A lot of owners land on Headway Capital when they're under pressure, not when they have the luxury of building a perfect capital plan. A supplier pays late. Inventory has to be ordered now. Payroll lands before receivables clear. You need money for a business reason that makes sense, but time is the primary problem.

That's where fast online lenders get attention. They promise speed, lighter qualification standards, and a simpler path than a bank. Sometimes that's exactly what a business needs. Sometimes it's the financial equivalent of using a very expensive wrench on a problem that really calls for a full toolbox.

Headway Capital fits a narrow but real use case. It can work when the job is short-term working capital and the business can repay quickly. It becomes much less attractive when an owner starts using it for long-term growth, equipment, buildouts, or recurring structural cash flow problems.

Table of Contents

- Your Business Needs Cash Fast What Are Your Options

- What Exactly Is Headway Capital

- Calculating the True Cost of a Headway Capital Loan

- Who Is an Ideal Borrower for Headway Capital

- The Application and Funding Process Explained

- Headway Capital Strengths and Weaknesses

- How Headway Capital Compares to Other Lenders

- The Final Verdict and Your Next Step

Your Business Needs Cash Fast What Are Your Options

A restaurant owner gets hit with a walk-in cooler repair right before a busy weekend. A distributor has a chance to buy inventory at a strong margin, but the vendor wants payment before customer checks arrive. A service company lands a large job and needs to float labor before the first invoice gets paid.

Those are normal business problems. They're also the exact moments when owners start searching for fast funding and end up comparing online lenders, merchant cash advances, short-term loans, and lines of credit. The hard part isn't finding offers. The hard part is figuring out which product matches the problem.

Headway Capital sits in the fast-access category. That makes it worth looking at if your problem is immediate and short-lived. If you're trying to sort through the broader quick-cash options, this guide to three types of quick short-term business loans for instant cash flow gives a useful frame for comparing speed against cost.

Fast money can solve a timing issue. It usually doesn't solve a business model issue.

That distinction matters. If you need a short bridge, a high-cost credit line may be acceptable. If your business is growing and needs better structured capital, speed alone isn't enough.

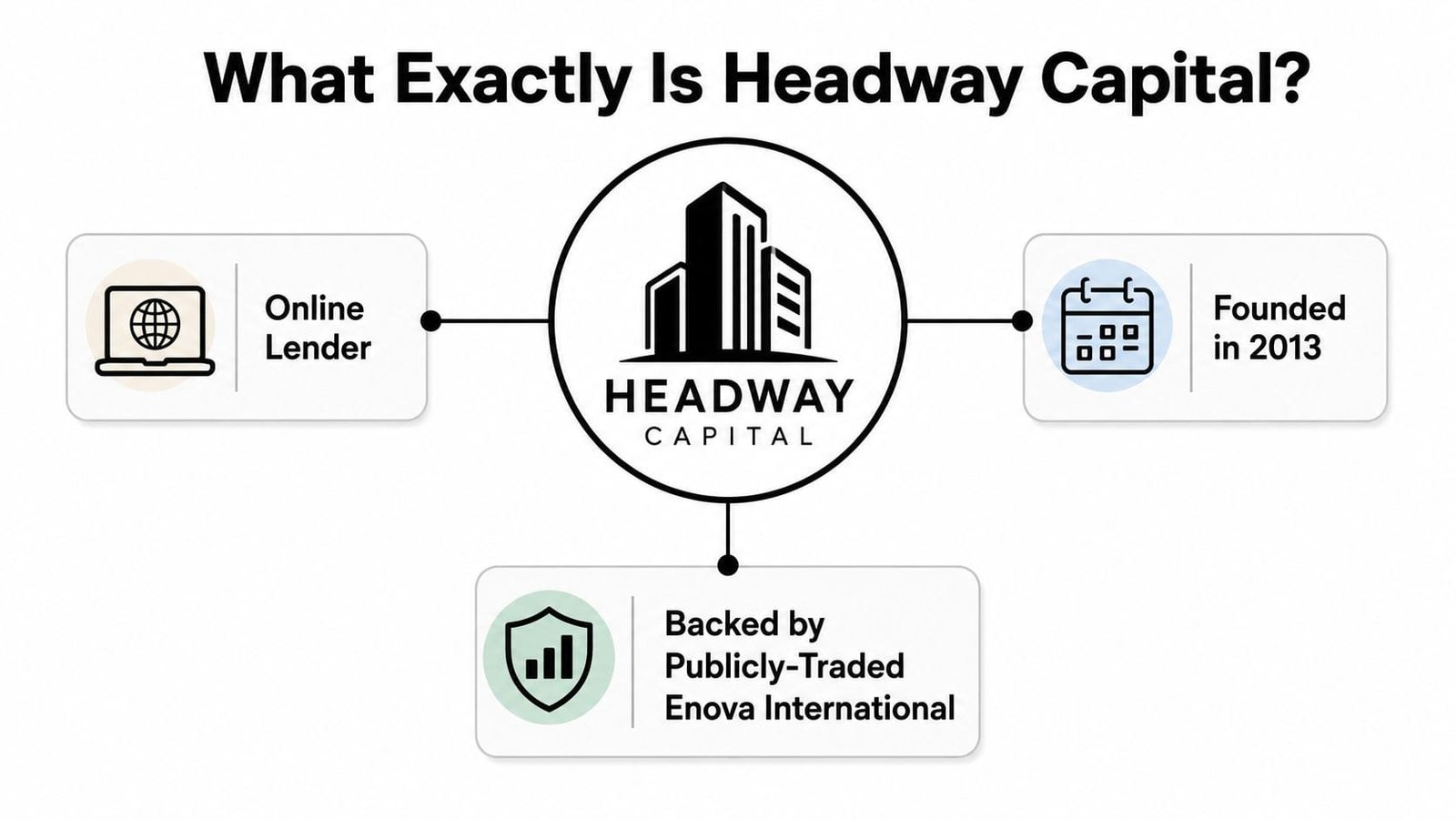

What Exactly Is Headway Capital

Headway Capital is an online lender focused on one product category: a revolving business line of credit for short-term working capital. In plain terms, it is built for timing gaps, not long-horizon growth financing. That distinction matters because many owners apply for a fast credit line when what they really need is a lower-cost loan with a longer repayment structure.

The company operates online and serves small businesses that need access to capital quickly. Its parent company is Enova International, a public company, which gives borrowers some context on the size and ownership behind the brand. More important than the corporate background, though, is the job the product is meant to do.

A Headway Capital line works like a business credit card with fixed payoff terms attached to each draw. You draw part of the approved amount when needed, repay over time, and regain access to available credit as the balance comes down. That setup can be useful if cash comes in unevenly but predictably enough to pay the line back on schedule.

One point causes confusion. Headway Capital the lender is separate from Headway Capital Partners, which is a private equity firm focused on buyouts and sponsor-backed deals, as shown on Headway Capital Partners. Business owners looking for operating cash are dealing with the lender, not the investment firm.

The practical use cases are pretty narrow, and that is not a criticism. It is the right tool for short inventory turns, a temporary receivables gap, urgent repairs, or payroll that needs to clear before customer payments hit. It is usually the wrong tool for buying a second location, refinancing existing debt, or funding a multi-month expansion plan.

That is the key lens for evaluating Headway Capital. It can solve an expensive short-term problem if the return is clear and the payoff window is short. Once a business has steadier revenue, stronger credit, or a financing need that lasts longer than a brief cash cycle, it usually makes sense to graduate to lower-cost capital. If you want a cleaner framework for that decision, this guide on how to calculate the real cost of a small business loan without the headache helps compare speed against total borrowing cost.

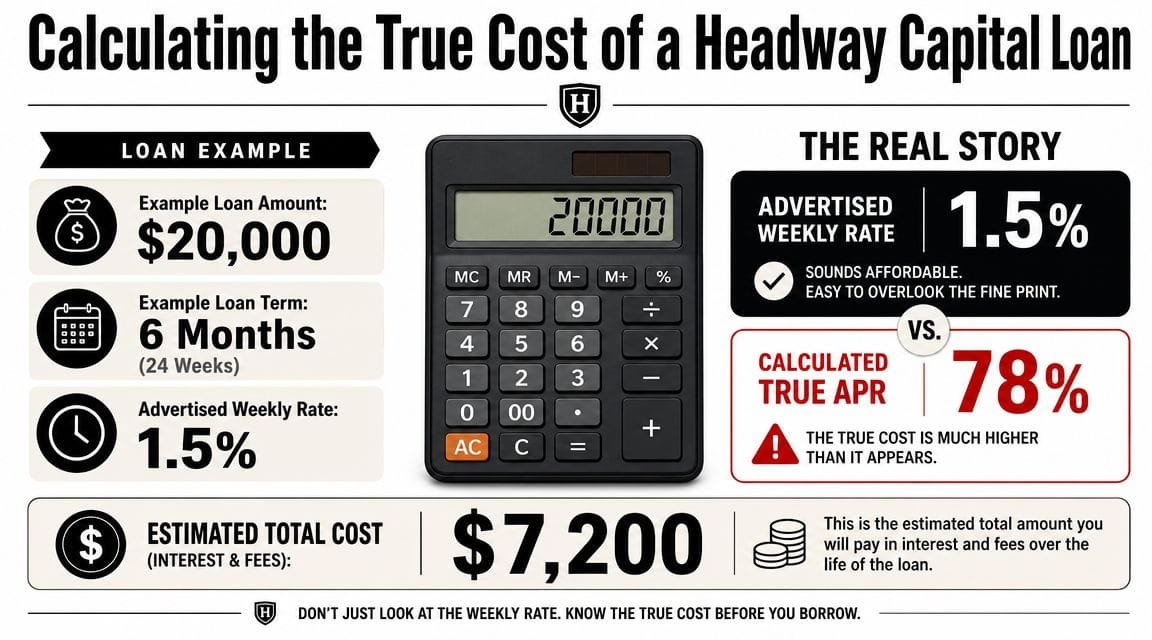

Calculating the True Cost of a Headway Capital Loan

What you pay for access

Many owners make the wrong call. Their focus is on approval and speed, neglecting the full borrowing cost.

Independent reviews cite Headway Capital pricing that starts at a 3.3% monthly interest rate plus a 2% draw fee in most states. The same review also notes that interest does not compound and there is no prepayment penalty (LendingTree's Headway Capital review).

That fee structure matters more than many borrowers expect. With a revolving line, every draw feels small and manageable. But each draw can carry its own cost. If you tap the line often, the fee friction adds up quickly.

A practical way to evaluate any offer like this is to ask three questions:

- How long will the money be outstanding

- How often will I need to draw

- What specific profit or cash protection does this draw create

If you want a better framework for comparing offers, this walkthrough on how to calculate the real cost of a small business loan without the headache is worth using before you sign anything.

When the cost can still make sense

High cost doesn't automatically mean bad product. It means the margin for error is small.

A line like this can make sense if the business uses it for a short, specific purpose and exits fast. If a draw helps you capture inventory that turns quickly, avoid a payroll miss, or bridge receivables you know are coming in, the premium may be tolerable. If you keep a balance out of habit, it usually stops making economic sense.

Practical rule: Expensive capital is acceptable only when the business can point to a clear, near-term payoff or risk avoided.

Here's the trap owners fall into:

| Use case | Fit |

|---|---|

| Temporary working capital gap | Reasonable |

| One-time inventory opportunity | Possible fit |

| Habitual monthly shortfall | Poor fit |

| Equipment purchase | Poor fit |

| Expansion project | Poor fit |

The absence of compounding interest and the lack of a prepayment penalty are real positives. They give disciplined borrowers a way to cut total cost by paying down fast. But that only helps if the business has a short repayment path. If it doesn't, the structure gets expensive in a hurry.

Who Is an Ideal Borrower for Headway Capital

Who tends to fit

Independent reviewer data suggests a business typically needs at least 12 months in operation, $50,000+ in annual revenue, and a minimum credit score of 560 to qualify (Prospeo company profile for Headway Capital).

That profile tells you a lot. Headway Capital isn't really aimed at true startups with no track record. It's more appropriate for an operating business that has some revenue history, fair credit, and a short-term cash need that a bank might not move fast enough to cover.

The ideal borrower usually looks like this:

- Established but not bank-perfect: The business has history and revenue, but not the profile a traditional bank loves.

- Operationally stable: The company can repay from normal business activity, not wishful thinking.

- Using funds tactically: The draw covers timing, not long-range transformation.

- Comfortable with premium pricing: The owner understands speed costs money.

Who should probably look elsewhere

If your business needs more than a working-capital patch, this probably isn't your best lane.

A company doing larger volume, especially one dealing with heavy inventory, equipment, construction, acquisitions, or multi-site expansion, can outgrow this kind of facility fast. The issue isn't only cost. It's also product fit. A revolving line with a relatively modest ceiling can help smooth operations. It won't usually support serious scale-up plans.

If the financing need lasts longer than the cash gap, the product is usually wrong.

Headway Capital also isn't a great fit for businesses that are already borrowing to keep up with recurring cash strain. In that case, the line can become a pressure valve, not a solution. Owners in that position should step back and ask whether they need a better capital structure, a different repayment profile, or operational changes in receivables and margin management.

The Application and Funding Process Explained

A typical Headway Capital application starts the same way many cash crunches start. Payroll hits Friday, a customer pays next week, and the owner needs to know whether this line can close fast enough to matter.

The process is online, which helps on speed. It also means underwriting depends heavily on what your documents show, not how well you tell the story. Clean records usually beat a strong sales pitch.

Headway Capital generally asks for the basics you would expect from a working-capital lender:

- Business details: Legal name, entity type, time in business, and contact information

- Owner information: Identity details and ownership stake

- Revenue documentation: Information that shows the business can support repayment

- Business bank statements: Recent account history to verify deposits and cash flow patterns

Preparation matters more here than owners expect. If deposits are inconsistent, business records do not match the application, or statements raise avoidable questions, the file slows down.

What the timeline usually means in real life

Headway Capital promotes fast decisions and, in some cases, next-business-day funding, as noted earlier. Treat that as the best-case scenario.

In practice, speed depends on three things. Whether the application is complete, whether the bank activity is easy to follow, and whether underwriting sees a clear path to repayment from normal operations. If any one of those breaks down, the clock stretches.

I tell owners to think about this process the same way they think about shipping. Overnight delivery only works if the package is ready to go.

That matters because this product is usually used for short-term, expensive working capital. If the money arrives too late, you still carry the high cost without getting the full benefit. A fast line only does its job when timing is tight and the draw solves a specific problem.

Before applying, get your paperwork in order first. That small step often does more for approval speed than anything you type into the form.

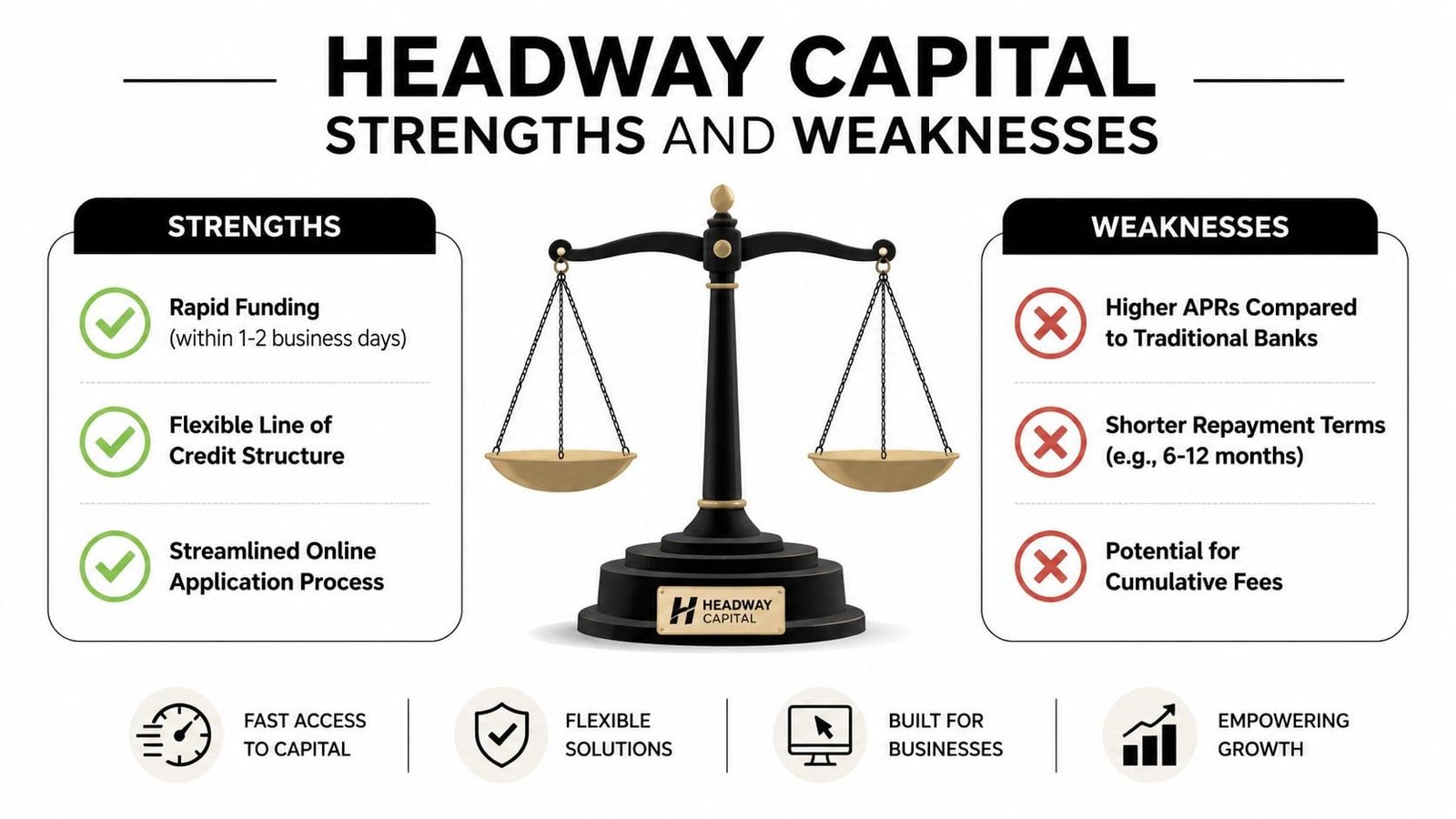

Headway Capital Strengths and Weaknesses

Headway Capital has a real place in the market. It also has very clear limits. If you understand both, the product is easier to judge.

Here's a visual summary before the deeper take.

Where it earns its place

The biggest strength is simple. It offers speed plus access for businesses that may not qualify cleanly with a traditional bank.

A revolving line is also more flexible than a one-time lump sum loan when the need changes month to month. If a business only wants to draw when necessary, that structure can be useful. It's especially practical for uneven cash cycles and short operational gaps.

A few strengths stand out:

- Fast turnaround: Good fit when timing matters more than perfect pricing.

- Reusable access to capital: Helpful for cyclical businesses and uneven collections.

- Fair-credit accessibility: More realistic for some owners than bank underwriting.

- Early payoff flexibility: No prepayment penalty helps disciplined borrowers reduce cost.

This video gives an additional overview of small-business funding trade-offs in this category.

Where it breaks down

The biggest weakness is cost. Independent review coverage notes estimated APRs can range from 39% to 82%, and the line tops out at $100,000, which makes it expensive and limited for anything beyond very short-term liquidity management (NerdWallet's Headway Capital review).

That creates a narrow window where the product works well. Outside that window, it gets hard to defend.

| Strength | Why it matters | Weakness | Why it matters |

|---|---|---|---|

| Fast funding | Helps with urgent needs | High APR range | Cost can overwhelm benefit |

| Revolving structure | Good for repeat short draws | Modest ceiling | Limits usefulness for larger firms |

| Accessible underwriting | More owners can qualify | Not ideal for long-term use | Expensive to carry |

| No prepayment penalty | Encourages quick payoff | Draw fees | Frequent use can get costly |

A strong emergency tool can still be a poor growth tool.

That's the right way to think about Headway Capital. It's not automatically good or bad. It's specific.

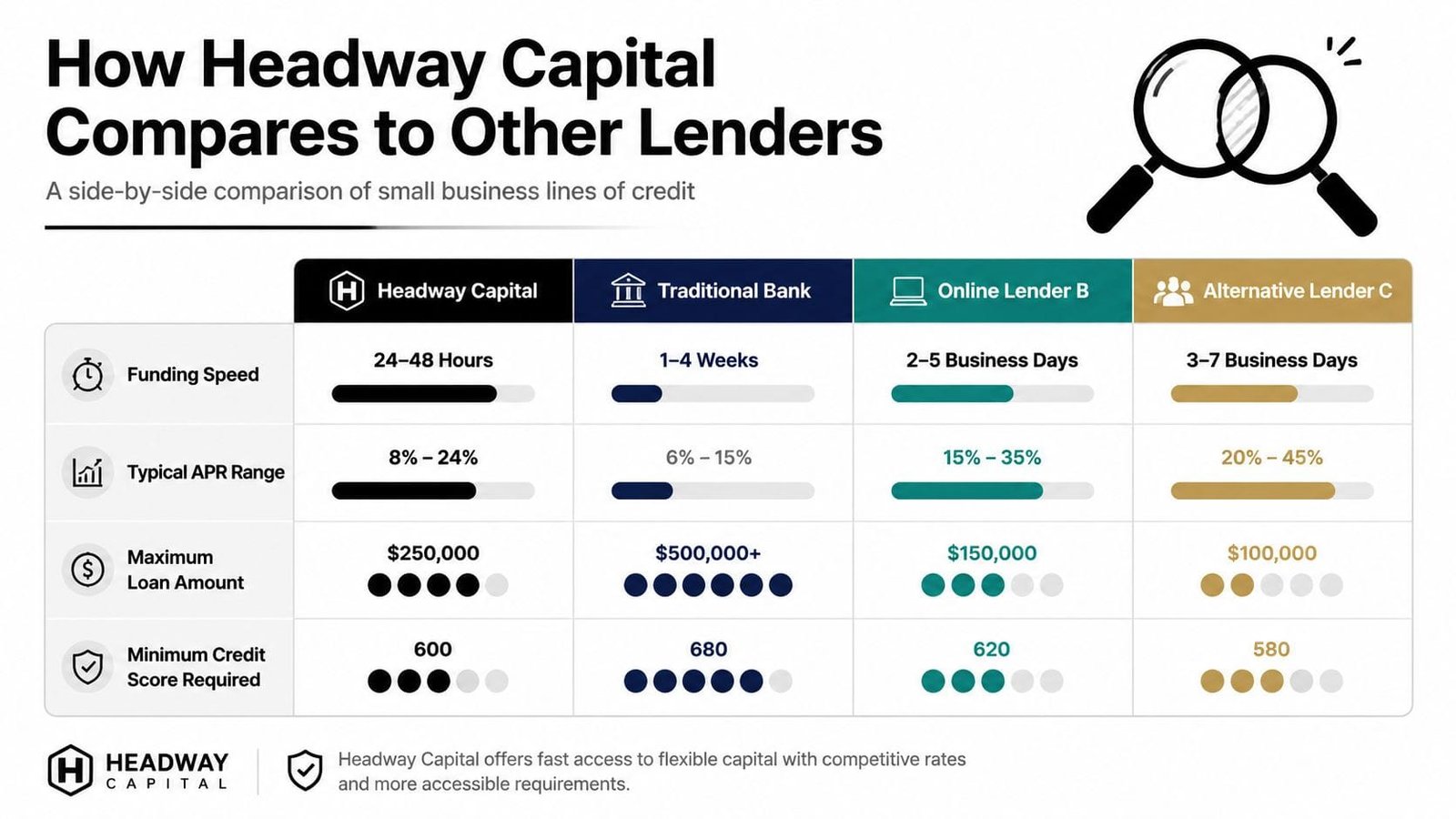

How Headway Capital Compares to Other Lenders

A business owner with payroll due Friday does not shop the same way as an owner planning a second location for next year. That distinction matters more than the lender's brand name.

Headway Capital belongs in the first bucket. As noted earlier, it offers a revolving line meant for short-term working capital. That makes it useful for timing gaps, uneven receivables, and urgent operating needs. It does not fit larger projects that need lower monthly payments, longer repayment periods, or a lower all-in borrowing cost.

Banks sit on the opposite side of the spectrum. Approval usually takes longer. Documentation is heavier. Credit standards are tighter. In return, qualified businesses often get cheaper capital and a structure that makes more sense for equipment purchases, refinancing, expansion, or other investments that should pay off over years, not weeks.

SBA financing often works well for established companies that can wait through underwriting and want a loan built for breathing room. If the goal is growth, a longer runway matters. A high-cost credit line can solve a short cash squeeze, but it is a poor way to finance a project that will take time to produce returns.

Here is the practical comparison:

- Headway Capital: Best for fast, short-duration working capital when speed matters more than price.

- Bank loan: Better for stronger businesses that want lower-cost capital and can wait.

- SBA financing: Better for planned growth, larger uses of funds, and repayment stability.

The bigger comparison is not just lender versus lender. It is single-product lender versus broader search.

When a business applies directly to a lender that mainly offers one structure, the answer usually stays inside that structure. If the business really needs a term loan, equipment financing, or an SBA product, a credit line offer can still look tempting because it is available now. That is how owners end up using expensive short-term money for jobs it was never built to do.

A broader platform can help you compare products before you commit. This guide to alternative business loans is a useful place to start if you want to compare lines of credit with term loans, equipment financing, and other nonbank options.

| Product type | Usually strongest for | Usually weakest for |

|---|---|---|

| Online revolving line | Cash flow gaps, urgent expenses, short repayment cycles | Expansion, refinancing, long-horizon projects |

| Bank term loan | Planned borrowing, lower-cost capital, larger investments | Immediate funding needs |

| SBA-backed loan | Growth capital, longer repayment terms, payment stability | Last-minute cash needs |

| Equipment financing | Vehicles, machinery, asset purchases | General operating shortfalls |

Here is the graduation point I watch for. If the business keeps returning to short-term credit for recurring needs, or if the amount needed is growing, the problem usually is no longer a temporary cash gap. It is a capital structure issue. At that stage, the right move is usually to leave emergency-style funding behind and shop for financing built for growth.

Headway Capital can do its job well. That job is narrow. Use it like a fire extinguisher, not like your HVAC system.

The Final Verdict and Your Next Step

Headway Capital makes sense for a business that needs short-term working capital fast, can handle a high-cost structure, and has a clear plan to pay the draw down quickly. In that lane, it can do its job well. The revolving format is useful. The speed is valuable. The easier qualification profile opens doors that banks often won't.

But this is not the product I'd point most growth-oriented businesses toward for major financing decisions. If the need is expansion, equipment, construction, acquisition, or finding the best available structure for a stronger company, Headway Capital is usually too expensive and too limited.

The bigger mistake isn't taking expensive money once for a real emergency. The bigger mistake is staying in emergency-capital products after the business has outgrown them.

If that's where you are, your next move should be simple. Define the actual job the capital needs to do. Then compare multiple structures before you accept a single lender's offer. Short-term liquidity, long-term growth, and asset-backed borrowing should not be financed the same way.

If you want to see whether a better-fit option exists before committing to a high-cost credit line, take a look at Business Loan Warrior. A single no-fee application can help you compare funding paths across products like term loans, SBA financing, lines of credit, equipment loans, and other business funding options, so you're choosing the right tool for the job instead of defaulting to the fastest offer.