You get the loan offer by email. The lender highlights one percentage in bold, the monthly payment looks manageable, and the funding timeline sounds fast. Then you reach the fee page and the numbers stop making intuitive sense.

That's where many strong business owners make an expensive mistake. They compare the headline rate, assume the cheapest-looking offer is the best one, and miss the way lenders package cost through fees, repayment frequency, prepayment terms, and product structure.

A small business loan percentage isn't always one thing. It might refer to an interest rate, an APR, an SBA guarantee percentage, or a factor rate on a product that doesn't behave like a standard loan at all. If you don't translate that percentage into actual dollars leaving your business, you're not evaluating financing. You're reacting to marketing.

This guide is built for that exact moment. The point is simple: take any offer in front of you and convert it into true borrowing cost, cash flow impact, and decision clarity.

Table of Contents

- What Does a Small Business Loan Percentage Really Mean

- APR vs Interest Rate The Two Numbers That Dictate Your True Cost

- Typical Loan Percentages by Funding Type in 2026

- From Percentages to Payments A Practical Calculation Guide

- The Five Factors That Shape Your Loan Offer

- How to Secure the Lowest Possible Loan Percentage

What Does a Small Business Loan Percentage Really Mean

When owners search for small business loan percentage, they usually want one answer. They don't get one because lenders use the word “percentage” to describe different parts of a financing offer.

Sometimes it means the interest rate. Sometimes it means APR, which includes interest plus certain fees. In SBA lending, some people even confuse the guarantee percentage with the borrower's cost. On revenue-based products, the lender may avoid APR language entirely and lead with a factor rate instead.

The same-looking number can describe different things

A term loan priced at one percentage and a merchant cash advance priced with another can't be compared at face value. They collect differently, behave differently, and hit cash flow differently.

That matters because the wrong comparison creates the wrong decision. A business owner may reject a healthy bank product because the rate looks higher, then accept a faster offer that drains more cash over the life of the deal.

Here's the cleaner way to read any offer:

- Identify the product type: Term loan, line of credit, SBA loan, equipment loan, invoice financing, or merchant cash advance.

- Identify the pricing language: Interest rate, APR, factor rate, flat fee, draw fee, service fee, or prepayment charge.

- Convert the offer into dollars: Total borrowed, total paid back, payment frequency, and the timing of each payment.

- Judge cash flow, not just price: A cheaper annualized cost can still be stressful if the payment structure is too aggressive for your business cycle.

A percentage is only useful when you know what balance it applies to, what fees sit around it, and how fast the lender collects.

The decision standard that actually works

In practice, I look at financing through three filters:

| Question | Why it matters |

|---|---|

| How much cash do you receive at closing? | Fees can reduce usable capital on day one. |

| How much cash leaves the business in total? | This reveals true borrowing cost. |

| How often does the lender get paid? | Repayment timing shapes operational pressure. |

If you use those three filters consistently, most loan offers become much easier to judge. The language gets less intimidating because you stop treating percentages as abstract finance jargon and start treating them as cash flow instructions.

APR vs Interest Rate The Two Numbers That Dictate Your True Cost

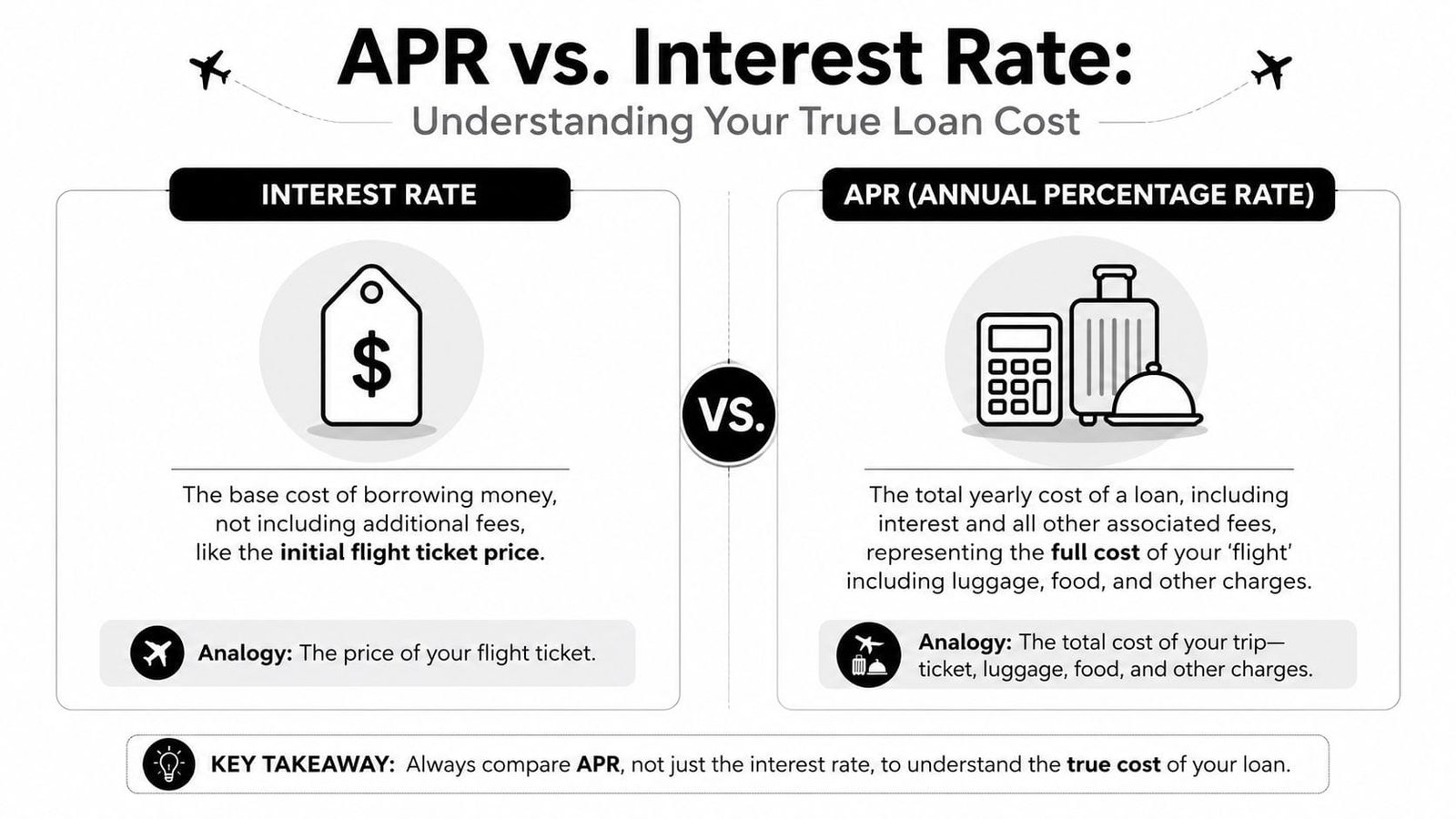

The interest rate is the sticker price. APR is the drive-off cost.

That distinction is where most financing analysis either becomes disciplined or falls apart. A lender can promote an appealing interest rate while layering in origination charges, underwriting costs, servicing fees, or prepayment terms that raise the actual cost of capital.

Interest rate tells you only part of the story

The interest rate is the base charge for using the lender's money. It does not always capture the full cost of getting that money into your account and keeping the facility active.

APR is meant to reflect a broader view. It pulls in interest and certain borrowing costs so you can compare one offer against another more accurately. If you want a practical benchmark for what business borrowing can look like in the market, review current business loan interest rates today and then compare those numbers against the fee structure on your actual offer.

Fees are where lenders reshape economics

A few charges matter more than owners think:

- Origination fee: Taken upfront or financed into the loan, reducing net proceeds or increasing financed balance.

- Underwriting or processing fee: Common on some products, especially faster-moving nonbank offers.

- Annual or service fee: Can raise the all-in cost even when the note rate looks reasonable.

- Prepayment penalty: Limits your ability to refinance or exit early without additional expense.

Practical rule: Always compare loans using APR, not the interest rate.

That's especially important in the SBA market, where many articles confuse guarantee language with borrower pricing. The SBA notes that guarantee percentages such as 85% for loans of $150,000 or less, lender risk retention of 15% to 25%, prepayment fees, annual service fees, and variable rate caps such as base + 6.0% for $50,001 to $250,000 loans all affect the economics borrowers experience, even though many summaries don't present the full cost picture upfront through the same lens (SBA 7(a) terms and conditions).

The simplest way to evaluate an offer

When I review a loan summary, I don't ask “What rate did they quote?” first. I ask:

- What are the net proceeds?

- What is the total repayment amount?

- What are the fees at closing and during the loan?

- What happens if the business repays early?

That approach immediately exposes weak offers. Some loans look inexpensive until you notice that a chunk of the approved amount never reaches your operating account because fees are deducted before funding. Others look flexible until the prepayment language effectively traps you.

A quick test you can use today

If a lender won't clearly disclose the following in plain language, slow down:

| Item to confirm | What you need |

|---|---|

| Rate format | Interest rate, APR, or factor rate |

| Fees | Upfront, ongoing, and exit-related |

| Repayment timing | Daily, weekly, or monthly |

| Net funding | Amount received after deductions |

The best financing offers survive scrutiny. The weaker ones depend on haste.

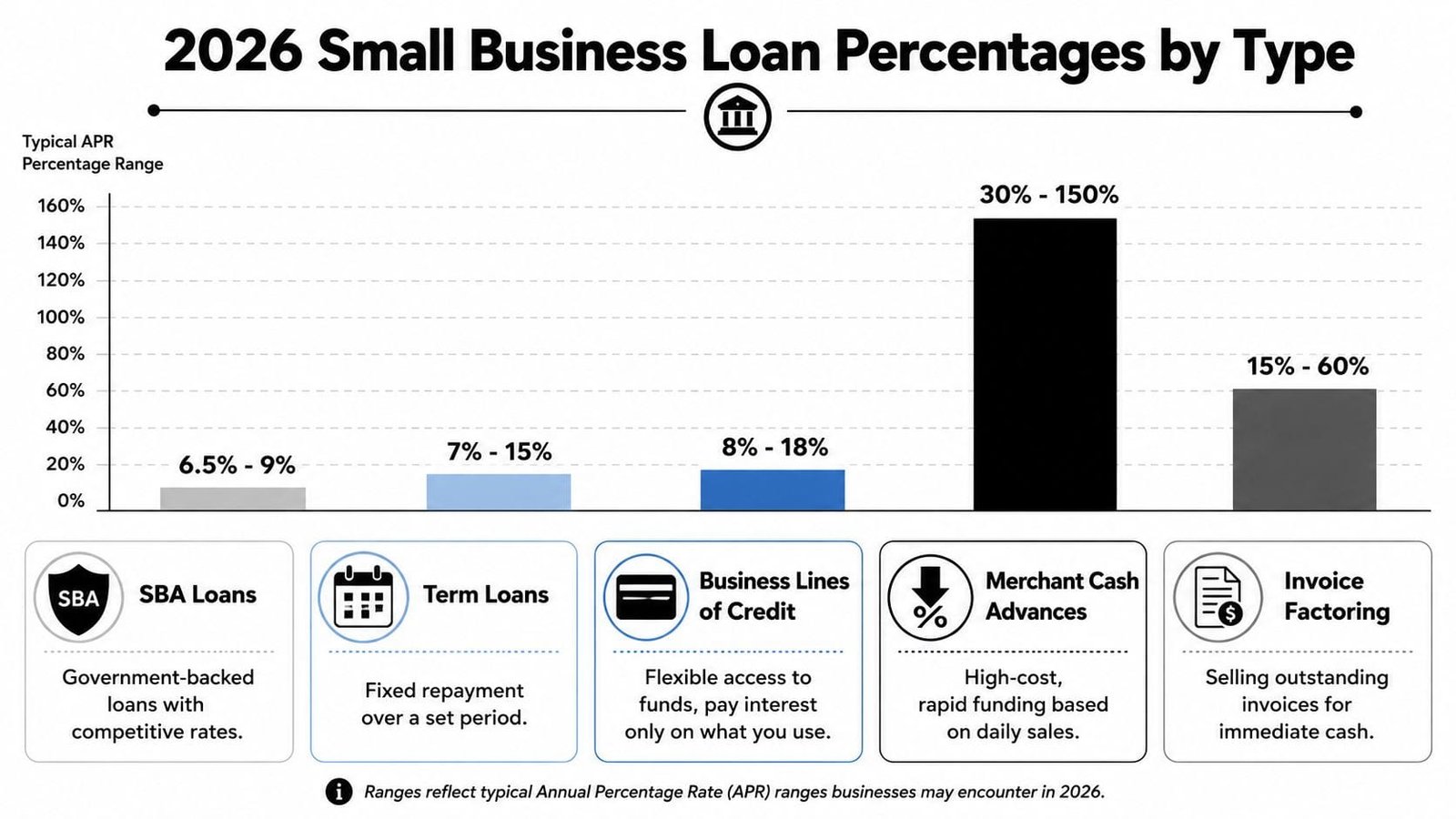

Typical Loan Percentages by Funding Type in 2026

Loan pricing varies more by product design than most owners expect. That's why “small business loan percentage” is a slippery search term. It captures several financing categories that solve different problems and price risk in different ways.

For 2026 planning, the better approach is to look at each funding type through three lenses: how the money is used, how it's repaid, and how the pricing should be interpreted.

A practical market reference

| Funding type | How owners usually use it | Repayment pattern | Pricing lens to use |

|---|---|---|---|

| SBA loan | Expansion, acquisitions, equipment, working capital | Usually structured and longer-term | Look at rate plus fees and the total cost of capital |

| Traditional term loan | Growth projects, inventory, hiring, refinancing | Fixed scheduled payments | Compare on APR and total repayment |

| Business line of credit | Short-term working capital swings | Revolving, based on draws | Focus on draw costs, fees, and usage pattern |

| Equipment financing | Machinery, vehicles, production assets | Amortized against the asset | Asset support can improve structure |

| Invoice financing | Accelerating receivables | Tied to invoices collected | Understand fee cadence and timing |

| Merchant cash advance | Fast cash for urgent needs | Frequent remittances from sales | Don't compare factor rate to APR directly |

The infographic above includes common market-style ranges for these categories, but use them as directional context rather than a substitute for underwriting. Your actual offer will move based on lender appetite, documentation quality, and the way your cash flow looks on paper.

SBA loans often offer meaningful capital, but preparation matters

SBA financing remains one of the most important categories to evaluate carefully because it often supports larger strategic uses of capital. In 2023, approximately 59% of SBA loans were approved, with 34% fully approved and 25% partially approved, and the average SBA loan amount was $479,685 according to Lendio's small business lending statistics. That tells you two things. Businesses do get through the process, and the capital can be substantial when they do.

The trade-off is complexity. SBA offers often look more borrower-friendly than nonbank alternatives, but owners still need to examine fees, guarantee-related economics, and variable-rate structure rather than assuming “SBA” automatically means “cheap.”

Why the product category matters more than the headline number

An equipment loan and a line of credit can both support growth, but they are not interchangeable. Equipment financing usually sits against a tangible asset, so the lender has a clearer recovery path if the loan fails. A line of credit is more operational. It supports working capital and fluctuates with use, so the pricing logic is different.

Merchant cash advances deserve special caution. The factor rate format can look simpler than a loan rate because it appears to promise a fixed payback amount. Simpler does not mean cheaper. It often means the lender has shifted the discussion away from annualized cost and toward speed and convenience.

Matching the financing to the operating problem

The best financing decisions start with the business problem, not the advertised percentage.

- Long-lived asset purchase: Equipment financing or SBA often fits better than a short-duration product.

- Temporary working capital gap: A line of credit may be more appropriate than a fixed lump-sum term loan.

- Receivables-heavy operation: Invoice-based funding can align better with collection cycles.

- Emergency liquidity need: Fast products may solve the timing issue, but you need to price the urgency realistically.

Some finance teams also review broader treasury options alongside debt strategy, especially if they operate internationally or explore digital payment infrastructure. For owners evaluating modern cash-management tools, this resource on criptomonedas para empresas offers useful context on how businesses think about financial operations beyond traditional banking alone.

The right product is the one that fits the purpose, protects cash flow, and still looks acceptable after you calculate total repayment.

From Percentages to Payments A Practical Calculation Guide

A loan doesn't hurt your business because of a label. It hurts your business when the payment structure takes more cash than your operating cycle can support.

That's why I reduce every offer to a short worksheet. I want to know the net amount received, the total amount repaid, and how quickly the lender collects it. If you want a deeper walkthrough of the mechanics, this guide on how to calculate the real cost of a small business loan without the headache is a useful companion.

Example one with a standard term loan

Assume you borrow $100,000 on a term loan priced at 9% APR.

Start with three questions:

- How much do you receive?

If fees are deducted at closing, your usable cash may be less than the face amount. - What is the monthly payment?

That depends on the loan term and amortization schedule. - What is the total repayment?

Multiply the scheduled payment by the number of payments, then add any fees not already included.

For a standard amortizing loan, the monthly payment contains both principal and interest. Early payments lean more heavily toward interest, and later payments shift toward principal. That means the cost of borrowing isn't just the APR. It's also the length of time you carry the balance.

Example two with a merchant cash advance

Now assume the same $100,000 funding amount comes through a merchant cash advance with a 1.3 factor rate.

The easiest part of this calculation is the total payback:

- Advance amount: $100,000

- Factor rate: 1.3

- Total repayment: $130,000

That looks straightforward, but it hides the key issue. A factor rate does not adjust for time the way APR does. If the lender collects that $130,000 quickly through daily or weekly remittances, the effective annual cost can become dramatically more expensive than many owners realize.

A factor rate tells you how much you'll repay. It doesn't tell you how expensive the money is on an annual basis.

The comparison method that works in real life

Use this side-by-side checklist:

| Calculation step | Term loan | Merchant cash advance |

|---|---|---|

| Amount funded | Start with face amount | Start with advance amount |

| Fees deducted upfront | Subtract from proceeds | Subtract from proceeds if applicable |

| Total repayment | Add scheduled payments and fees | Multiply advance by factor rate |

| Payment frequency | Usually periodic installments | Often frequent remittances |

| Best comparison tool | APR and amortization | Total payback plus estimated annualized cost |

The back-of-the-envelope test

Before accepting any offer, write down these four lines on paper:

- Cash received at funding

- Total dollars repaid

- Payment frequency

- Earliest no-penalty payoff option

If the lender resists giving you those answers clearly, assume the structure benefits from confusion. Strong offers don't require mystery to look attractive.

The Five Factors That Shape Your Loan Offer

Lenders don't arrive at a percentage by instinct. They build it from risk signals. If you understand those signals, you stop being surprised by pricing and start preparing for it.

Credit quality drives pricing first

A lender starts with credit because it gives a fast read on repayment history and financial discipline. For closely held businesses, the owner's personal credit often matters alongside the business file.

Credit doesn't act alone, but it does shape the conversation quickly. Strong files usually get broader product access, cleaner terms, and more room to negotiate. Weaker files often get pushed toward shorter-duration or higher-friction structures.

Time in business and revenue affect lender confidence

A seasoned company with stable revenue gives an underwriter more to analyze. That doesn't guarantee approval, but it makes the file easier to defend.

Young companies can still get funded, especially when bank statements, margins, and deposits tell a consistent story. The challenge is that many lenders price uncertainty aggressively. If the business can't show durability yet, the lender often protects itself through cost or structure.

Industry risk and collateral change the structure

Some sectors produce steadier cash flow than others. A lender sees that clearly, even if the owner focuses on recent performance. Businesses with volatile margins, seasonal swings, or operational fragility may face tighter terms because the repayment path looks less predictable.

Collateral can offset some of that concern. A lender behaves differently when the financing is attached to equipment, vehicles, or other identifiable assets. Asset support doesn't make a weak file strong, but it can improve how the offer is built.

This short video gives a useful lens on how lenders and borrowers think about financing decisions in practice.

Where you apply changes the outcome

Many owners assume underwriting is mostly about their business profile. It isn't. Lender type matters. In 2024, small banks achieved a 52% full approval rate, while large banks were at 44% and online lenders were at 31%, according to Credit Suite's lending statistics summary. That gap reflects something practical. Smaller institutions often rely more on relationship-driven judgment, while larger and digital-first channels may lean harder on rigid filters.

The same principle applies to product fit. A business with strong assets but uneven recent cash flow may receive a more workable structure from one lender category than another. Owners who only apply in one channel often mistake one lender's appetite for the entire market.

A lender's view of your file

When I review a borrower profile before financing discussions, I ask:

- Does the business generate reliable cash flow?

- Can the lender verify that quickly through statements and returns?

- Is there collateral or another risk offset?

- Does the industry create unusual volatility?

- Is this being shown to the right lender type?

The cheapest capital usually goes to the business that looks easiest to understand, easiest to verify, and easiest to repay.

That's why preparation matters as much as raw business quality. Two owners can run companies with similar economics and receive very different offers because one presents a clean, lender-ready file and the other submits a confusing package.

How to Secure the Lowest Possible Loan Percentage

The lowest possible small business loan percentage usually goes to the owner who prepares before applying, not the one who negotiates hardest at the end.

Start by tightening the basics. Clean up personal and business credit where possible, organize recent financial statements, and know your cash flow story cold. If revenue is seasonal or margin has shifted, explain it before the lender asks. Underwriters get nervous when they see surprises they have to interpret on their own.

Next, match the loan to the purpose. Don't use a short, aggressive product for a long-term growth investment if a better-structured option exists. If you already carry debt, evaluate whether refinancing could improve payment pressure and total cost. This overview of SBA loan refinancing and how to lower existing small business debt payments is worth reviewing when older debt is constraining current growth.

Then do the step many owners skip. Compare multiple offers. Not one. Multiple.

A lender competes differently when they know you're evaluating real alternatives. That pressure can improve rate, fee treatment, repayment flexibility, or all three. Even when the final pricing doesn't move much, the comparison process often exposes which offer is cleaner, which one hides cost in structure, and which lender is easiest to work with after funding.

Don't accept the first percentage you see. Accept the offer that still looks right after you translate it into net proceeds, total repayment, payment timing, and exit flexibility.

If you want to compare financing options without turning your office into a underwriting lab, Business Loan Warrior gives you a practical way to do it. You can check where you stand, review personalized offers, and compare terms side by side so you're not judging a loan by the headline percentage alone.