You're probably looking at two screens right now. One shows an income statement with solid profit. The other is your bank balance, and it feels tighter than it should.

That disconnect gets stressful fast when you're applying for a loan. The lender doesn't just want proof that your business can earn money on paper. They want to know whether your operations produce cash, whether your working capital is under control, and whether a repayment plan fits the way money moves through your business.

That's where the statement of cash flows matters. And for most businesses, the operating section is presented using the indirect method for statement of cash flows, which starts with net income and adjusts it into actual cash from operations. As CFI explains in its guide to the indirect method, this format is dominant in practice because it makes the bridge between earnings quality and liquidity explicit for analysts and lenders.

Table of Contents

- Why Your Profits Dont Match Your Bank Account

- What Is the Indirect Method The Big Picture

- The Core Adjustments From Net Income to Cash Flow

- A Worked Example A Small Business Scenario

- Indirect Method vs Direct Method What Lenders See

- Common Mistakes to Avoid on Your Loan Application

- What Your Cash Flow Statement Tells a Lender

Why Your Profits Dont Match Your Bank Account

A business owner can finish a strong quarter, approve bonuses, and still hesitate before opening the operating account. That's not unusual. It happens when profit and cash are moving on different timetables.

A simple version looks like this. You made sales, but some customers haven't paid yet. You bought inventory ahead of demand. You paid down vendors faster than usual. Your income statement still shows profit because accrual accounting records revenue when earned and expenses when incurred, not when cash changes hands.

To a lender, that gap matters more than most owners expect. A bank or underwriter isn't only asking, “Are you profitable?” They're asking, “Can this business turn profit into usable cash without constant strain?”

The lender's concern is practical

If your loan payment comes due every month, the lender wants confidence that your operations generate enough cash to support it. Strong revenue helps. So does margin. But neither answers the cash question on its own.

That's why the cash flow statement becomes so important during underwriting. It explains why cash increased, why it didn't, or why it fell even when the income statement looked healthy.

Practical rule: Profit tells a lender your business model works. Cash flow tells them whether repayment is realistic.

Owners who understand this usually prepare better loan files. They don't just submit statements. They explain them. If cash has been tight because receivables stretched or inventory built before a seasonal push, that story needs to be clear and grounded in the numbers. If you need help tightening operations before you apply, this guide on how to improve cash flow is a useful companion.

Why this format keeps showing up

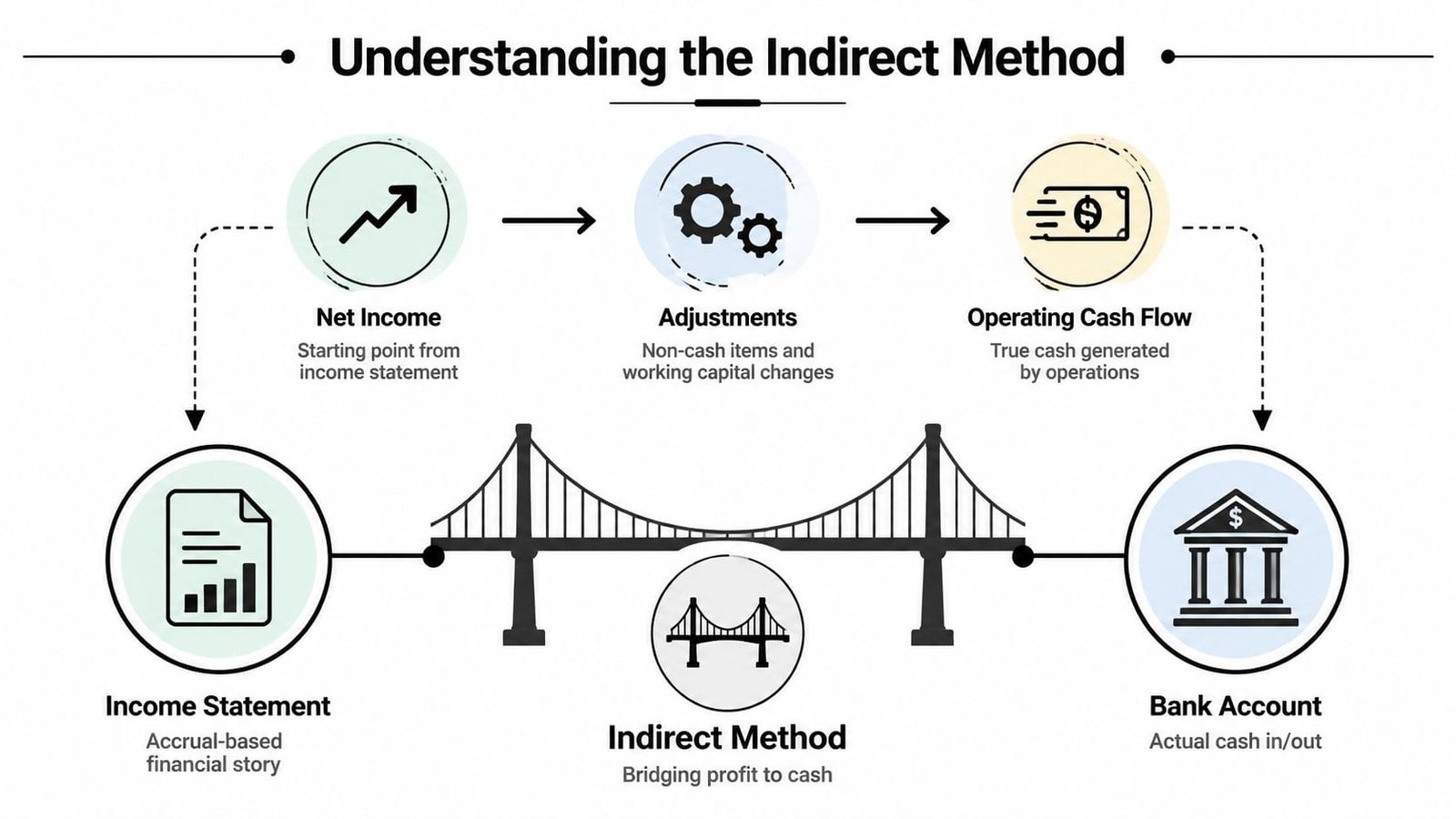

The operating section of the cash flow statement is usually presented through the indirect method. It starts with net income and then adjusts for items that affected accounting profit but not cash, plus changes in working capital.

That structure is useful in lending because it shows where cash got tied up. It also shows whether reported earnings are supported by actual operating liquidity, which is exactly the issue an underwriter cares about when reviewing a loan request.

What Is the Indirect Method The Big Picture

Think of your income statement as one version of the story and your bank account as another. The indirect method for statement of cash flows is the translator between the two.

It does not rebuild your cash activity line by line from scratch. Instead, it starts with net income and adjusts that figure until it reaches cash from operating activities. That reconciliation is the heart of the method.

Why accountants and lenders rely on it

This format is common because it works with financial statements most businesses already produce. You begin with the bottom line from the income statement, then use balance sheet changes and a few key adjustments to show what happened to cash.

Major finance references note that most companies use the indirect method because it reconciles accrual-based net income to cash from operating activities, as explained in CFI's overview of the statement of cash flows.

That matters for a borrower because lenders are used to reading it. They know where to look for non-cash expenses, where to spot unusual working-capital swings, and where to test whether your reported earnings convert into liquidity.

A clean analogy for busy owners

If the income statement is your business written in the language of promises, invoices, and accrued expenses, the cash flow statement rewrites it in the language of money received and money spent.

The indirect method does that translation in three broad moves:

- It starts with profit: Net income is the opening number.

- It strips out accounting entries that didn't use cash: Depreciation is the classic example.

- It captures timing differences: Receivables, inventory, and payables can all change cash without changing profit in the same way.

The indirect method is less about math tricks and more about timing. It answers one blunt question. How much cash did the business operations actually produce?

That's why this statement becomes powerful in a loan package. It doesn't just say the business earned money. It shows whether those earnings are turning into something a lender can trust.

The Core Adjustments From Net Income to Cash Flow

The mechanics of the indirect method are where many owners tune out. Don't. This is the part lenders read closely because it shows whether cash pressure is temporary, structural, or self-inflicted.

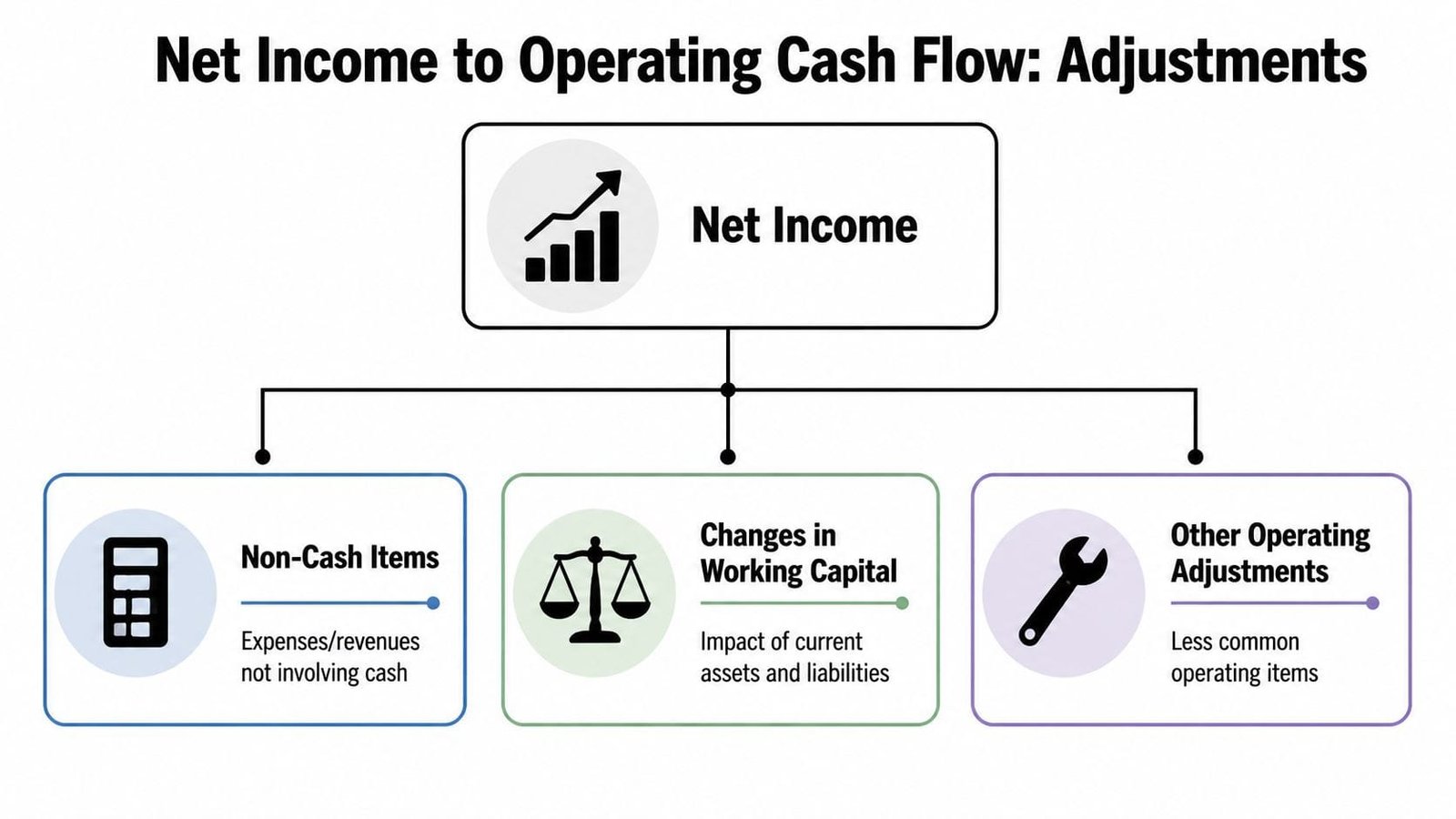

At a practical level, the method starts with net income and makes a series of adjustments. Some are simple. Others reveal how your business is really being managed.

Start with net income and question every non-cash item

The first category is non-cash expenses. These reduce net income, but no cash left the bank when they were recorded.

Depreciation and amortization are the usual examples. If your income statement includes depreciation expense, that lowered profit, but you didn't write a current-period check labeled “depreciation.” So in the indirect method, you add it back.

A useful way to think about it is this: if an expense hurt profit but didn't consume cash this period, it likely needs to be reversed in the operating cash flow section.

For owners who want a quick refresher on the starting line, here's a plain-English guide on how to find net income.

A short explainer helps here:

Remove items that belong somewhere else

The second category is non-operating gains or losses. These can distort operating cash flow if you leave them in.

Say you sold a piece of equipment and recognized a gain. That gain increased net income, but it doesn't belong in operating cash flow because the cash from selling the asset belongs in investing activities. So you reverse the gain out of the operating section.

The rule is straightforward:

- If a gain increased net income but came from a non-operating event: subtract it from operating cash flow.

- If a loss reduced net income but came from a non-operating event: add it back in the operating section.

This is one of the spots where owners make classification mistakes in lender packages. The bank may not call it out immediately, but it affects how they read the quality of earnings.

Watch working capital like a lender does

Working capital adjustments are where the true story usually lives. Yale's accounting materials explain the indirect method as a decomposition of operating cash flow into accounting buckets, including non-cash items, non-operating items, and working-capital movements. That framework also shows why rapid inventory growth or slower receivables collection can reduce cash even when earnings stay steady, as outlined in Yale's explanation of the mathematics of the indirect method.

Here's the lender-friendly version.

| Working capital account | What an increase usually means for cash | What a decrease usually means for cash |

|---|---|---|

| Accounts receivable | Cash is tied up, so it reduces operating cash flow | Cash is collected, so it helps operating cash flow |

| Inventory | Cash was spent on stock, so it reduces operating cash flow | Cash is released, so it helps operating cash flow |

| Accounts payable | Cash is preserved, so it helps operating cash flow | Cash was paid out, so it reduces operating cash flow |

Here, profitable companies get squeezed.

You can grow sales aggressively, extend generous terms, and show strong earnings. But if receivables rise faster than collections, cash gets trapped. You can prepare for demand by buying inventory, but cash leaves before the sales arrive. You can keep vendors happy by paying quickly, but that may tighten your operating account.

When I review loan files, the most common issue isn't weak profit. It's a business that grew faster than its working capital discipline.

A lender usually reads these adjustments as signals:

- Rising receivables: Are customers slowing down, or are credit terms too loose?

- Expanding inventory: Is this planned growth, poor forecasting, or aging stock?

- Shrinking payables: Did the company choose to pay down vendors faster, or are suppliers tightening terms?

The numbers matter, but the explanation matters too. If you can connect the adjustment to a business decision and show control over it, the same cash flow statement that might have looked concerning can become a sign of sound management.

A Worked Example A Small Business Scenario

Abstract explanations only go so far. Let's make this concrete with a fictional business called Precision Parts LLC, a small manufacturer applying for an expansion loan.

The owner submits an income statement showing healthy profit. Then the lender notices that cash from operations is much lower than expected. The indirect method explains why.

The setup

Precision Parts LLC reports the following for the year:

| Description | Amount |

|---|---|

| Net income | Healthy positive profit |

| Depreciation expense | Recorded on the income statement |

| Gain on sale of old equipment | Included in net income |

| Accounts receivable | Higher than last year |

| Inventory | Higher than last year |

| Accounts payable | Lower than last year |

Nothing here is alarming by itself. In fact, this pattern is common in a growing manufacturing company. The owner extended credit to customers, stocked more raw materials ahead of larger orders, and paid suppliers down to maintain relationships.

The problem is that each of those choices affects cash differently than it affects profit.

Building the operating cash flow section

Here's how the indirect method would be built conceptually for Precision Parts LLC.

| Description | Amount |

|---|---|

| Net income | Start here |

| Add back depreciation | Increases operating cash flow because it was non-cash |

| Subtract gain on equipment sale | Removes non-operating gain from operating section |

| Subtract increase in accounts receivable | Cash hasn't been collected yet |

| Subtract increase in inventory | Cash was used to build stock |

| Subtract decrease in accounts payable | Cash went out to vendors |

| Net cash from operating activities | Lower than net income |

That final line is the one a lender focuses on. Not because profit doesn't matter, but because this line shows how much cash the business's operations generated after the normal timing distortions are cleared up.

A lender reviewing Precision Parts LLC would likely ask a few follow-up questions:

- On receivables: Are larger customers taking longer to pay, or did the company sell more on terms?

- On inventory: Is the build intentional because demand is rising, or is product sitting too long?

- On payables: Was the reduction a strategic move to improve vendor relationships?

Those questions aren't traps. They're underwriting questions. If the owner can answer them clearly, the cash flow statement starts to support the application instead of weakening it.

A good cash flow story doesn't require perfect numbers. It requires numbers that make sense together.

This is why I tell owners to rehearse their indirect-method walk-through before sending a lender package. If your net income is strong but operating cash flow is softer, you need a crisp explanation. “We grew receivables because we landed larger accounts and collections are catching up” is better than “I'm not sure why cash is lower.”

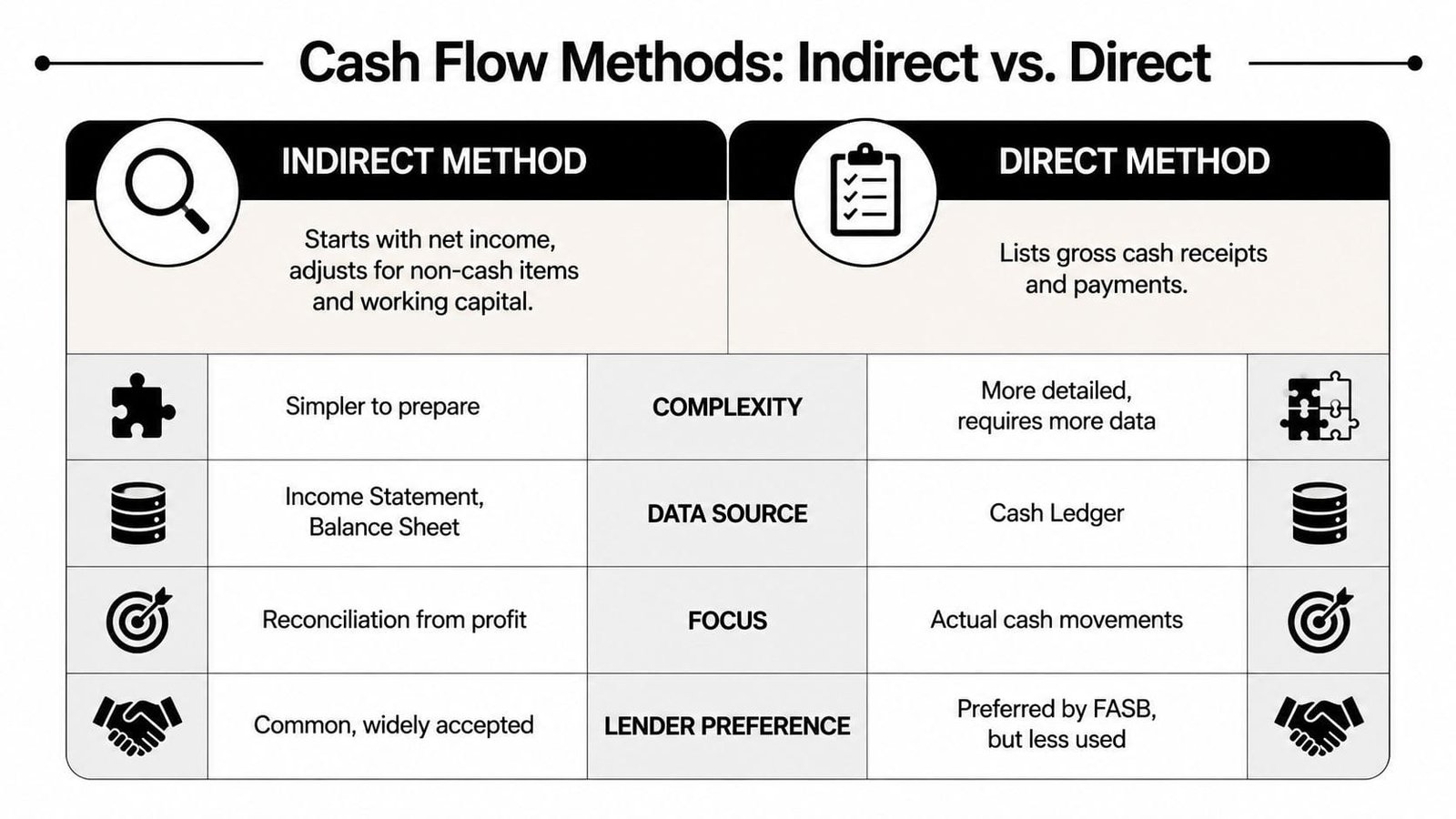

Indirect Method vs Direct Method What Lenders See

Both the indirect and direct methods report operating cash flow. The difference is presentation. For a loan application, that difference matters because each format highlights a different story.

Two formats, different stories

The direct method lists actual cash receipts and payments. It reads more like a checkbook summary. Cash received from customers. Cash paid to suppliers. Cash paid for payroll. It's intuitive.

The indirect method starts with net income and reconciles to cash from operations by adjusting for non-cash items and working-capital changes. It reads more like an explanation.

Here's a side-by-side view:

| Method | What it emphasizes | What it's like to read |

|---|---|---|

| Indirect | How profit turns into cash | A bridge from earnings to liquidity |

| Direct | Where cash physically came from and went | A list of receipts and payments |

Why lenders tend to like the indirect view

For underwriting, the indirect method often does a better job of exposing what lenders care about. It doesn't just show cash movement. It shows why cash and profit diverged.

That matters because, as noted earlier, working capital can change cash dramatically without changing reported earnings in the same way. A lender wants to see those mechanics plainly. If inventory jumped or receivables stretched, the indirect method surfaces it quickly.

This is the practical trade-off:

- Direct method strength: Easier for non-accountants to understand at a glance.

- Direct method weakness: It doesn't naturally show the bridge from accrual profit to operating cash.

- Indirect method strength: It highlights earnings quality and working-capital discipline.

- Indirect method weakness: It can feel less intuitive if you haven't worked with financial statements much.

For a lender, the indirect method often fits the job better because it answers underwriting questions directly. Is profit backed by cash generation? Are current assets consuming cash? Are liabilities temporarily supporting liquidity?

If you're presenting a business for financing, the indirect method usually gives the cleaner credit story.

Common Mistakes to Avoid on Your Loan Application

Loan packages often get weakened by avoidable cash flow mistakes. The issue usually isn't fraud or sloppiness. It's that the owner submits statements without understanding what the lender will zero in on.

Red flags that weaken your file

One common mistake is treating the cash flow statement like a compliance document instead of a credit document. If operating cash flow differs sharply from net income, and there's no explanation, the lender fills in the blanks. Usually conservatively.

Another mistake is mishandling working capital adjustments. Owners often know receivables, inventory, and payables matter, but they can't explain the direction of the impact. That creates doubt fast.

Watch for these issues:

- Unexplained receivables growth: If customers are taking longer to pay, be ready to say why and what you're doing about it.

- Inventory buildup without context: A lender may see excess stock unless you connect it to demand, seasonality, or supply planning.

- Payables swings that look reactive: If payables dropped because you rushed to pay vendors, explain the reason. If they rose because you delayed payments, be careful. That can look like stress.

- Misclassified one-time events: Gains from asset sales and similar items shouldn't muddy the operating section.

- No reconciliation narrative: A clean statement with no verbal explanation is weaker than most owners realize.

Your lender is reading for control. They want to see that you understand what moved cash and that you can manage it.

What to say when the lender asks questions

The best answers are short, specific, and operational.

Don't say, “Cash was just lower this quarter.”

Say something closer to this:

- On receivables: Collections lagged because a few larger invoices hit near period-end, and the aging is already improving.

- On inventory: We built stock ahead of committed demand to avoid production delays.

- On payables: We shortened payables intentionally to secure supply continuity with key vendors.

That kind of answer tells the lender you're not guessing. You know how cash moves through your business.

What Your Cash Flow Statement Tells a Lender

A lender doesn't read your cash flow statement to admire accounting technique. They read it to judge whether your business handles money with discipline.

The indirect method for statement of cash flows helps you prove that discipline. It shows whether profit turns into operating cash, whether working capital is helping or hurting liquidity, and whether the business is stable enough to support new debt.

Used well, this statement becomes more than a report. It becomes a credibility tool. It shows that you understand the gap between earnings and cash, that you can explain it, and that you can plan around it. That matters even more when paired with a forward-looking view, which is why a guide on how to build a cash flow forecast that empowers your loan strategy belongs in the same preparation process.

If you can walk a lender through your operating cash flow with confidence, you stop sounding like an applicant hoping for approval. You sound like a borrower who knows exactly how the business will repay the loan.

If you're preparing for financing and want a faster path to the right options, Business Loan Warrior helps small business owners check specific funding options through a no-fee application, compare structures that fit their cash flow, and move from paperwork to funding with real underwriting support.