You finally get the email you've been chasing. A serious buyer sends a purchase order that's big enough to change your year. Then the math hits. Your supplier wants money now, your customer will pay later, and your cash account can't carry both growth and fulfillment at the same time.

That's a key reason owners start looking into financing purchase orders. Not because the business is weak, but because growth creates a cash gap at exactly the wrong moment. If you've got a confirmed order, a capable supplier, and a customer that pays on standard terms, purchase order financing can keep the deal alive. Used well, it enables growth. Used badly, it turns one good sale into a long stretch of expensive capital.

Table of Contents

- The Growth Dilemma You Did Not See Coming

- How Purchase Order Financing Actually Works

- Decoding the Costs and Underwriting Process

- Is PO Financing Right for Your Business

- The Benefits Dangers and Critical Exit Strategy

- PO Financing vs Other Funding Alternatives

- Your Application Checklist and Choosing a Partner

The Growth Dilemma You Did Not See Coming

A big order should feel like a win. For a lot of small and midsize businesses, it feels like a funding emergency.

The problem usually isn't profitability. It's timing. You need cash to buy or produce goods before your customer pays the invoice. That gap sits right in the middle of your working capital definition, and it's where otherwise healthy businesses get stuck. They aren't short on demand. They're short on upfront liquidity.

Traditional loans often miss this situation. A bank may take too long, ask for broader collateral, or evaluate the request like general business debt instead of an order-specific transaction. But the need is narrow and immediate. You don't need a long-term loan for overhead. You need a way to pay a supplier so the order ships.

That's why purchase order financing has moved from a niche tool into a more mainstream funding method. The global purchase order financing market was valued at approximately $71.7 billion in 2020 and is projected to reach $106.2 billion by 2027 according to Credlix's market overview of import purchase order financing.

Practical rule: If the order is solid but cash timing is the problem, look for a transaction-specific solution before you take on broad, expensive debt.

This matters most for importers, distributors, wholesalers, and product companies selling to larger retailers or institutional buyers. They often have real purchase orders in hand and very little room to prepay suppliers out of pocket. Financing purchase orders exists to bridge that exact gap. The mistake is assuming the bridge takes care of itself after the order is delivered. It doesn't.

How Purchase Order Financing Actually Works

Single-purpose capital for one order

Purchase order financing is best understood as transaction-specific capital tied to one customer order. The funds are used to pay a supplier so goods can be produced, purchased, and shipped. They are not meant for payroll, rent, ad spend, or other general operating expenses.

That distinction matters more than many owners expect. If a business starts using PO financing to patch broader cash flow problems, the facility gets expensive fast and becomes hard to exit. The right use case is narrow. A real purchase order exists, the customer is expected to pay, and the only gap is getting the supplier covered before delivery.

Four parties usually sit inside the deal:

- Your business: You receive the purchase order and manage production, shipping, and communication.

- Your customer: Usually a creditworthy business or government buyer that pays after delivery.

- Your supplier: The manufacturer or vendor fulfilling the order.

- The financing company: The party that pays the supplier and is repaid when the customer pays.

Speed is one reason owners use this product under deadline. Pre-approval decisions are often available within 24 to 48 hours, according to Finder's guide to purchase order financing.

Clean records help. If you track inventory in QuickBooks Online, lenders will often want clear support for item counts, costs, purchase history, and fulfillment details. A tool like Cloudvara for QBO inventory management can help organize that file package before underwriting starts.

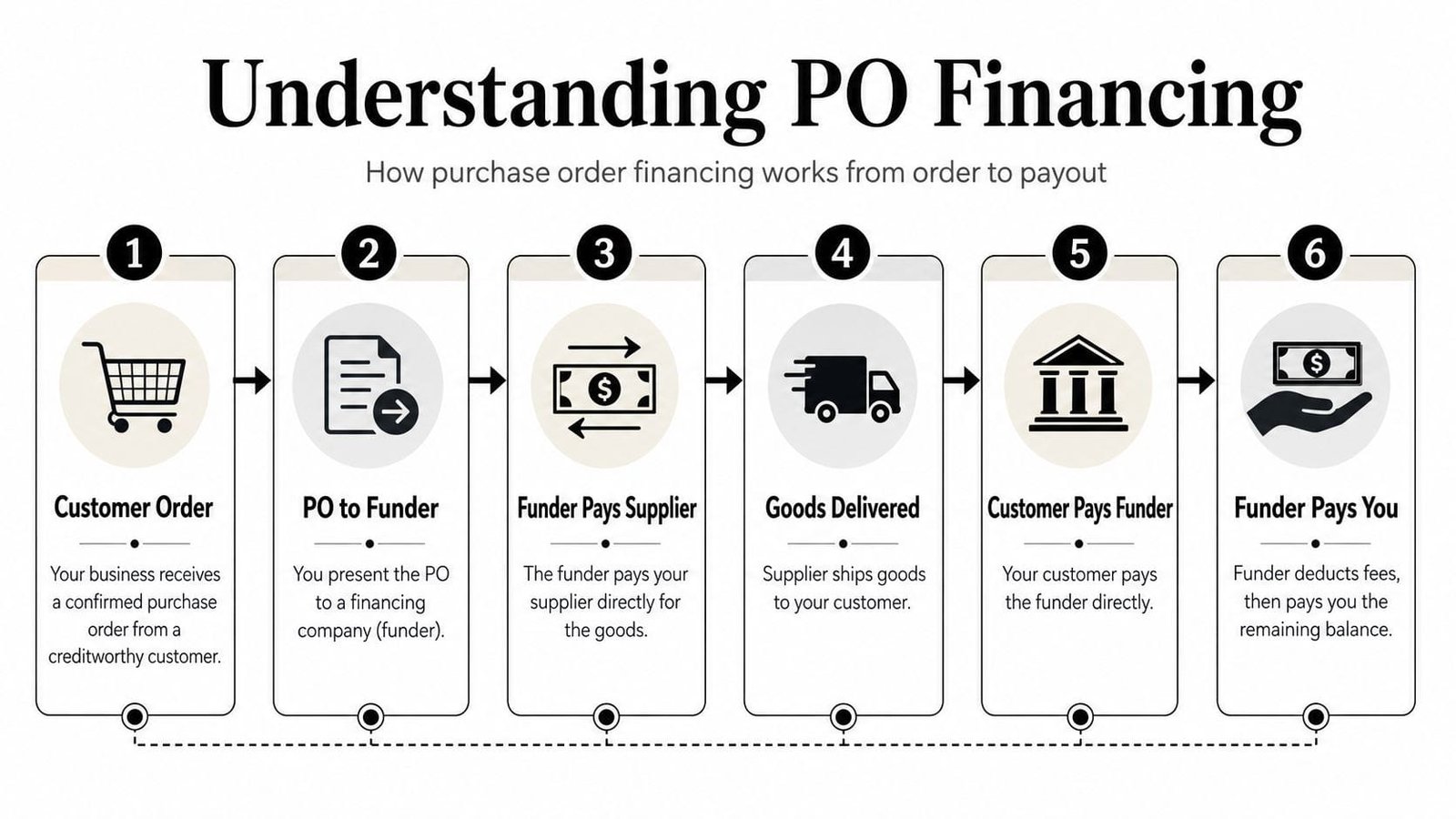

The six step flow

The mechanics are simple. The control points are where owners get surprised.

You receive a confirmed purchase order

The customer submits an order for finished goods. Buyer quality carries a lot of weight because repayment depends on that buyer paying as agreed.You submit the order to the financing company

The funder reviews the purchase order, supplier information, production timeline, and the margin in the transaction.The funder pays the supplier directly

In many structures, funds do not pass through your operating account. The financing company pays the supplier so manufacturing or procurement can begin.The supplier ships the goods

The shipment goes to your customer or to an approved location under the transaction terms.The customer pays against the order or invoice

Those proceeds are used to repay the financing company. This is why documentation, delivery acceptance, and invoice accuracy matter so much.You receive the remaining balance after fees

Once the funder is repaid and fees are deducted, the rest comes back to your business.

Many owners describe this like a standard loan. In practice, it behaves more like an advance against the cash flow from one order.

That structure explains two common approval issues. First, lenders care heavily about the end buyer's credit quality because that buyer is the repayment source. Second, PO financing usually works best for finished or near-finished tangible goods sold to businesses or government entities, not services or direct-to-consumer sales, as described in the Finder guide linked above.

One more watch-out belongs here, because it affects whether this tool helps or hurts. A successful funded order is only half the job. The other half is deciding what happens after it closes. If the same customer keeps placing orders and every one of them needs outside funding, the business may be growing without building usable working capital. That is where margins start getting squeezed and PO financing turns from a short-term tool into a habit.

Decoding the Costs and Underwriting Process

What the pricing looks like

Owners tend to ask one question first. What will this order cost me by the time everyone gets paid?

Purchase order financing is priced around a transaction, not a long-term amortizing loan. That distinction matters because the fee may look manageable at first glance, then eat far more margin than expected once production delays, freight issues, or slow customer payment stretch the timeline. Analysts at Dealstruck in its guide to purchase order financing note that many funders want gross margins in the 20% to 30% range before they get comfortable, and funding levels can vary based on buyer strength, shipping terms, and deal structure.

The practical question is not whether a funder will cover the supplier cost. The practical question is whether the order still works after fees, inspection costs, wire charges, freight surprises, and the time value of waiting to get your profit back.

I tell owners to model the deal twice. First, run it as planned. Then run it again with a slower delivery, a longer payment cycle, and one margin hit. If the order only works in the best-case version, it is too fragile to finance.

That matters even more if you expect repeat orders. A thin but fundable transaction can train a business to rely on outside capital every time inventory has to be built. If that pattern continues, it often points to a deeper working capital problem, not a one-off growth squeeze. At that stage, broader working capital financing options for businesses may be a better long-term fit than repeating expensive PO transactions.

If the order looks healthy before financing but weak after all fees and delays are accounted for, the order is buying revenue at the expense of profit.

What lenders really underwrite

PO finance firms focus less on your company history than many owners expect. They are asking whether this specific order will convert into cash cleanly and on time.

The review tends to center on three points:

- The buyer can and will pay

- The supplier can deliver as promised

- The margin leaves room for financing costs and mistakes

That first point drives more approvals than owners realize. A strong end buyer with a clear payment record can offset weaknesses that would kill a conventional loan request. A weak buyer does the opposite. If repayment depends on a customer known for deductions, disputes, or slow approvals, the funder sees collection risk, not just credit risk.

Supplier risk gets less attention from applicants and more attention from funders. If the goods are custom, if production is overseas, or if delivery terms are sloppy, the transaction gets harder fast. Incoterms, inspection rights, split shipments, and who holds title at each stage all affect whether the deal is financeable. Small documentation gaps can stop funding because they create uncertainty about who is responsible if something goes wrong.

Here is what helps approval:

- Creditworthy end customer: Established B2B or government buyer with a credible payment pattern.

- Clear, non-cancelable purchase order: Terms that reduce dispute and cancellation risk.

- Reliable supplier: A vendor with a track record, realistic lead times, and no obvious fulfillment concerns.

- Enough gross margin: Room for fees, mistakes, and still a worthwhile profit.

- Clean paperwork: Matching purchase orders, supplier quotes, shipping terms, and delivery requirements.

Here is what causes trouble:

- Low-margin deals that leave little room for fees or delays

- Custom production risk where acceptance depends on subjective buyer approval

- Split or partial shipments with unclear billing and delivery triggers

- Overseas supply chains with vague freight responsibility or title transfer terms

- Customers with deduction habits even if they eventually pay

The underwriting process tells you something useful beyond approval odds. It shows whether this order is helping you build a stronger company or pulling you into a cycle where every new sale needs expensive outside support. Owners who miss that point can end up financing growth that never turns into durable cash flow.

Is PO Financing Right for Your Business

Purchase order financing fits a narrow band of businesses very well. Outside that band, it's usually the wrong tool.

Three businesses that often fit

A consumer products brand selling into a major retailer is a classic example. The buyer issues a meaningful purchase order, the supplier needs money to manufacture the goods, and the brand can't wait for retailer payment terms to clear. In that situation, the financing supports fulfillment without draining cash needed for packaging, freight, or sales operations. Businesses in this position often also look at broader working capital for businesses once order volume becomes more consistent.

An IT or equipment reseller with a government contract can also fit well. The order is for tangible goods, the customer is institutional, and the transaction is defined. The reseller's challenge isn't demand. It's paying vendors upfront while waiting for the government buyer to process the invoice.

A fast-growing importer or exporter is another strong candidate. These businesses often manage supplier lead times, shipping coordination, customs timing, and delayed customer payment all at once. PO financing can be useful when the order is clean and the buyer is strong.

The best-fit borrower doesn't need money because the business is failing. They need money because the order arrives before the cash.

Here's a short explainer that gives a helpful visual overview before you decide whether the structure matches your deal.

Where it usually does not fit

This product usually does not work well for service businesses, construction draws, or direct-to-consumer orders. It also tends to struggle when the goods are heavily customized and the lender sees performance risk rather than simple procurement risk.

It's also a poor fit if your margins are thin, your supplier is unproven, or your customer can cancel the order easily. In those situations, the capital may still exist somewhere in the market, but PO financing is unlikely to be the cleanest or safest option.

If you're financing purchase orders for repeat clients every month, that's another signal to pause. The deal may fit operationally, but the capital stack may already be wrong.

The Benefits Dangers and Critical Exit Strategy

Why owners use it anyway

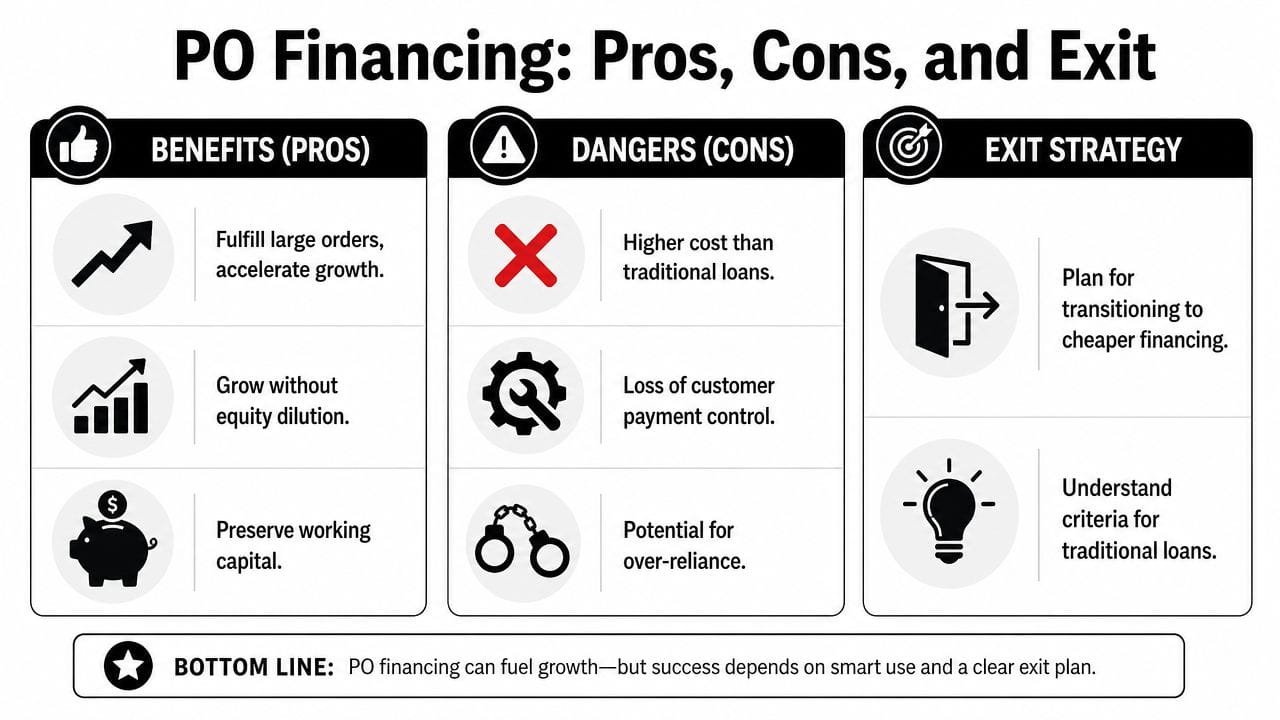

PO financing solves a real operational problem. It lets a business accept larger orders than its cash balance would otherwise support. That can accelerate growth without selling equity and without tying up internal liquidity in one customer shipment.

The practical benefits are easy to see:

- It enables fulfillment: You can take the order instead of turning it down.

- It preserves cash: You don't have to empty the operating account just to start production.

- It matches the transaction: The capital is tied to a specific order, not broad working capital use.

For a company in a growth spurt, that can be the difference between scaling and stalling. Many owners use it once, close the gap, prove demand, and then move into cheaper forms of capital once the sales pattern is established.

The trap most articles skip

The danger isn't just that PO financing is expensive. The bigger danger is staying in it too long.

RangeMe notes that the hidden risk is failing to transition to lower-cost capital after the initial 60-day window. Without a planned exit, the compounded cost at 2% to 4% markup on COGS per month can exceed 30% of gross profit over a year, turning a bridge into a durable drag on margins, as described in RangeMe's article on purchase order financing risks and benefits.

That's the part owners underestimate. One order works. Then another order comes in from the same buyer. Then another. Soon the company is using high-cost transactional capital as if it were a standing facility. Margin gets thinner, supplier negotiations get tighter, and management starts blaming operations when the actual issue is financing structure.

Field note: If PO financing becomes routine, your next move shouldn't be “find another PO funder.” It should be “build the exit.”

A sound exit plan often means moving to a lower-cost option once the goods are delivered and invoiced, or once recurring volume gives a lender confidence to extend more flexible working capital. The details vary, but the principle doesn't. Use PO financing to get through the order. Don't let it become your permanent source of growth capital.

PO Financing vs Other Funding Alternatives

Funding options at a glance

Choosing the right product depends on where the cash gap sits. PO financing is for the period before delivery. That's what makes it different.

| Funding Type | When It's Used | Primary Use Case | Basis for Approval |

|---|---|---|---|

| PO Financing | Before goods are delivered | Paying a supplier to fulfill a confirmed order | Strength of the customer order, buyer quality, supplier reliability |

| Invoice Financing | After goods are delivered and invoiced | Accelerating cash tied up in receivables | Quality of the invoice and the customer's ability to pay |

| Business Line of Credit | Ongoing operating cycle | Flexible access to working capital across repeated needs | Overall business profile, cash flow, and lender criteria |

| Short-Term Loan | Lump-sum need with fixed repayment | Bridging a temporary need not tied to a single order flow | Business performance, repayment ability, and lender credit standards |

For a deeper look at the post-delivery option, invoice factoring is often the natural comparison because it addresses a similar cash conversion problem at a later stage in the transaction.

How to choose the right tool

Ask one question first. Has the product shipped yet?

If the answer is no and the problem is paying the supplier, PO financing may fit. If the answer is yes and the problem is waiting on receivables, invoice financing is usually closer to the need. If this is a recurring pattern across many customers, a line of credit may be more efficient than using an order-by-order product forever.

A short-term loan can work when the use of funds is broader and not tied to one clean transaction. But it won't always solve supplier-control issues, and it may not move fast enough when the order has a tight production clock.

Owners get in trouble when they shop by approval odds instead of fit. The right product is the one that matches the stage of the sale, the type of collateral in the deal, and the way repayment will happen.

Your Application Checklist and Choosing a Partner

What to gather before you apply

A PO financing request usually stalls for ordinary reasons. The purchase order is cancelable. The supplier quote is missing shipping terms. The margin is too thin once fees, freight, duties, and inspection costs are added back in.

A lender is not only checking whether the order is real. They are checking whether the deal can survive a delay, a dispute, or a cost increase without trapping you in expensive funding longer than planned. That matters because a fundamental mistake with PO financing is not using it once. It is staying on it too long because nobody planned the handoff to a cheaper facility.

Bring a file that answers four questions fast: Who is buying, who is supplying, what has to be paid upfront, and how does the lender get taken out at the end?

A practical checklist looks like this:

- Customer purchase order: Clear, current, and hard to cancel. If the order can be changed easily, expect extra scrutiny.

- Supplier paperwork: A proforma invoice or supplier quote showing units, costs, production timing, and payment terms.

- Your sales invoice or margin summary: The lender needs to see the revenue side, but they also need to see enough gross profit left after financing costs.

- Business financials: Recent statements that show you can run the order, absorb normal hiccups, and cover expenses outside this transaction.

- Delivery terms and logistics documents: Incoterms, freight responsibilities, customs details, and inspection requirements matter, especially on cross-border deals.

- Exit plan: State whether payoff comes from customer payment, invoice factoring, an accounts receivable line, or another lower-cost facility.

If you are thinking past a single order, tie this decision back to broader capital structure decisions. The right short-term fix should make your next financing step easier, not more expensive.

What to look for in a financing partner

Start with one question. What does this lender expect the exit to look like?

A good partner can explain that in plain English. They should tell you how fees accrue over time, who pays the supplier, what happens if the shipment slips, whether partial deliveries create problems, and what they want in place before they fund the next order. If the answer is vague, the relationship usually gets expensive fast.

Ask how they handle exceptions. Orders change. Containers get held. Customers pay late. Strong partners have a process for these issues and will tell you where they draw the line. Weak ones talk only about approvals.

Look for a lender that can discuss the next product before you need it. Many businesses outgrow PO financing once orders become repeatable and receivables turn into the stronger collateral. This guide on how to layer multiple financing tools without over-leveraging your small business is useful if you are trying to move from one-off transactional funding to a cleaner, lower-cost structure.

The best financing partner does more than get the deal funded. They help you decide which orders are worth financing, which ones will strain margin, and when it is time to graduate to something cheaper.