You've found a franchise you believe in. The brand is established, the operating model feels proven, and you can see the grand opening in your head. Then the financing conversation starts, and the numbers stop looking like a single franchise fee and start looking like a full business launch.

That's where many first-time buyers get stuck. They ask whether they can get a loan, when the better question is whether they can assemble the right mix of capital for the entire project. A franchise opening usually needs funding for buildout, equipment, inventory, payroll, rent, and reserves, not just the license to operate. Many buyers end up realizing the true issue is, as StartCap notes in its discussion of franchise financing, “How much cash do I really need beyond the franchise fee?” rather than the basic question of whether financing exists.

The strongest franchise financing options usually work as a capital stack. One layer handles long-term assets. Another covers short-term operating gaps. A third comes from your own equity or seller support. When you build that stack well, the financing supports the business. When you build it poorly, the financing starts running the business.

Table of Contents

- Your Dream Franchise Is More Than Just a Fee

- The Foundation Government-Backed SBA Loans

- Exploring Conventional and Alternative Financing

- A Side-by-Side Comparison of Your Top Choices

- Building Your Capital Stack Strategically

- Your Franchise Financing Application Checklist

- From Application to Grand Opening with Confidence

Your Dream Franchise Is More Than Just a Fee

The first budgeting mistake I see is simple. A buyer treats the franchise fee as the deal, when it's really just the admission ticket.

A real opening budget usually extends far beyond that first payment. You may need tenant improvements, signage, furniture, equipment, opening inventory, staff training payroll, rent before revenue is stable, and a reserve for the first months of operation. That's why many discussions of franchise financing options feel incomplete. They explain the loan product, but they don't explain the full cash requirement behind the opening.

The real financing question

A franchise buyer often starts with, “Can I borrow for this?” The sharper question is, “What needs long-term money, what needs flexible money, and what needs my own cash?”

That shift matters because one loan rarely fits every use. If you use a short-payback product to fund a long-lived buildout, you create pressure before the location has had time to mature. If you put everything into one large term loan without preserving liquidity, you may open undercapitalized.

Practical rule: Don't finance your franchise as one purchase. Finance it as a set of different needs with different repayment timelines.

What a complete budget usually includes

Before talking to lenders, break the project into use cases:

- Brand entry costs: Franchise fee, legal review, and any opening obligations tied to the franchisor.

- Physical setup: Buildout, fixtures, furniture, remodeling, and signage.

- Operating launch costs: Inventory, payroll, rent, utilities, and opening marketing.

- Cash cushion: Reserves for delays, slower ramp-up, or supplier timing issues.

That's the point where franchise financing options become easier to evaluate. You stop shopping for one magical loan and start building a structure that gives the business room to breathe.

The Foundation Government-Backed SBA Loans

For a first franchise purchase, SBA-backed lending usually serves as the senior debt layer in the capital stack. It often carries the longest repayment window available to a new operator, which matters when the business is still building sales, staffing up, and absorbing opening costs.

An SBA loan involves three parties: the borrower, the bank, and a federal guaranty that reduces part of the lender's risk. That structure is why banks will often consider deals they might decline on conventional terms alone, especially for first-time franchisees with a solid profile but limited direct operating history.

The 7(a) program is the workhorse. It can cover franchise fees, equipment, buildout, working capital, and even an acquisition of an existing unit if the deal is structured properly. That flexibility makes it a strong base layer when the project has several moving parts and you want one primary loan to anchor them.

The trade-off is paperwork, timing, and use-of-proceeds discipline. SBA money is attractive because it can stretch repayment and improve monthly cash flow. It also comes with tighter documentation, lender scrutiny, and rules around how funds are allocated. Borrowers who treat it like a general pool of cash usually run into trouble. Borrowers who map each dollar to a defined use tend to move faster and close cleaner.

That is why I rarely look at SBA financing as the whole answer. I look at it as the foundation. If the 7(a) handles the long-lived costs, such as acquisition, buildout, and core startup expenses, other products can fill narrower gaps without overloading one facility.

Where 7(a) and 504 fit

The 7(a) program usually fits best when the franchise project includes mixed uses under one roof. A new unit opening might need help with the franchise fee, leasehold improvements, equipment, and opening working capital at the same time. An acquisition might combine business value, furniture and fixtures, and a reserve for transition. 7(a) is designed for that kind of range.

The 504/CDC program is more specialized. It is built for major fixed assets, usually owner-occupied real estate or large equipment purchases, and it can be a strong match for franchisees buying property or funding heavy asset investments tied to expansion. It is less useful when the capital need is mostly goodwill, startup spending, or short-term operating liquidity.

Another practical advantage is eligibility review. If a franchise appears in the SBA Franchise Directory, lenders have one less eligibility issue to sort through. That does not remove underwriting. It does reduce avoidable friction in a process that already asks for plenty of documents.

If you want a clearer breakdown of where each SBA option fits, this comparison of SBA 7(a), 504, and microloans gives a useful side-by-side view.

SBA financing tends to work well in three situations:

- New unit openings: One senior facility can cover several large startup costs with repayment terms that are easier on early cash flow.

- Existing unit acquisitions: The structure can support a purchase that includes business value, equipment, and transition capital.

- Owner-operators protecting liquidity: Lower equity injection requirements than some conventional loans can help preserve cash for the first year of operations.

The limitation is just as important as the benefit. SBA debt is slower to close than many shorter-term products, and it should not be forced onto every need in the deal. A franchise buyer who uses long-term SBA proceeds for the right costs, then layers in other financing where appropriate, usually ends up with a healthier capital stack and more room to operate.

Exploring Conventional and Alternative Financing

A franchise opening rarely gets funded with one loan. The stronger approach is to assign each cost to the financing tool built for it. That is how a capital stack works. Long-term debt carries long-term assets. Flexible credit covers timing gaps. Specialty financing handles assets that can stand on their own.

That distinction matters because franchise budgets are uneven. Equipment, opening inventory, franchise fees, leasehold improvements, training, and early payroll do not behave the same way. Funding all of it with one product usually means at least one part of the deal is poorly matched.

The main tools and where they fit

Conventional bank term loans work best for borrowers who already look bankable on paper. Strong liquidity, clean global cash flow, good collateral, and a lender that knows the franchise brand all help. The trade-off is selectivity. A first-time franchise buyer may find that conventional credit offers good pricing but less flexibility on structure, guarantor strength, or collateral shortfalls.

Franchisor financing can fill a narrow gap. Some brands finance part of the franchise fee, opening package, or required equipment. That support can reduce the amount you need from outside lenders, but it usually covers a slice of the project rather than the whole opening budget. Read the terms carefully. Deferred payments that reset quickly can tighten cash flow right when the location is still ramping.

Equipment financing deserves more attention than it usually gets. If the unit depends on ovens, vehicles, washers, cardio machines, or other revenue-producing equipment, those assets can often support their own financing. That keeps them from crowding out working capital in your senior facility. It also aligns repayment with the useful life of the asset, which is a cleaner structure than paying for five-year equipment with short-term operating money.

Lines of credit solve a different problem. They are built for movement. Payroll timing, inventory purchases, small seasonal swings, and delayed receivables are good uses. Using a line of credit for a permanent project cost creates avoidable pressure because revolving credit is meant to turn, not sit.

Seller financing shows up most often in franchise resales. It can help close a valuation gap or reduce the cash due at closing. I like it best when it supports a deal that already works and the seller has a reason to stay invested in a smooth handoff. If seller paper is the only reason the transaction survives, the buyer should slow down and recheck the assumptions.

Alternative lenders can be useful when timing matters, bank underwriting is too rigid, or a borrower needs a smaller targeted facility alongside the main loan. The key is choosing the right use case. Fast capital is helpful for short-duration needs and specific gaps. It becomes expensive when used as the foundation of the project. Borrowers comparing nonbank products can review these alternative business loan options to see where speed, structure, and cost tend to line up.

Common mistakes in franchise capital stacks

The easiest way to test a financing plan is to ask a simple question: what exactly is this money paying for?

That question exposes the usual mistakes:

- Using short-term working capital for buildout costs. Buildout produces value over years. Short repayment against that cost can choke the business during the first several months.

- Pushing equipment purchases into a general-purpose loan. That uses up borrowing capacity that may be better reserved for softer costs like payroll, opening inventory, and early operating cushion.

- Treating franchisor financing as a full solution. It often helps, but it usually does not cover the broader capital need.

- Leaving no revolving credit in the stack. A unit can be profitable on paper and still hit timing problems in the first year.

There are also equity-style tools that affect the stack differently. Personal cash lowers debt service but reduces the owner's liquidity. Seller support can reduce cash needed at closing but adds another party to the structure. ROBS can supply equity from retirement funds without scheduled loan payments, which helps early cash flow, but the compliance burden is real and mistakes are costly.

A simple rule keeps many first deals out of trouble: borrow short for short-lived needs, borrow long for long-lived assets, and keep enough true working capital to absorb a slower ramp than the pro forma expects.

This is the part many first-time buyers struggle with. They compare products one by one instead of building the stack around the opening plan. A platform like Business Loan Warrior helps by lining up the use of proceeds, lender fit, and timing in one process, so the financing package supports the business you are opening rather than forcing the business to fit the first approval you get.

A Side-by-Side Comparison of Your Top Choices

A buyer gets approved for a solid SBA loan, then realizes at closing that the SBA facility is carrying equipment, startup costs, and a thin working-capital reserve all in one note. The deal still funds, but the structure is doing too many jobs. That usually shows up later in the form of tighter cash flow and less flexibility.

A better comparison starts with function, not product name. Each option below solves a different part of the franchise launch.

Franchise Financing Options at a Glance

| Financing Type | Typical Amount | Interest Rate | Term Length | Best For |

|---|---|---|---|---|

| SBA 7(a) | Varies by lender and project scope | May be fixed or variable, subject to SBA and lender pricing limits | Up to 25 years depending on use of proceeds | Startup costs, equipment, working capital, real estate, acquisitions, refinancing |

| Conventional bank loan | Varies | Varies | Varies | Established borrowers with strong banking relationships and conventional underwriting strength |

| Equipment financing | Typically tied to equipment value | Varies | Structured around the useful life of the equipment | Kitchens, vehicles, laundromat machines, fitness equipment, POS hardware |

| Line of credit | Varies by lender and borrower profile | Varies | Revolving rather than fixed amortization | Payroll gaps, inventory timing, receivable delays, short-term operating swings |

The practical differences matter more than the labels.

SBA 7(a) is usually the most flexible tool in the stack. It can cover a broad mix of costs, which makes it useful for first-time franchise buyers who need one primary facility to anchor the deal. The trade-off is process. Documentation is heavier, lender timelines can stretch, and not every use of proceeds fits as cleanly as borrowers expect.

Conventional bank loans can price well and work for strong borrowers, especially if the business already has history or the guarantor has substantial liquidity. They are less forgiving on startup risk. For a first unit with no operating history, conventional credit is often harder to win than borrowers assume.

Equipment financing works best when the asset has a clear value and a useful life that supports the repayment schedule. It preserves room in the senior loan for softer costs that do not collateralize well. That distinction matters in equipment-heavy concepts.

Lines of credit solve timing problems. They are designed for short gaps, not permanent undercapitalization. If the pro forma only works because the line stays maxed out, the issue is not the credit product. The issue is the capitalization plan.

The right answer is often a stack, not a single loan. An SBA loan may carry franchise fees, buildout, and opening working capital. Equipment financing can sit beside it for revenue-producing assets. A revolving line can protect the first year from timing stress. For a closer look at how those pieces fit together, see this guide on layering multiple financing tools without over-leveraging your small business.

That is the comparison that actually helps. Which product is cheapest matters, but which product belongs in each slot of the capital stack matters more.

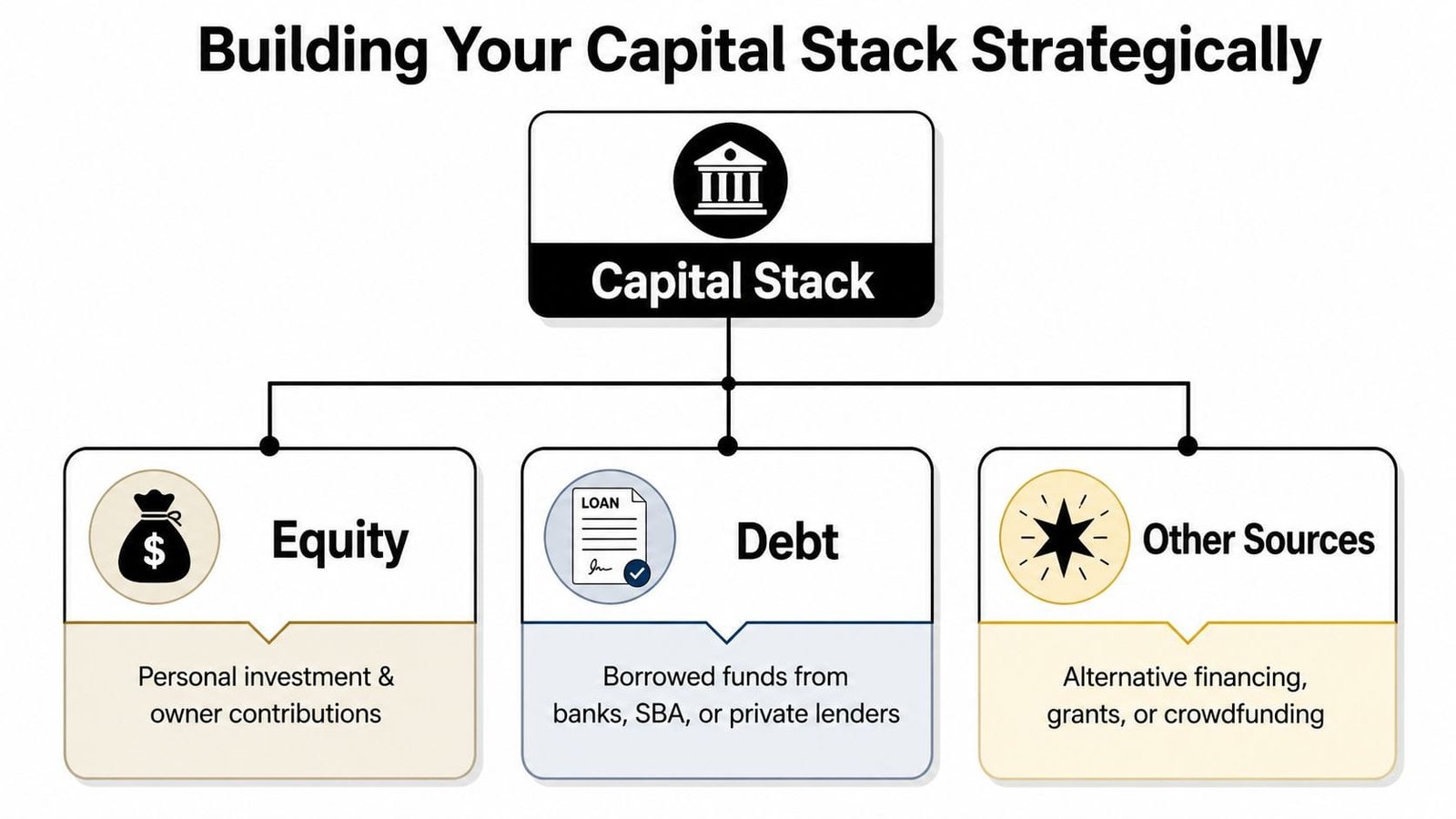

Building Your Capital Stack Strategically

A first-time franchise buyer usually starts with one question: "How much can I borrow?" The better question is, "Which dollars should pay for which job?" That shift changes the outcome.

Good franchise financing starts with structure. Franchise fees, buildout, equipment, opening inventory, payroll cushion, and contingency reserves do not behave the same way. If they are all forced into one loan, the repayment schedule often stops matching the business reality. That is how a deal can close on paper and still feel tight by month three.

Match each layer to its job

The rule is simple. Long-life assets should usually be paired with longer-term debt. Short-term operating swings belong with short-term credit. Owner cash belongs where lenders expect staying power.

In practice, that often looks like this:

- Senior term debt: Best suited for franchise fees, acquisition costs, leasehold improvements, and opening working capital that needs time to convert into stable cash flow.

- Equipment financing: Best suited for ovens, POS systems, refrigeration, fitness machines, or other assets with a clear resale value and a useful operating life.

- Revolving credit: Best suited for timing issues such as payroll, inventory purchases, or receivables lag. It should support the operation, not carry the business.

- Equity contribution: Best suited for down payment requirements, reserve support, and any cost category that should not create immediate monthly debt service.

That is the core of a capital stack. Each layer has a lane.

A fuller explanation of how to layer financing tools without over-leveraging your small business can help if you are pressure-testing your structure before you apply.

A practical stack for a new coffee franchise

Take a new coffee franchise going into a suburban strip center. The project includes the franchise fee, tenant improvements, espresso equipment, smallwares, signage, opening inventory, training travel, and enough cash to absorb a slower first quarter.

One lender may place an SBA 7(a) loan in the senior position to cover the broader startup package. A separate equipment loan may handle the espresso machines, grinders, refrigeration, and POS hardware, especially if that keeps the senior facility cleaner or preserves more working capital. The borrower may also set up a modest line of credit for timing gaps after opening, not as a substitute for adequate capitalization. Then the owner brings in cash equity to satisfy injection requirements and keep real reserves on hand.

That stack is stronger because each piece solves a specific problem. It also gives you room to adjust. If equipment can be financed on its own terms, the senior lender does not have to stretch as far. If reserves stay in cash instead of getting swallowed by buildout overruns, the business has more margin for a slow ramp.

Business Loan Warrior helps simplify that process. Instead of treating franchise financing as a hunt for one approval, the platform helps borrowers sort costs into the right buckets, compare structures across products, and build a stack that fits the unit economics of the concept.

The goal is not to close with the biggest loan. The goal is to open with the right mix of capital, enough flexibility to operate, and debt service the business can carry.

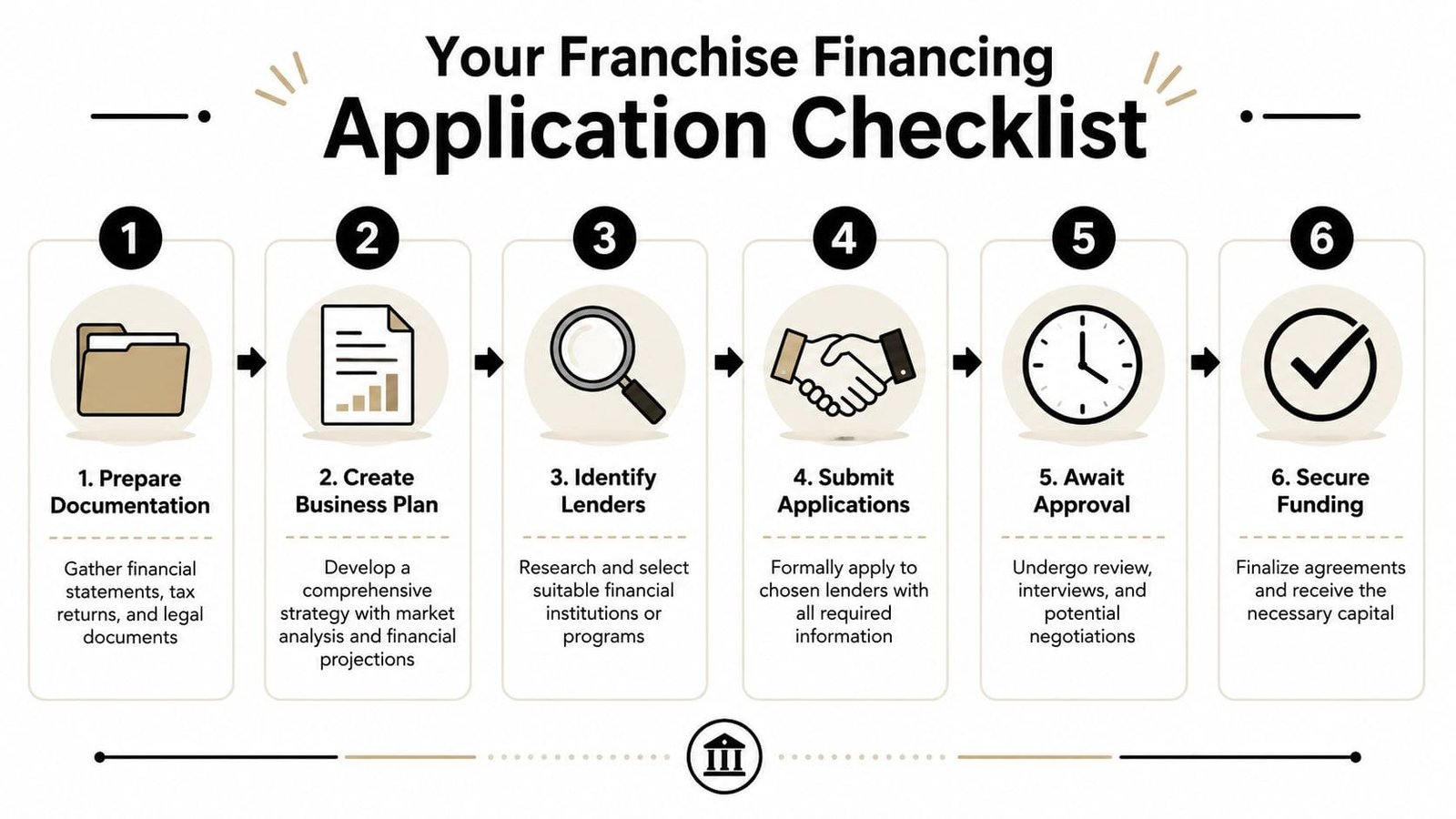

Your Franchise Financing Application Checklist

Most franchise financing applications don't fail because the idea is bad. They fail because the file is incomplete, the use of funds is unclear, or the borrower applies to the wrong channel first.

Documents that usually decide the outcome

Start with a lender-ready package. For franchise buyers, that usually includes the core documents below.

Franchise Disclosure Document

Lenders want to understand the brand, the obligations, and the operating model. Have the full FDD available, not just selected pages.Business plan and use-of-funds breakdown

Show exactly what the capital is paying for. Separate acquisition, buildout, equipment, opening payroll, inventory, and reserves.Personal financial statement

A first location often leans heavily on the owner's financial profile, liquidity, and contingent obligations.Tax returns and bank statements

Lenders use these to check consistency, liquidity, and repayment capacity.Entity and legal documents

Formation paperwork, leases or letters of intent, purchase agreements if acquiring an existing unit, and any seller notes.

Before you submit anything, make sure every document tells the same story. If your plan says one thing and your bank statements suggest another, underwriting slows down fast.

Here's a quick visual guide to the process:

How to move faster without getting sloppy

The process usually improves when you do three things well:

- Know your credit profile: Review personal and business credit before lenders do. Fix obvious reporting issues early.

- Choose lenders by fit: Don't send the same request everywhere. Match the request to the product and lender appetite.

- Prepare for follow-up: Underwriters often need clarification on injection sources, lease terms, or buildout budgets.

For many borrowers, the hardest part isn't the application itself. It's coordinating multiple products without duplicating effort. A platform approach can help by letting you complete a single application, compare loan paths, and keep documents in one place while communicating with underwriters through a central dashboard.

That's one reason many owners prefer fintech-enabled marketplaces over a scattered lender-by-lender search. The simpler the process, the easier it is to build the full stack without losing track of timing.

From Application to Grand Opening with Confidence

The strongest franchise financing options rarely come from one product in isolation. They come from a structure that fits the business you're opening. Senior debt supports the heavy lift. Equipment financing handles asset purchases cleanly. Revolving credit protects cash flow timing. Your equity keeps the whole plan credible.

That's how you move from “Can I get approved?” to “Can this location open on solid financial footing?” The difference is strategy.

The process can feel crowded when you're balancing franchise requirements, lender underwriting, and opening deadlines. But it's manageable when the capital stack is built intentionally and the paperwork is organized from day one.

If you're ready to turn a franchise plan into a workable funding structure, Business Loan Warrior can help simplify the process. Its no-fee application lets you check pre-approval without affecting credit, compare appropriate funding paths, organize documents in one secure dashboard, and connect with underwriters while you build the right mix of capital for your opening.