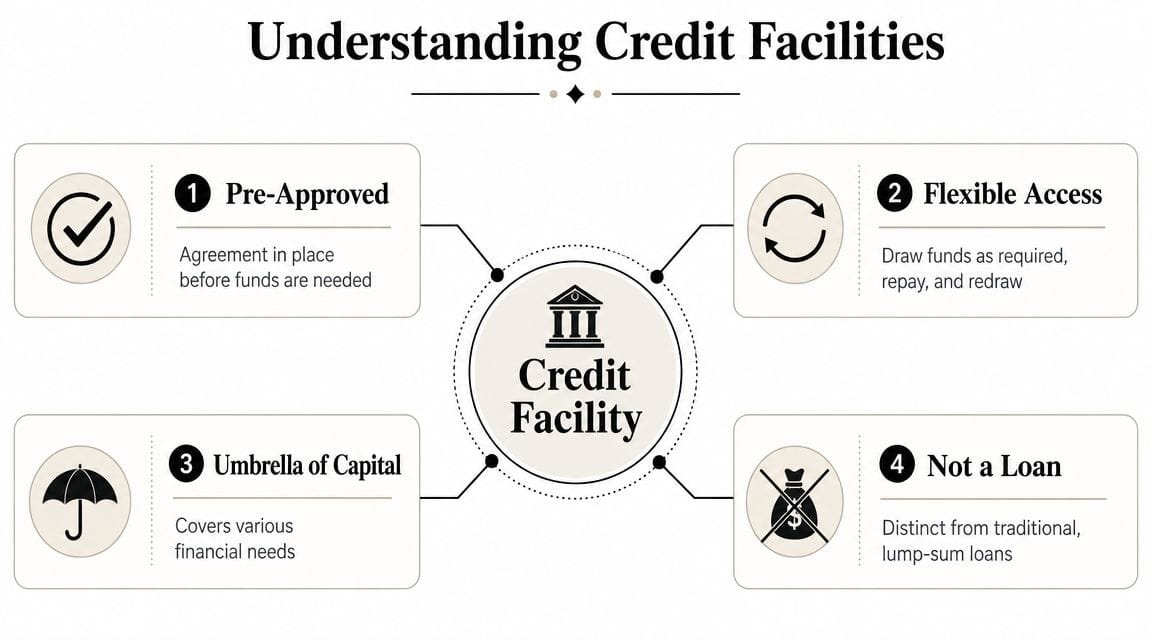

A credit facility is a pre-approved financing arrangement that lets your business draw funds repeatedly up to a fixed limit instead of reapplying every time you need cash, and interest and fees are usually tied to what you draw while the unused portion may still carry maintenance or commitment fees. Think of it as a funding reservoir you can tap when needed, rather than a one-time bucket of cash dumped into your account like a traditional loan.

If you're running a growing business, this probably feels familiar. Payroll lands on Friday, a big customer pays late, a supplier offers better pricing if you buy now, and suddenly the issue isn't whether your company is healthy. It's whether cash is arriving at the right time.

That's where many owners get tripped up. They ask for a loan when what they really need is flexibility. A loan can be perfect for one major purchase. But when your needs rise and fall, a credit facility often works better because the arrangement is already in place before the pressure hits.

For a busy owner, the primary value isn't just access to money. It's speed, control, and the ability to make decisions without reopening the financing conversation every few weeks.

Table of Contents

- Your Business Needs More Than Just a Loan

- What a Credit Facility Is in Plain English

- Exploring the Main Types of Credit Facilities

- Credit Facility vs Loan vs Line of Credit

- How Smart Businesses Use Credit Facilities

- Applying for a Credit Facility Key Terms and Costs

- Your Pre-Application Checklist for Success

Your Business Needs More Than Just a Loan

A business owner lands a new contract. Good news. Then the practical questions hit.

Can you buy materials before the customer pays? Can you staff the job without draining operating cash? Can you cover the gap without slowing down everything else in the business?

A traditional loan can help if the need is clear, fixed, and one-time. But many healthy companies don't operate in neat straight lines. They move through uneven billing cycles, seasonal demand, delayed collections, and surprise opportunities. That's why the better question often isn't, "Can I get money?" It's, "What funding structure fits the way my business moves?"

A credit facility fits that reality better because it gives you room to draw when needed, repay, and stay ready for the next bump or opportunity. It acts less like emergency money and more like a financial operating tool.

Practical rule: If your cash need changes month to month, a rigid one-time loan may solve the first problem and create the second.

That distinction matters most for owners who are already growing. Growth usually creates stress before it creates comfort. More sales can mean larger inventory orders, more labor, and longer receivable cycles. Without flexible access to capital, success can tighten cash instead of freeing it.

If you're building a broader funding strategy, it's worth seeing how flexible capital fits alongside other options in a smart small business financing strategy that goes beyond a single loan.

What owners usually confuse

Many people hear "credit facility" and assume it's just a fancy bank term for a loan. It isn't.

A loan is usually one event. A credit facility is an arrangement. That difference changes how you plan, how you borrow, and how quickly you can respond when business conditions shift.

What a Credit Facility Is in Plain English

A credit facility is a pre-approved borrowing arrangement your business can tap under rules set in advance.

The easiest way to understand it is to separate the approval from the use of the money. With a standard loan, approval and funding often happen as one event. With a credit facility, the lender first sets a limit, terms, and conditions. Your business then draws funds only when there is a real need, up to that limit.

Cornell Law School describes it as a pre-approved financing arrangement that lets a business draw repeatedly up to a fixed limit, with interest and fees tied to what is drawn and possible commitment fees on the unused portion.

A credit facility gives you access to capital before the pressure shows up.

That distinction matters more than it sounds. If a supplier offers a discount for buying early, or a large customer pays 45 days later than expected, you are not starting from zero and hoping a lender moves fast enough. You already have an agreed framework in place.

What the agreement controls

The facility is the agreement itself. It lays out how much is available, when you can borrow, what it costs, and what your business has to maintain to keep access open.

In plain terms, it usually covers:

- Your borrowing limit. The maximum amount available under the facility.

- How draws happen. The process for pulling funds when needed.

- What you pay. Interest usually applies to what you use, and some facilities also charge fees on the unused portion.

- How long access lasts. The agreement sets the term, review schedule, and renewal rules.

- What the lender expects from you. This can include reporting, financial benchmarks, or collateral requirements.

For a small business owner, the practical question is simple. What problem is this facility meant to solve? If the pressure comes from waiting on customer payments, a tool tied to invoices may fit better than a broader facility. In that case, it helps to understand how accounts receivable financing works for cash flow gaps caused by slow-paying customers.

Why owners care once cash flow gets tight

A credit facility helps with timing.

That may sound basic, but timing is where many growing businesses feel strain. Revenue can look strong on paper while cash is stuck in inventory, payroll, receivables, or deposits for upcoming work. A facility gives you a way to cover that gap without applying for brand-new financing every time the business speeds up or gets unpredictable.

So in plain English, a credit facility is not just borrowed money. It is a standing source of funding your business can use with intention. That makes it less of a one-time transaction and more of a tool for managing growth, uneven cash flow, and short-notice opportunities.

Exploring the Main Types of Credit Facilities

The main types of credit facilities differ in one practical way. They answer different cash flow problems.

If your business needs a cushion for uneven weeks, one structure fits better. If you are planning a larger project with a clearer price tag, another usually makes more sense. The goal is not to memorize labels. The goal is to match the tool to the job so the funding helps growth instead of adding friction.

Revolving facilities

A revolving facility gives you access to funds up to a set limit, then lets you repay and borrow again during the term of the agreement.

It works like a fuel tank you can refill. You use some capacity, replace it, and use it again as business activity changes. That makes it useful for companies with moving targets rather than one fixed expense.

A seasonal wholesaler is a good example. Inventory orders rise before sales arrive. Payroll and shipping have to be paid first. A revolving facility helps cover that gap without forcing the owner to apply for a new loan every time the cycle repeats.

This type often fits:

- seasonal inventory purchases

- payroll before customer payments clear

- short-term working capital swings

- unexpected opportunities, such as discounted bulk stock

Term facilities

A term facility is built for a more defined borrowing need. The lender approves the arrangement, the business uses the funds for a planned purpose, and repayment follows an agreed schedule.

This is usually the better fit when the amount is larger and the use is easier to map out. Opening a second location, buying a major piece of equipment, or funding a structured expansion are common examples.

Some business owners get tripped up here because "credit facility" sounds like it must always mean flexible, draw-as-needed borrowing. It does not. A term facility still sits under the broader credit facility umbrella. The difference is that the borrowing behaves more like a planned capital tool than an ongoing cash flow buffer.

Some agreements combine both. A business might keep a revolving portion for day-to-day liquidity and a term portion for a specific growth investment.

Strong financing plans match each dollar to its job.

Committed and uncommitted facilities

This distinction matters more than the names suggest.

A committed facility means the lender has agreed to make funds available under the contract, as long as you continue meeting the stated conditions. That gives you more certainty for planning payroll, inventory, or recurring operating needs.

An uncommitted facility gives the lender more discretion over whether to approve each advance. That can still be useful, but it is less dependable if you are counting on the money to keep operations moving.

For a small business owner, the question is simple. Are you arranging backup capital for convenience, or are you relying on it as part of your cash flow plan? If customer invoices are the bottleneck, a broader facility may not be the cleanest answer. It may help to compare it with accounts receivable financing for slow-paying customer invoices.

The broader point is this. "Credit facility" is a category, not one single product. Once you see the main types clearly, you can judge them by what matters most in real life: flexibility, certainty, cost, and how well they support growth when cash timing gets messy.

Credit Facility vs Loan vs Line of Credit

The confusion usually comes from overlap. A line of credit can be a type of credit facility. A term loan can sit beside one. And in casual conversation, people use all three terms as if they mean the same thing.

They don't.

Funding options at a glance

| Feature | Credit Facility | Term Loan | Business Line of Credit (LOC) |

|---|---|---|---|

| Structure | A pre-approved financing arrangement that may include different borrowing components under one agreement | A one-time lump-sum borrowing | Usually a revolving borrowing tool with a set limit |

| Best use | Ongoing liquidity planning, variable working capital, or combining short-term and planned borrowing needs | A single major purchase or project with a defined budget | Short-term operating needs and recurring cash flow gaps |

| Access to funds | Draws depend on the facility terms already negotiated with the lender | Funds are usually advanced once | Draw as needed up to the limit |

| Repayment style | Varies by facility type | Fixed repayment schedule is common | Flexible repayment, then redraw if available |

| Cost pattern | Costs may include interest on drawn funds plus fees on unused commitments | Interest applies to the funded amount | Interest usually applies to what is drawn; other fees may apply |

| Planning value | High, because the arrangement is in place before money is needed | Good for a known need | High for short-term liquidity management |

| Typical mindset | Strategic liquidity tool | Project financing tool | Operating cushion |

How to choose the right structure

If your need has a beginning, middle, and end, a term loan is often the cleanest fit. Buy equipment. Open a location. Refinance a specific obligation. That's a loan conversation.

If your need keeps changing, you usually want reusable access. That's where a line of credit or broader credit facility makes more sense.

The important nuance is that a credit facility is often the larger umbrella concept. A business line of credit is one common form of it. Some facilities are simple. Others are built to cover several needs at once.

Here's a useful way to decide:

- Choose a term loan when the spending plan is specific and mostly one-time.

- Choose a line of credit when timing gaps are the problem.

- Choose a broader credit facility when your business needs a financing framework, not just a single product.

A lot of owners only compare monthly payments. That's too narrow. You should also compare readiness, redraw flexibility, fees on unused capacity, and how each option fits the way your receivables and payables move. If you're weighing revolving access against lump-sum financing, this guide on when to choose a line of credit over a loan can help sharpen the decision.

How Smart Businesses Use Credit Facilities

The best use of a credit facility isn't dramatic. It's disciplined. Strong operators use it to keep momentum when timing gets messy.

Managing inventory before revenue arrives

A manufacturer sees demand building ahead of its busy period. Suppliers want payment early. Customers won't pay until product ships and invoices clear.

A revolving facility helps the owner buy raw materials at the right moment instead of waiting for cash to catch up. That protects purchasing power and keeps production moving. The facility isn't replacing profit. It's smoothing timing.

Bridging payroll and receivables

A service firm lands bigger clients. Good development, but larger customers often pay on slower cycles. Payroll doesn't wait.

In that scenario, the facility becomes a bridge. The owner draws enough to cover wages and project costs, then repays when receivables land. Used this way, the facility supports growth without forcing the company to keep excessive idle cash on the balance sheet.

Owner mindset: Use flexible credit to bridge timing gaps, not to hide a broken business model.

Funding a strategic move without stalling operations

A growing company wants to acquire a smaller competitor, add a product line, or invest in a meaningful expansion. The move requires planned capital, but the business still needs day-to-day liquidity.

A broader facility is especially effective in these situations. One part of the arrangement may support the strategic transaction while another preserves working capital flexibility. Instead of draining every available dollar for growth, the company keeps room to operate.

What separates good use from bad use

Smart use usually has three traits:

- Short purpose windows. The business knows why it's drawing and what event should repay the balance.

- Operational visibility. Management can tie borrowing to receivables, inventory turns, or a defined project.

- Restraint. Owners don't treat available credit as free cash.

Poor use looks different. The balance stays high, there isn't a clear repayment path, and the facility starts covering chronic losses or loose spending. A credit facility is powerful, but it works best as a tool for control, not avoidance.

Applying for a Credit Facility Key Terms and Costs

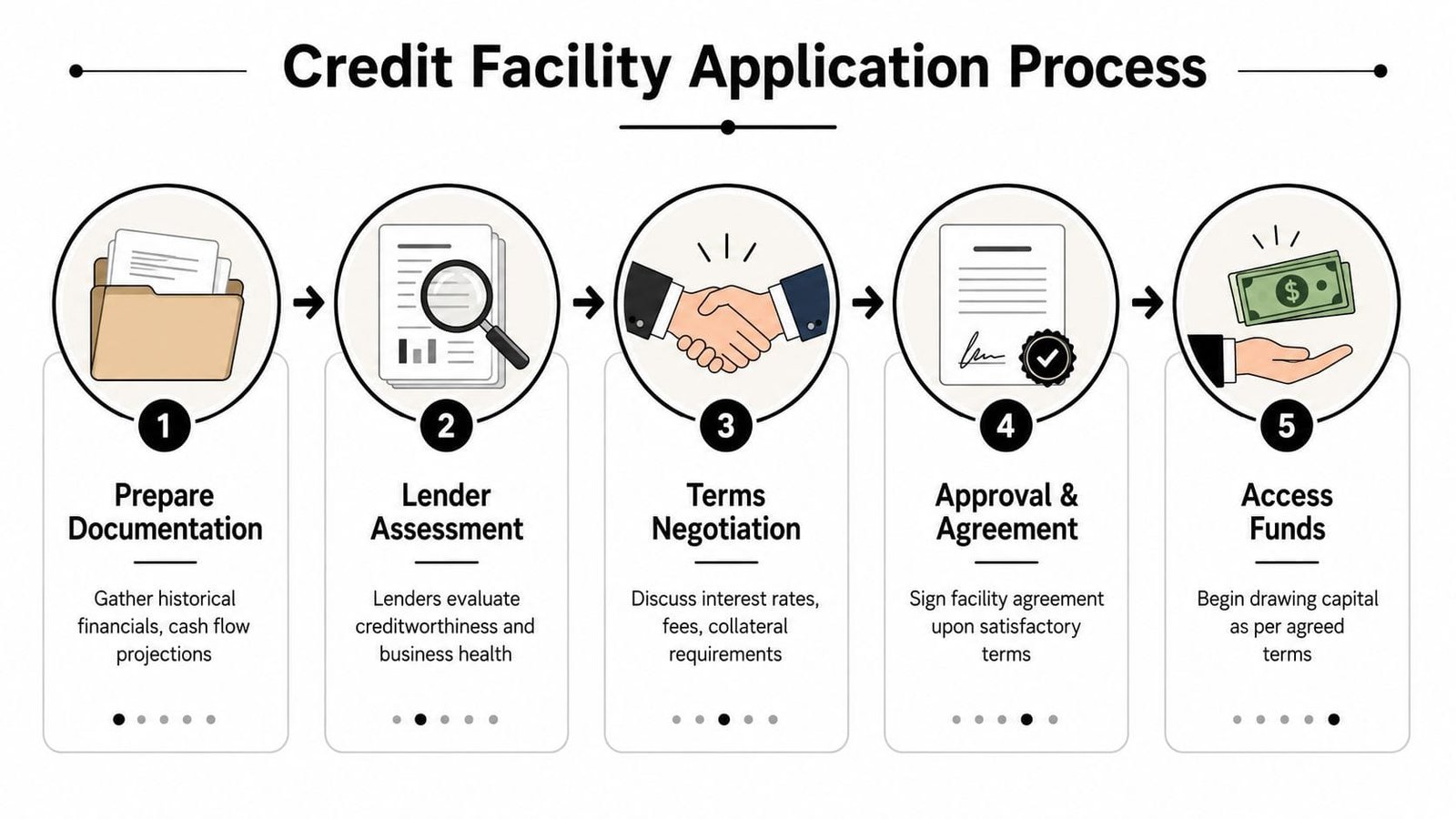

Before a lender approves a facility, they're trying to answer a simple question: if they give your business flexible access to capital, will you use it responsibly and repay it reliably?

What lenders review before approval

Expect the lender to look closely at your financial picture, not just your top-line story.

You'll usually need things like:

- Historical financials. Profit and loss statements, balance sheets, and cash flow records help show whether the business is stable.

- Current business performance. Recent statements show whether trends are holding up.

- Cash flow projections. Lenders want to see how borrowed funds fit into expected inflows and outflows.

- Ownership and business details. Formation documents, operating information, and sometimes background on principals are part of the file.

Your credit profile also matters more than many owners expect. Debt.org explains that lenders rely on standardized credit factors, and FICO's model gives the biggest weight to payment history at 35% and amounts owed at 30%, with the other factors being length of credit history at 15%, new credit at 10%, and credit mix at 10% in this breakdown of the credit factors lenders commonly evaluate.

That matters because discipline with existing obligations affects your next approval. If you've been maxing out available credit or paying late, lenders won't see flexibility. They'll see risk.

Costs and terms that deserve a second look

The obvious cost is interest on drawn funds. But with a credit facility, that's rarely the whole story.

Watch for these terms:

- Commitment or maintenance fees. Some facilities charge for keeping unused capacity available.

- Covenants. These are promises you make in the agreement, often tied to financial condition or reporting.

- Collateral requirements. Some facilities may be secured by business assets or other support.

- Reporting duties. You may need to provide periodic financial statements, borrowing base information, or compliance certificates.

A covenant sounds intimidating, but usually it means this: "Keep the business within the financial guardrails we agreed to, and keep us informed." The actual risk isn't the word. It's signing an agreement without understanding what could trigger a problem.

Before you negotiate price, understand the rules for access, reporting, and renewal. Those terms shape how usable the facility really is.

Your Pre-Application Checklist for Success

Walking into a lender meeting unprepared usually costs you twice. First in time, then in bargaining power. The better your package, the easier it is to get a facility that fits the business.

Get your house in order

Start with your records.

- Clean up bookkeeping. If your financials are messy, lenders assume operations may be messy too.

- Gather core documents. Have recent financial statements, business details, and cash flow information ready before anyone asks.

- Review existing debt. Know what obligations are already in place and how they affect your flexibility.

Know what you want before the lender asks

Many owners ask for "working capital" when they should be much more specific.

Write down:

- Why you need the facility. Inventory timing, receivable gaps, project bridging, acquisition support, or something else.

- How you expect to use it. Occasionally, regularly, or as a backup.

- How repayment should happen. From receivables, seasonal sales, recurring cash flow, or a planned event.

That clarity helps a lender match structure to need. It also keeps you from overborrowing just because a larger limit is available.

Walk in with better questions

Good borrowers don't just answer questions. They ask sharp ones.

Use this list:

- Ask how unused capacity is priced. You need to understand fees on money you haven't drawn.

- Ask what triggers a default or review. Covenants and reporting rules matter as much as the rate.

- Ask how renewal works. A facility that disappears at the wrong time can create stress.

- Ask what flexibility exists for growth. If your business scales quickly, can the structure grow with it?

A credit facility works best when you treat it like part of your operating system, not a rescue button. Preparation is what turns it from expensive convenience into strategic flexibility.

If you're exploring a credit facility and want a practical next step, Business Loan Warrior helps small business owners compare funding options through one no-fee application. You can check pre-approval, review customized financing paths, and find a structure that fits working capital, growth, or both without turning the process into another full-time job.