You know the feeling. Revenue lands, the account balance looks healthy, and for a moment the business seems fine. Then payroll hits, a supplier invoice clears, a tax payment comes due, and suddenly you're asking a much harder question than “Are we profitable?”

You're asking whether the business can stay liquid long enough to keep moving.

That's where most owners outgrow the basic spreadsheet they started with. A real small business budget worksheet isn't just a list of expenses. It's the operating map for cash movement, timing, and decision-making. And if you want outside capital, it also becomes something else: evidence. Lenders don't fund optimism. They fund businesses that can show discipline, visibility, and a believable path to repayment.

Table of Contents

- Why Your Business Needs More Than a Basic Budget

- Gathering Your Financial Building Blocks

- Designing Your Funding-Ready Budget Worksheet

- Projecting Income and Forecasting Expenses Accurately

- Turning Your Budget into a Loan Application Tool

- How to Maintain Your Budget as a Living Document

- From Financial Clarity to Confident Growth

Why Your Business Needs More Than a Basic Budget

A basic budget usually starts as a control tool. Owners want to stop overspending, set targets, and keep the lights on. That's useful, but it's incomplete.

Problems arise when cash timing turns against you. A strong month on paper can still leave you squeezed if customers pay late, inventory has to be purchased upfront, or fixed costs keep hitting before receivables clear. That's why a worksheet has to do more than total income and expenses. It has to show when money moves, what costs are locked in, and what choices you have.

According to Smartsheet's small business budget guidance, 82% of U.S. businesses that fail do so because of poor cash flow management rather than lack of profitability, and experts recommend underestimating initial revenue forecasts by 25% to 30% to build a more resilient plan.

That recommendation matters because most owners are naturally optimistic about sales and overly casual about timing. They remember the big invoices they expect to send. They don't always model the lag between sending the invoice and having usable cash in the bank.

Practical rule: Profit can keep a business attractive. Cash keeps it alive.

A lender sees the same thing. If your worksheet only says, “sales up, expenses down,” it doesn't answer the underwriting question. Can this company absorb normal volatility and still make its obligations? A funding-ready budget worksheet answers that directly.

Why lenders care about the same worksheet

Internally, your budget helps you decide whether to hire, buy equipment, expand marketing, or delay a purchase.

Externally, that same document becomes proof that you understand:

- Cash timing rather than just accounting profit

- Cost behavior under changing sales conditions

- Operational discipline when actual results drift from plan

- Repayment capacity if new debt is added

A weak budget is like driving with a fuel gauge that only updates at the end of the month. A strong one shows what's in the tank, what the route demands, and whether you can handle a detour.

Gathering Your Financial Building Blocks

Before opening Excel or Google Sheets, pull the raw material. Most broken budgets don't fail in the formulas. They fail because the owner built them on memory, not records.

A workable starting point is the last stretch of your actual financial history. Best practice is to use data from the past 12–36 months of P&L and cash flow statements so your categories stay consistent and grounded in reality, as outlined in this budgeting and forecasting guide.

The documents worth gathering first

Start with the records that tell you how the business has behaved:

Profit and Loss statements

These show revenue, cost of goods sold, gross margin, and operating expenses over time. They help you spot patterns that memory hides, especially around seasonality and creeping overhead.Cash flow statements

These matter because profit and cash are not the same thing. A business can post a strong month and still feel pressure if collections are slow or vendor payments are front-loaded.Balance sheets

These help you see obligations, working capital pressure, debt levels, and whether assets and liabilities support the story your income statement is telling.Bank statements and credit card statements

These are the ground truth. They catch subscriptions, bank fees, software renewals, and one-off spending that often gets missed in rough budgets.Sales reports and invoice aging

These help forecast incoming cash, not just booked revenue. If customers usually pay on delay, your worksheet should reflect that timing.Payroll records, rent, insurance, loan schedules, and utility bills

These are the fixed-cost backbone of the business. If you don't capture them accurately, everything downstream gets distorted.

If you want a quick way to pressure-test whether those records are telling a healthy story, a financial health assessment for small businesses can help surface weak spots before you build projections on top of them.

The budget shouldn't start with hope. It should start with evidence.

What owners often miss

The most common omission isn't some advanced finance metric. It's consistency.

Expenses get labeled one way in bookkeeping, another way in a budget tab, and a third way when someone prepares loan paperwork. That creates friction fast. If “merchant processing,” “bank card fees,” and “payment fees” are really the same category, consolidate them. If “owner draw” is mixed in with payroll, separate it. Clean categories make the worksheet easier to manage and easier to defend.

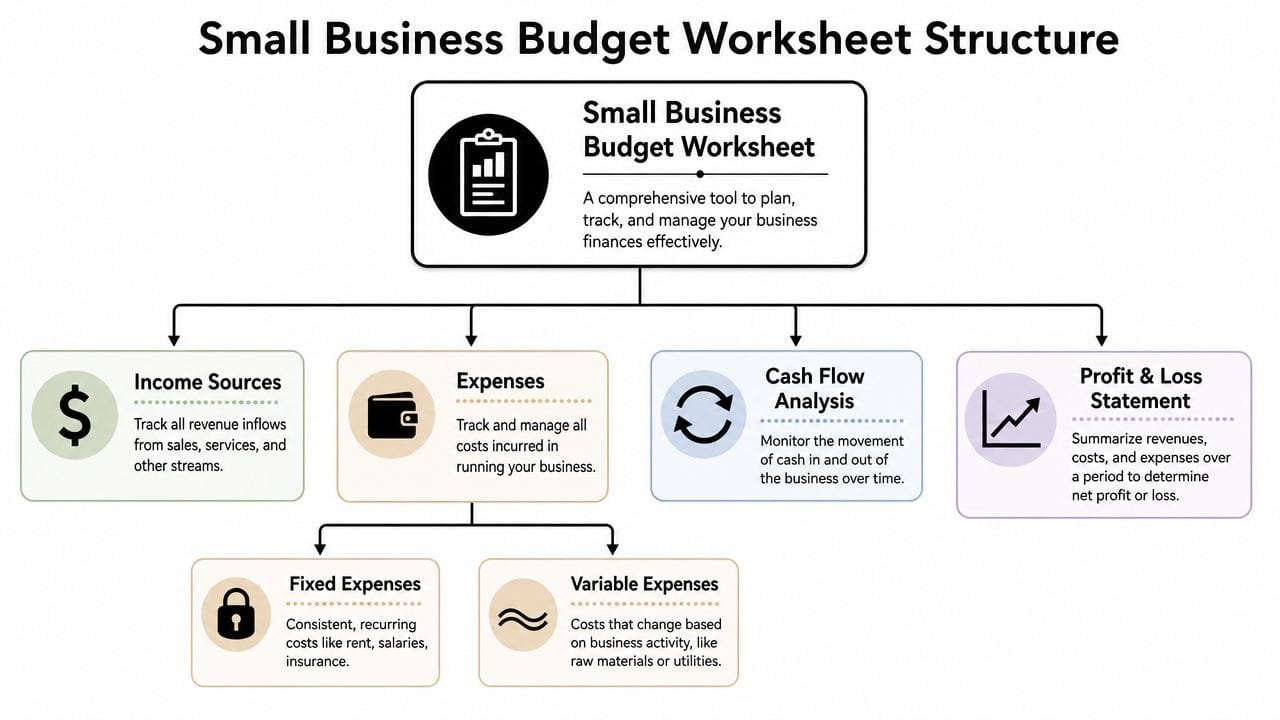

Designing Your Funding-Ready Budget Worksheet

A good small business budget worksheet should be easy to update, easy to audit, and hard to misunderstand. If it's so complex that only one person can interpret it, it won't help you manage the business, and it won't help a lender trust the numbers.

The shift to digital templates in Excel or Google Sheets matters because auto-calculation formulas reduce human error and make frequent updates practical, as noted in this overview of small business budget templates. That matters because a worksheet that isn't updated regularly becomes decoration.

Start with the structure, not the formulas

Build the worksheet in layers.

At the top, list income sources by type, not just one total revenue line. A company with retail sales, service income, maintenance contracts, and other income should show those separately. That gives you cleaner forecasting and a better explanation if one line changes sharply.

Under that, separate expenses into:

- COGS

- Fixed operating expenses

- Variable operating expenses

- Debt payments

- Taxes

- Capital expenditures if relevant to the planning period

One of the biggest technical mistakes in SMB budgeting is failing to separate fixed costs from variable costs. That distorts break-even analysis and makes the worksheet much less useful for real planning, as noted in the earlier budgeting guidance.

The minimum columns that matter

Most owners need fewer line items than they think and more columns than they expect.

Use these columns:

- Line item

- Annual budget

- Period budget

Monthly usually works well. Some businesses need weekly visibility. - Actual

- Variance

- Notes

- Cash timing

- Lender compliance notes

That last pair is what most templates skip.

Cash timing helps track when revenue is collected and when obligations are paid. Lender compliance notes give you space to flag items tied to underwriting questions, such as debt service, collateral-backed assets, lease obligations, or unusual one-time costs.

If a line item affects repayment capacity, don't bury it in a generic expense bucket.

Sample expense categorization

| Expense Category | Example | Why It Fits |

|---|---|---|

| Fixed Costs | Rent | Usually stays the same regardless of monthly sales volume |

| Fixed Costs | Salaries | Recurring payroll commitments don't usually move with each sale |

| Variable Costs | Shipping | Rises and falls with order volume |

| Variable Costs | Raw materials | Changes based on production or delivery activity |

| COGS | Product components | Directly tied to what you sell |

| Operating Expenses | Software subscriptions | Supports the business but isn't part of producing inventory |

| Debt Service | Loan payment | Needs to be visible because lenders will evaluate repayment ability |

| Taxes | Sales or income tax payments | Must be planned separately because timing can strain cash |

| Capital Spending | Equipment purchase | Not a routine operating expense and should not be mixed into normal overhead |

Keep the worksheet usable

Owners often overbuild these files. They add too many tabs, too many account codes, and too many small categories that don't change decisions.

A better worksheet groups accounts where it makes practical sense. If several small software tools behave like overhead, combine them. If multiple marketing channels are managed as one budget decision, roll them up. A budget is a management tool first. The accounting system can carry more detail than the worksheet needs.

For funding readiness, the worksheet should answer three questions quickly:

- Where does cash come from?

- What costs are unavoidable?

- What happens to liquidity if revenue arrives later than planned?

If your spreadsheet can answer those cleanly, you're much closer to something a lender can use.

Projecting Income and Forecasting Expenses Accurately

Forecasting is where many budgets subtly go off the rails. The worksheet looks polished, but the assumptions underneath it are soft.

The biggest problem is revenue modeling. Plenty of businesses no longer fit a simple pattern of steady monthly sales or early-stage guesswork. They operate with a hybrid income model, mixing recurring revenue with project-based work, one-time large invoices, milestone billing, or seasonal spikes.

Revenue needs timing, not just totals

Many templates still treat revenue as a smooth line. That's not how real businesses behave.

According to Business.com's discussion of small business budget templates, many templates fail to address this hybrid income reality, and a stronger worksheet should map cash flow timing so revenue spikes line up against large liability payments when proving liquidity to underwriters.

That means your worksheet should separate:

- Recurring contracted revenue

- Likely but not yet closed pipeline

- Project or milestone revenue

- Seasonal surges

- Low-probability upside

Don't stack all of that into one monthly sales estimate. Treat each stream based on how dependable it is and when cash lands.

For owners trying to sharpen those assumptions, it helps to study how small businesses use data to turn sales history, pipeline behavior, and operating patterns into better decisions. The point isn't fancy analytics. The point is replacing guesswork with a repeatable method.

A forecast earns trust when it shows restraint. It loses trust when every opportunity is treated like cash in hand.

Expense forecasting should follow business activity

Expense forecasting works best when it mirrors how the business runs.

Fixed costs usually stay stable enough to budget from contracts, payroll records, and recurring bills. Variable costs should move with volume. COGS should track the revenue stream that creates it. If materials rise only when production rises, forecast them in that relationship. If commissions pay after collection, reflect that lag.

A practical way to build expense assumptions is to ask:

- What costs happen even in a slow month?

- What costs rise only when sales rise?

- What costs show up before revenue is collected?

- What costs are one-time or irregular but still likely?

This is also where many owners forget equipment deposits, renewals, tax obligations, repairs, and expansion-related costs. Those items don't always appear every month, but they can reshape a quarter.

If you're building this with financing in mind, a dedicated cash flow forecast for loan strategy helps connect projections to borrowing needs and repayment timing.

A more credible way to forecast

A reliable worksheet usually combines three lenses:

Historical behavior

Use your records to show what the business has already done in strong and weak periods.Current operating reality

Adjust for known changes like pricing, staffing, supplier contracts, or customer churn.Collection and payment timing

Forecast when money moves, not just when it's earned or billed.

That's the difference between a budget that looks impressive and one that helps you make decisions.

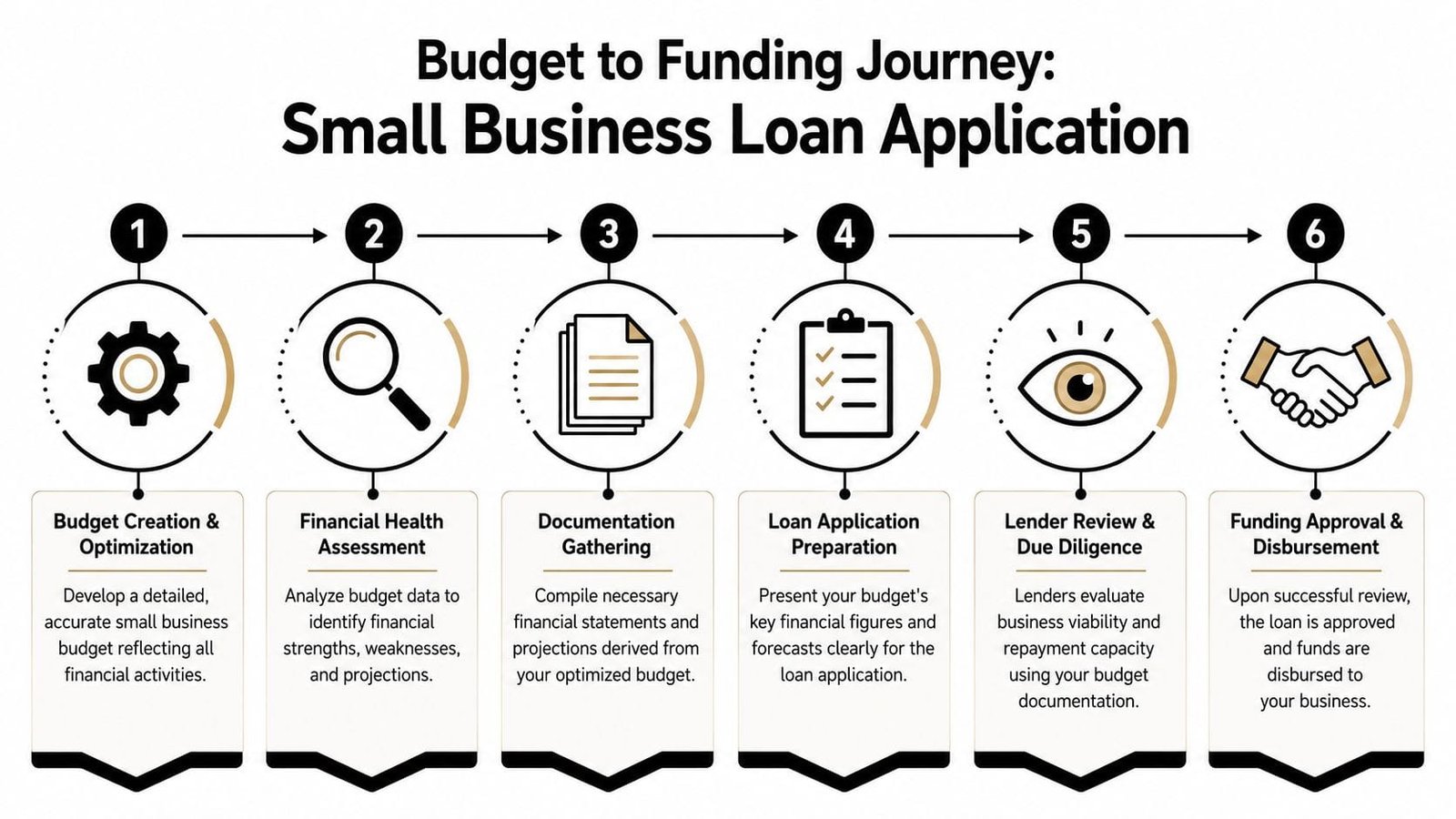

Turning Your Budget into a Loan Application Tool

Most owners think of the budget as an internal document. Lenders don't.

To an underwriter, your budget is part of the evidence package. It shows whether management understands the business, whether assumptions are grounded, and whether repayment looks realistic under normal pressure.

That's why the Budget-to-Funding Gap matters. Most budget guides focus on internal cash tracking but ignore how the document should be structured for underwriting. As explained in Gusto's discussion of budget templates, templates rarely include dedicated fields for debt service coverage ratios or collateral mapping, even though those are critical for owners seeking capital.

What underwriters want to see

Underwriters don't need a prettier spreadsheet. They need a clearer one.

They're usually looking for signs of:

- Consistent categorization across historical statements and projections

- Visible debt obligations rather than hidden blended expenses

- Reasonable revenue assumptions tied to real operating patterns

- Liquidity awareness when payments and collections don't line up

- Management control shown through planned-versus-actual tracking

- Collateral visibility if assets support the request

If your worksheet blends loan payments into overhead, hides owner distributions, or treats every sale as immediate cash, it creates more questions than confidence.

Add a lender view to the worksheet

A funding-ready worksheet should include a separate section, tab, or summary block that reframes the budget from a lender's perspective.

Include fields for:

- Beginning cash balance

- Cash from sales

- Expected collection timing

- Cash paid for expenses

- Expected payment timing

- Loan repayments

- Tax payments

- Ending cash balance

- Debt service coverage tracking

- Collateral notes for major assets

That approach aligns with structured budgeting methods that calculate ending cash by starting with beginning cash, adding collections, and subtracting expenses, loan repayments, and taxes.

Lenders don't assume your cash will behave nicely. Your worksheet should show that you don't assume that either.

A useful presentation format is a summary page that answers these practical questions:

- Can the business cover current obligations?

- What happens if receivables slow?

- Is debt service clearly visible?

- What assets or recurring income support the request?

- Are there large liabilities clustered in the same period as revenue dips?

What makes a budget convincing

Convincing doesn't mean aggressive. It means coherent.

A lender is more likely to trust a budget that:

- shows conservative treatment of uncertain revenue,

- separates operating costs from debt service,

- explains major assumptions in notes,

- and ties the borrowing purpose to a visible business need.

For example, if you're seeking equipment financing, your worksheet should show where that equipment affects revenue, cost structure, or production timing. If you're seeking working capital, the worksheet should show the operating gap the funds are meant to stabilize. If you're pursuing an SBA or expansion loan, the budget should make the use of proceeds and repayment logic easy to follow.

For owners preparing the broader package, a detailed guide to business loan applications helps frame the budget alongside the other documents lenders expect.

A budget becomes powerful in lending when it stops reading like bookkeeping and starts reading like management.

How to Maintain Your Budget as a Living Document

The businesses that get the most value from a small business budget worksheet aren't the ones that build the most elaborate file. They're the ones that revisit it often enough to catch problems while they're still small.

Experts recommend treating the budget as a recurring process with a review cadence of once to four times per month, which turns it into a dynamic decision tool built around planned-versus-actual variance, according to this reporting and budgeting resource.

Use variance as an early warning system

The variance column is where the worksheet starts doing real work.

If payroll runs higher than planned, ask whether it came from overtime, staffing changes, or scheduling inefficiency. If revenue misses plan, check whether the issue is demand, pricing, collections, or delayed project timing. If marketing overspends but drives stronger collections later, that's not automatically a problem. It may be a signal to reallocate.

What matters is speed. A variance noticed in the same month can usually be managed. The same variance discovered at quarter-end often becomes damage control.

If part of your monthly routine still involves extracting financial data from static reports, tools like online PDF to Excel conversion can make it easier to move statements into a working spreadsheet without retyping everything by hand.

Build a review rhythm you'll actually keep

Most owners don't need a finance committee meeting every week. They need a cadence they won't abandon.

A practical rhythm looks like this:

- After accounting close review actuals against plan

- Mid-period check cash position, receivables, and large upcoming payments

- Quarterly adjust assumptions for pricing, staffing, vendor costs, and financing needs

That's enough structure to keep the worksheet alive without turning it into a burden.

Here's a useful walkthrough if you want a visual reset on budgeting discipline:

What should trigger an update

Don't wait for the calendar alone. Update the worksheet when the business changes.

Common triggers include:

- A major new contract that changes staffing or purchasing needs

- A price increase from suppliers that affects margin

- New debt or lease commitments that change fixed cash obligations

- Expansion plans like equipment, space, or location investment

- Collection slowdowns that put pressure on working capital

Review cadence keeps the budget current. Variance analysis makes it useful.

A living document doesn't need to be perfect. It needs to be current enough to support the next decision.

From Financial Clarity to Confident Growth

A strong small business budget worksheet does more than organize numbers. It gives you control over timing, visibility into pressure points, and a way to make decisions before cash problems force them on you.

It also changes how you approach funding. Instead of walking into the process with scattered statements and rough estimates, you show up with a document that explains how the business earns, spends, collects, and repays. That's a very different posture. It signals that you're not chasing money to patch confusion. You're using capital to execute a plan.

If your current budget only tracks expenses, rebuild it. Separate fixed costs, variable costs, and COGS. Add planned-versus-actual columns. Add cash timing. Add a lender view. Then keep it current.

That's how owners move from “I think we can afford this” to “I know what this business can support.”

When you're ready to turn a well-built budget into real financing options, Business Loan Warrior can help you explore funding built around your business needs, from working capital to equipment, construction, SBA, and expansion loans.