You've got work lined up. The problem isn't demand. It's capacity.

A contractor wins a larger hauling job, or a site development firm adds another subdivision, and suddenly one more truck changes everything. One extra dump truck can keep crews moving, reduce subcontracting, and protect margins. It can also tie up a lot of capital if you buy the wrong unit, structure the financing poorly, or ignore what the lender is really looking for.

That's where most owners lose time. They don't need generic advice about “exploring options.” They need to know which financing structure fits a scaling fleet, what matters if the owner doesn't hold a CDL, and how a newer company can still make a credible file when traditional underwriting is thin. Even details outside the note matter. If you're spec'ing a truck for client-facing work or resale value, practical build choices like choosing chrome bumpers for your rig can influence durability, appearance, and long-term fit for the operation.

Table of Contents

- Why Smart Dump Truck Financing Fuels Growth

- Assess Your Needs and Financial Readiness

- Comparing Dump Truck Financing Products

- Estimate Your Total Cost and Payments

- Application Strategy and Negotiation Tactics

- Your Next Step to Getting Funded

Why Smart Dump Truck Financing Fuels Growth

The owners who use dump truck financing well don't treat it like a necessary evil. They treat it like an operating tool.

If your business is already moving material consistently, financing lets you put a truck to work while preserving cash for fuel, payroll, insurance, and the surprises that always show up on active jobs. That matters more when you're scaling from one unit to several, because fleet growth rarely happens in a straight line. One month you need capacity fast. The next month you need flexibility because another project start gets pushed.

What growth-minded owners get right

Established operators usually focus on three questions first:

- Will this truck stay busy: A financed truck should support contracted work, repeat hauling demand, or a clear internal need that replaces outsourced hauling.

- Does the structure match the plan: A truck you'll keep for years should usually be financed differently from a truck you expect to rotate out.

- What happens if volume changes: Good financing works in a busy quarter and still leaves room to operate if receivables slow down.

A dump truck can be profitable and still strain cash flow if the payment structure doesn't match how the business collects revenue.

That's why smart financing isn't just about approval. It's about matching the truck, the term, and the payment profile to the way your company earns money.

Where this gets missed

A lot of guidance assumes the borrower is the driver. That's outdated. Plenty of strong applicants are owners, partners, or fleet managers who don't hold a CDL themselves. Others are newer businesses with real industry knowledge but thin business credit. Those files can still work when the application shows lender logic, not just ambition.

The difference is simple. Strong borrowers present a truck as a revenue asset with a clear operating plan. Weak borrowers present a wish list.

Assess Your Needs and Financial Readiness

A contractor wins a new site package, needs another truck within two weeks, and starts calling lenders before deciding whether the unit should be a tri-axle, a single-axle, or a lighter non-CDL setup. That is how good businesses end up with bad financing. Approval can come fast. Fixing the wrong truck or the wrong payment structure takes much longer.

Define the work before you price the truck

Start with the revenue job the truck needs to do over the next 12 to 24 months. Established companies scaling a fleet usually make better financing decisions when they tie the truck to a specific lane of work. Aggregate hauling, paving support, demolition, municipal contracts, snow work, or moving material between your own crews all create different underwriting pictures.

The truck has to fit the work, your driver pool, and your compliance burden.

That matters even more for owners adding capacity without adding unnecessary licensing friction. In some operations, a non-CDL dump truck can be the smarter buy because it widens the driver pool and keeps the unit productive across more local jobs. In others, a heavier truck earns more per day and justifies the added cost. The right answer depends on payload, route distance, site access, and who will run the truck.

Review these points before you request terms:

- Primary use case: Match the truck to the material, haul distance, and site conditions.

- Truck class and configuration: Confirm axle setup, body style, GVWR, and whether a non-CDL unit would cover enough of your workload.

- New versus used: New units usually finance more easily. A clean used truck can still be the better financial move if service records, hours, and remaining life hold up.

- Revenue tie-in: Show where the work comes from. Contracted jobs, recurring customers, and internal hauling demand all help.

- Compliance fit: If the unit will move between job sites or cross state lines, review DOT dump truck regulations before you commit to a truck that adds avoidable operating headaches.

I would rather see a borrower finance the right used truck with a clear work plan than a new truck that looks good on paper and sits three days a week.

Build a file an underwriter can approve

Lenders do not just review revenue. They review whether your business can absorb another fixed payment without tightening the rest of the operation. A clean file answers that question quickly.

Established businesses should come prepared with recent tax returns, business bank statements, debt schedules, and basic details on the truck being purchased. If the request is tied to growth, show the path to utilization. A short equipment narrative helps more than owners expect, especially on fleet additions. Explain what the truck will replace, what it will add, who will operate it, and how fast it should become billable.

If you are financing multiple units or adding other iron with the truck, it also helps to understand how lenders view the broader collateral mix. This overview of heavy equipment loan options for construction businesses gives useful context on how equipment age, use case, and business history affect approvals.

Use this checklist before you submit:

- Tax returns: Show earnings consistency and whether the company supports another monthly obligation.

- Bank statements: Show cash discipline. Underwriters look for overdrafts, sharp balance swings, and whether deposits support the story in the application.

- Current debt list: Existing truck, equipment, or MCA payments affect how much room is left.

- Equipment quote or buyer's order: Lenders need a clear purchase price, seller information, and truck specs.

- Insurance plan: If coverage will be tight or delayed, funding often stalls.

- Equipment narrative: State why this truck is needed now, not just why it would be nice to have.

A stronger down payment can help, but cash is not the only way to improve a file. Better bank activity, a shorter term request, or a cleaner explanation of the truck's revenue role can also improve lender confidence.

Established business or startup, prove the same thing

Every lender is trying to answer one question. Will this truck stay working and will the payment get made on time?

For established companies, the proof usually comes from operating history. Show stable deposits, a realistic debt load, and a truck request that fits your current mix of work. If you are scaling from one or two trucks into a larger fleet, explain how dispatch, maintenance, and driver coverage will keep utilization up. That matters for non-CDL owners too. Ownership and driving are often separate in growing companies, and that is not a problem if the file clearly shows who runs the truck and how the business controls the asset.

For startups or credit-thin businesses, the path is different but still workable. The file has to replace missing credit depth with other credibility signals. Good trade references, verifiable time in the industry, a seller quote from a reputable dealer, cash reserves, and a clear operating plan all help. If the owner has managed crews, hauled as a subcontractor, or worked inside the same niche before starting the company, say so directly. A thin file gets stronger when it reads like an operating business instead of a hopeful idea.

Check readiness before you apply

Ask these questions before you let a lender pull credit:

- Can this truck stay active enough to cover its payment and operating costs?

- Do you know who will drive it, insure it, dispatch it, and maintain it?

- Are your recent bank statements clean enough to support the story you are telling?

- If you are a startup, can you show trade references, industry experience, and some liquidity?

- If you are scaling, does this addition improve capacity without straining payroll and receivables?

If the answer to two or three of those is still fuzzy, tighten the file first. Borrowers who do that usually get better options and waste less time with lenders that were never a fit.

Comparing Dump Truck Financing Products

A dump truck can earn well and still be financed the wrong way. I see that problem more often with established companies adding units quickly, especially when the owner is focused on capacity and the lender is focused on a monthly payment.

The right structure depends on what this truck needs to do for the business. A revenue-producing core unit that you plan to run hard for years should usually be financed differently than a truck you may rotate out after a few seasons, a temporary contract truck, or a unit being added by a non-CDL owner who is hiring drivers and building dispatch capacity around it.

The four structures owners actually compare

Equipment loan

This is usually the default for a business buying a truck it expects to keep. You make fixed payments, build equity over time, and own the unit after payoff. For scaling fleets, that can work well when the truck fills a stable role and you want the asset on the books.

The trade-off is simple. Ownership gives you long-term control, but it also means you carry repair risk, resale risk, and the consequences of holding the truck too long.

Capital lease

A capital lease, including a $1 buyout or similar structure, is often chosen when the business wants end-of-term ownership but prefers lease-style paperwork or a payment structure that fits better with its tax and accounting treatment. In practice, this often behaves a lot like a financed purchase.

This can be a good fit if your controller or CPA wants a certain treatment, or if a lender is more flexible on a lease than on a straight loan.

Operating lease

An operating lease fits a different goal. You are paying for use more than ownership. That matters for fleet operators who replace units on a schedule, want to avoid aging iron, or do not want to spend time managing resale.

For a contractor scaling from three trucks to eight, this can protect flexibility. For a startup trying to build long-term equity, it is usually less attractive unless preserving cash matters more than owning the truck.

Business line of credit

A line of credit is a support tool, not usually the best primary tool for the truck itself. It can help cover a down payment, wet kit, body work, initial repairs, insurance gaps, or short receivables cycles tied to new contracts. It is less suited to carrying the full truck cost over time.

If you want a broader look at adjacent structures, this overview of heavy equipment loans is useful context.

Dump Truck Financing Options at a Glance

Industry lenders such as Bankers Financial note that dump truck financing commonly includes loans and lease structures with terms that vary based on truck age, credit strength, time in business, and intended use, with both new and used units often eligible through equipment-focused programs. Their dump truck financing overview is a better reference point than headline rate ranges pulled from one lender's marketing page, because actual approvals move with the file quality and the equipment.

| Financing Type | Best For | Typical Terms | Ownership |

|---|---|---|---|

| Equipment loan | Long-term use, equity building, core fleet assets | Fixed term, commonly several years, with structure driven by truck age, credit, and cash down | Borrower typically owns the truck after payoff |

| Capital lease | Businesses that want lease-style structure but expect to keep the truck | Fixed term with end-of-term buyout features | Usually designed toward end-of-term ownership |

| Operating lease | Fleets that want flexibility, lower long-term asset exposure, or easier refresh cycles | Term set around expected use and replacement timing | Lessor retains ownership unless there's a purchase option |

| Business line of credit | Deposits, working capital support, repairs, timing gaps around acquisition | Revolving access rather than a fixed equipment term | No truck ownership feature by itself |

Which product fits the way you grow

For an established business adding trucks, I usually start with one question. Is this unit being added to build permanent capacity, or to cover a period of growth you may want to adjust later?

If the truck is tied to repeat work, a dependable driver plan, and a niche you already know well, an equipment loan or capital lease usually makes more sense. If you are testing a new lane, expanding into a different material type, or trying to avoid getting stuck with older units at the wrong point in the cycle, an operating lease deserves a harder look.

For non-CDL owners, the same product rules apply. The lender still needs confidence that the business controls the truck, the insurance, the driver, and the revenue stream. The owner does not need to be the one behind the wheel for the file to make sense.

For credit-thin startups, the product decision matters too. A line of credit may sound flexible, but many new businesses are better served by a clean equipment request tied to one truck, one seller quote, and a file supported by trade references, cash reserves, and verifiable industry experience. A thin file gets easier to underwrite when the request is specific.

Use this quick filter:

- Choose an equipment loan if the truck is a long-term revenue unit and you want ownership after payoff.

- Choose a capital lease if you expect to keep the truck but a lease structure works better for payment design or accounting treatment.

- Choose an operating lease if replacement timing, fleet flexibility, or limiting long-term equipment exposure matters more than building equity.

- Use a line of credit selectively for related cash needs around the purchase, not as the first answer for the entire acquisition.

Before you sign, compare the financing structure against the truck's real operating burden, not just the note. The 2026 owner operator financial guide is a good reminder of how quickly insurance, maintenance, fuel, and downtime change what looks affordable on paper.

Estimate Your Total Cost and Payments

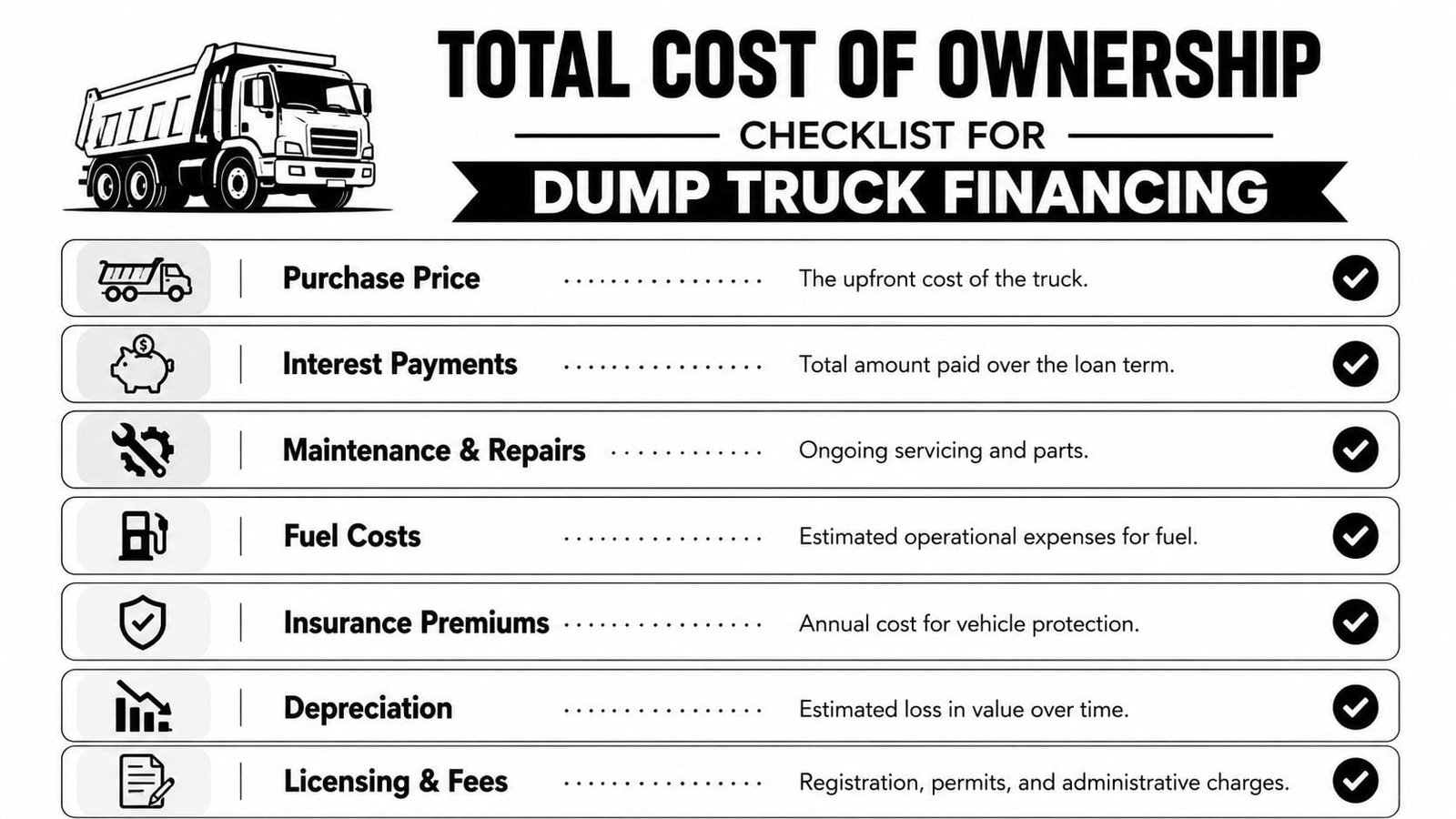

A lender quote is only one part of the decision. The actual number is the truck's full monthly burden on the business.

Build your true monthly number

Use a simple operating formula:

Monthly payment + insurance + fuel + maintenance + operator pay = true monthly cost

That's the number your jobs have to carry. If you stop at the finance payment, you can convince yourself a truck is affordable when it really isn't.

I also like adding a second line item for the non-monthly costs owners forget:

- Licensing and fees

- Unexpected repairs

- Downtime impact

- Depreciation and eventual replacement planning

A good owner-operator budgeting reference is this 2026 owner operator financial guide, because it forces you to think beyond the note and into real operating expense categories.

Know your true monthly truck cost before you negotiate the financing. If the truck can't support itself on a realistic operating budget, a better rate won't fix the problem.

A practical payment stress test

Take a hypothetical $150,000 truck. Don't jump straight to whether the lender says yes. Build the truck into the rest of the business.

Ask:

- What is the monthly payment range under the term you're considering

- What will insurance add

- How much fuel will this route profile burn

- What maintenance reserve should you hold

- Who is driving it, and what does that labor cost really look like

Then pressure-test the result. If collections slow for a month, can the business still carry the truck? If a major repair hits early, does the company have room to absorb it?

That's why I prefer looking at total cost of ownership before comparing lender offers. If you want a clean framework for that math, this guide on how to calculate the real cost of a small business loan without the headache helps translate the finance structure into an actual operating decision.

A truck should earn its place in the fleet. If the margin only works under best-case assumptions, the deal is too tight.

Application Strategy and Negotiation Tactics

A lender usually decides fast whether your file looks financeable. They slow down when the story is incomplete, the truck choice does not match the work, or the business owner cannot explain repayment in plain language.

A clean file gets attention. A messy one gets priced defensively.

The established business path

If you already run profitable jobs, have time in business, and are adding a truck because demand supports it, use that position. Underwriters want to see that this unit fits an operating system you already control. That matters just as much as credit score.

For an established company, the best negotiating points are usually the ones that protect cash:

- Ask for options on down payment. Putting more down can lower cost, but keeping cash for payroll, fuel, and repairs may be the better move.

- Negotiate rate and term together. A lower monthly payment can still be an expensive deal if the term is stretched too far.

- Show existing revenue support. Signed contracts, repeat customers, municipal work, and backlog all strengthen the file.

- Answer follow-up requests fast. Delays make lenders wonder what else is missing.

Established fleets should also push on structure, not just approval. If you are buying a second, fifth, or tenth truck, the question is whether this note leaves enough room for the next one. I have seen good companies accept a weak first offer because they were busy. Six months later, they needed another unit and did not like how tight their cash position looked on paper.

Non-CDL owners scaling a fleet should be ready for one extra question. Who is operating the truck, and how is that managed? A lender does not need you to hold the CDL personally if the business has qualified drivers, dispatch control, insurance lined up, and a clear plan for utilization.

The startup and thin-credit path

Newer businesses can still get funded. They just need to prove reliability with more than a personal credit file.

Lenders that work in commercial truck finance often look for alternative signs that the business is real and disciplined. That can include trade references, vendor relationships, deposit history, prior industry experience, and evidence that the owner understands the work. Equifax's business credit guidance explains how supplier and vendor payment history can help establish business credit, which is exactly why trade accounts matter for credit-thin operators (Equifax on building business credit with vendor tradelines).

That gives startups a practical path:

- Bring trade references. Tire vendors, parts suppliers, repair shops, and fuel providers can help confirm payment behavior.

- Document industry experience. Time spent as a driver, dispatcher, fleet manager, or subcontractor helps reduce execution risk.

- Show business deposits and contracts. A lender wants evidence that revenue is not hypothetical.

- Be realistic about down payment. More cash down can offset a thin file, but do not drain the business dry to force a deal.

- Use a guarantor or extra collateral carefully. It can improve approval odds, but it also increases personal exposure if the truck underperforms.

For startups, presentation matters more than polish. A lender will forgive a thin file faster than they will forgive a vague one.

Here's a deeper resource on preparing the submission package itself: the ultimate guide to business loan applications.

A short explainer on lender expectations can help before you submit anything:

Questions to ask before signing

A lot of bad dump truck loans get accepted because the owner was focused on speed. The approval felt like the hard part. It was not.

Before you sign, get direct answers to these points:

- Is the payment fixed for the full term

- Does the deal include a balloon payment

- What is the full amount paid by maturity

- Is there a prepayment penalty

- Are there seasonal or step-payment options

- Under a lease, are there condition, usage, or mileage limits

- How much cash is due at closing, including fees, first payment, and documentation charges

The Consumer Financial Protection Bureau's guidance on auto and equipment-style financing warns borrowers to review total cost, fees, add-ons, and end-of-term obligations carefully before signing (CFPB guidance on reviewing financing terms and costs). The same discipline applies here. If the lender cannot explain payoff, fees, and end-of-term terms clearly, keep shopping.

The strongest negotiation tactic is simple. Submit a file that answers the underwriter's real concerns before they ask, then compare offers on total structure, cash required, and flexibility under pressure. That is how established businesses scale cleanly, and it is how credit-thin startups get taken seriously.

Your Next Step to Getting Funded

By the time you're ready to apply, the hard part should already be done.

You should know which truck fits the work, how much cash you want to keep in the business, which financing structure matches your ownership plan, and what the truck really costs each month after insurance, fuel, maintenance, and labor. That preparation changes the conversation. Instead of asking a lender, “Can I get approved,” you're asking, “Which offer best fits the way this business runs.”

The owners who get the best dump truck financing usually do three things well. They submit complete files, they understand their real operating numbers, and they don't let urgency push them into the wrong structure.

If you're an established company scaling from one truck to several, that discipline protects cash and gives you room to grow. If you're a startup with thin credit, it helps you present a fundable story through trade references, operating experience, and a realistic plan. If you're a non-CDL owner building a fleet, it keeps the focus where it belongs, on business strength, operational control, and revenue.

The truck matters. The financing structure matters just as much.

Business owners who want a faster way to compare funding options can use Business Loan Warrior to check pre-approved offers through a single no-fee application without impacting credit. It's a practical way to save time, review multiple lender paths, and choose a dump truck financing offer that fits your fleet strategy instead of forcing your business to fit the financing.