real responsibility and reduce owner dependence.

- Describe operational discipline: Point to repeatable processes, reporting habits, and decision controls.

- Outline future plans carefully: Projections should be reasoned and supportable, not aspirational wish lists.

Clean paperwork gets the valuation started. Clear business narrative helps the appraiser capture what the paperwork alone misses.

If your valuation ties into ownership transition, gifting, or family transfer issues, legal planning becomes part of the preparation as well. This overview of succession planning and tax guidance is a useful reference for the legal side of a transition.

Preparation does two things at once. It speeds up the assignment, and it reduces the risk that value gets overlooked because the record was incomplete.

How to Choose the Right Business Valuation Provider

Choosing a valuation provider isn't just about finding someone who can produce a report. It's about finding someone who can produce a report that makes sense for your type of business and the reason you need it.

That choice matters in a crowded field. In the United States, the business valuation firms industry includes 3,916 businesses in 2026, with a total market size of about $3.1 billion and a 3.1% CAGR between 2021 and 2026, according to IBISWorld's industry profile for business valuation firms.

Credentials matter but context matters more

Credentials are the first screen, not the last one.

You want a provider with recognized training and a disciplined process. Credentials such as CVA or ASA can signal that the professional follows accepted standards. But a credential alone doesn't tell you whether that person understands your business model.

Industry context often makes a big difference. A restaurant group, specialty retailer, contractor, medical practice, or service firm can all have very different risk patterns and value drivers. The right provider should understand where value sits in your sector, whether that's contracts, recurring revenue behavior, management structure, brand reputation, or hard assets.

A generalist may still be competent. But if they don't understand how buyers or lenders view your type of business, the report may miss important nuance.

Questions worth asking before you hire anyone

Don't ask only about price. Ask how they think.

Here are useful questions:

- What kinds of businesses do you value most often? Look for direct experience with companies like yours.

- What is your process for gathering management input? Good valuators don't rely only on spreadsheets.

- How do you handle goodwill and other intangible value drivers? This matters for service businesses in particular.

- Have your reports been used for lending, tax, or dispute purposes? The provider should understand scrutiny.

- What records do you need from us up front? Their answer will tell you how organized their process is.

Also pay attention to how they explain things. If they hide behind jargon or won't discuss assumptions in plain English, that's a problem. A strong provider should be able to walk an owner through their reasoning without sounding vague or defensive.

The right fit is usually a mix of technical skill, industry familiarity, and communication discipline. You're not hiring a formula. You're hiring judgment.

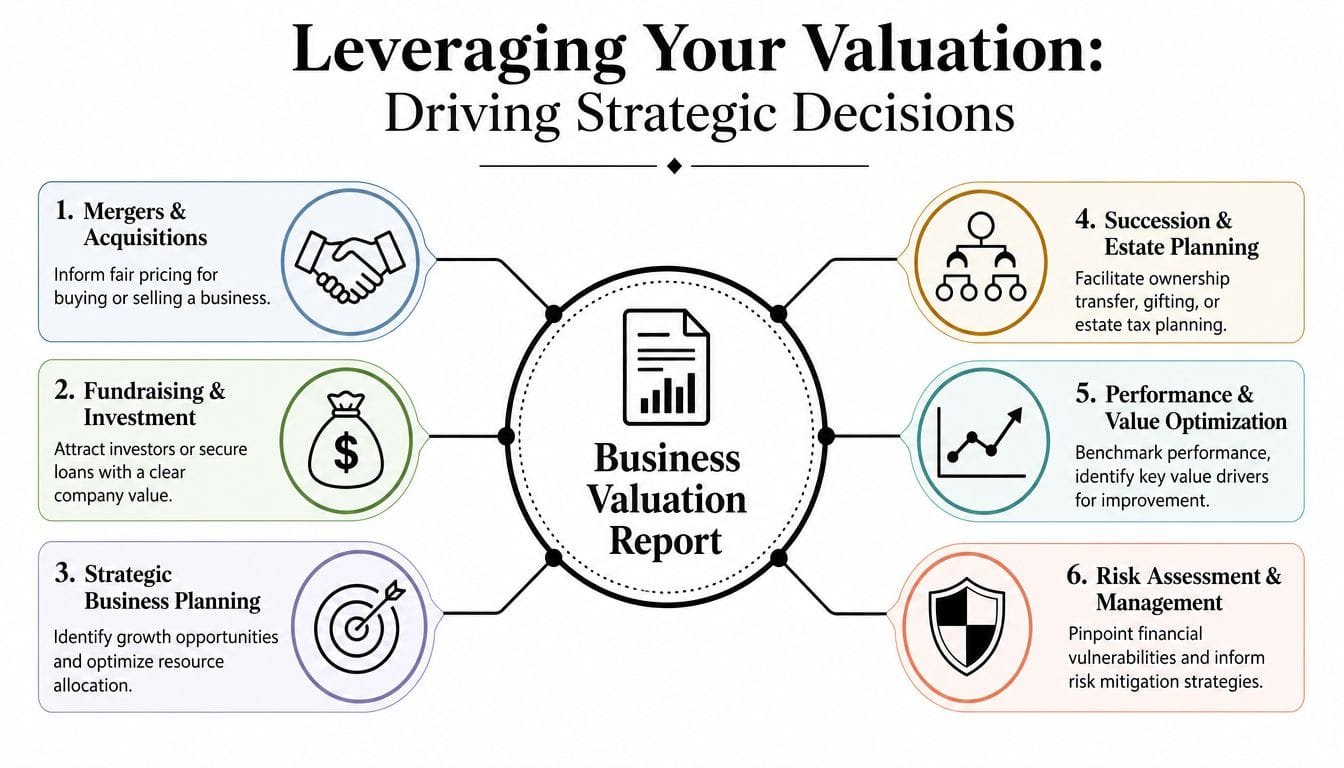

Using Your Valuation to Drive Strategic Decisions

The most important moment in a valuation process comes after the report is delivered.

Too many owners file it away until the next transaction. That wastes most of its value.

Turn the report into action

A valuation should change how you make decisions.

If the report shows customer concentration risk, that's not just a valuation note. It's a growth priority. If it shows that your company relies too heavily on you, that becomes an operations problem to solve. If it highlights the strength of your contract base or management team, you've identified assets worth protecting and strengthening.

A practical way to use the report is to sort findings into six decision areas:

- Financing readiness: Stronger documentation and a clearer value case can help support borrowing discussions.

- Acquisition planning: You gain a firmer base for pricing targets and evaluating your own company as a buyer.

- Exit timing: You can judge whether current value supports your personal goals or needs more work.

- Leadership development: If human capital drives value, management depth becomes an investment, not overhead.

- Risk reduction: Weaknesses in contracts, concentration, or systems become priorities instead of vague concerns.

- Resource allocation: Capital can move toward initiatives most likely to strengthen future value.

This is also where legal and deal structure questions matter. If you're raising capital or negotiating venture-backed terms, it helps to understand the framework investors and counsel often use. For founders and owners navigating those documents, this primer on understanding NVCA documents is a practical legal reference.

A short explainer can help make the strategic uses more concrete:

Why this matters more now

Business valuation services are moving from niche advisory work into something more central to capital decisions. The global business valuation service market is projected to grow from USD 246.5 billion in 2026 to USD 2,021.3 billion by 2035, with a 21% CAGR over that period, according to Business Research Insights on the business valuation service market.

You don't need that projection to know the direction of travel. Owners face more scrutiny around financing, more diligence in transactions, and more pressure to explain why their businesses deserve the price, terms, or capital they're asking for.

That's why the smart use of a valuation isn't passive. You use it to spot the value gap, strengthen goodwill, reduce owner dependence, improve documentation, and present a more credible business to lenders, investors, and buyers.

A good valuation gives you a number. A useful valuation gives you a plan.

That's the key idea. The report is not the finish line. It's a decision tool for building a more financeable, transferable, and valuable company.

If you're preparing to raise capital, refinance, acquire a business, or close the gap between today's value and your long-term goal, Business Loan Warrior can help you explore funding options that fit your next move. You can review customized financing paths without a fee, check pre-approval without affecting credit, and move faster when the time comes to act on what your valuation reveals.