You're probably here because you're applying for funding right now, or you're about to. Maybe it's a line of credit for working capital, equipment financing before a busy season, or an SBA loan to support expansion. Then a lender mentions a hard credit pull, and the question hits fast: Will this hurt my score, and should I let them do it?

That concern is justified. In business lending, credit pulls aren't just administrative background noise. They affect timing, lender choice, and how aggressively you should shop offers. What trips up many owners is that consumer credit advice doesn't always map cleanly to business funding. The biggest gap is rate shopping. Mortgage and auto borrowers often get some protection when multiple inquiries happen close together. Business borrowers usually can't assume that.

A hard credit pull isn't automatically bad. It's a normal part of underwriting. But if you treat every application like a free shot, you can create problems that are hard to unwind when you need capital most.

Table of Contents

- What Exactly Is a Hard Credit Pull

- Hard Pulls vs Soft Pulls for Business Owners

- The Impact of Hard Inquiries on Your Credit

- When Lenders Perform Hard Credit Pulls

- How to Strategically Manage Hard Inquiries

- FAQ for Small Business Borrowers

What Exactly Is a Hard Credit Pull

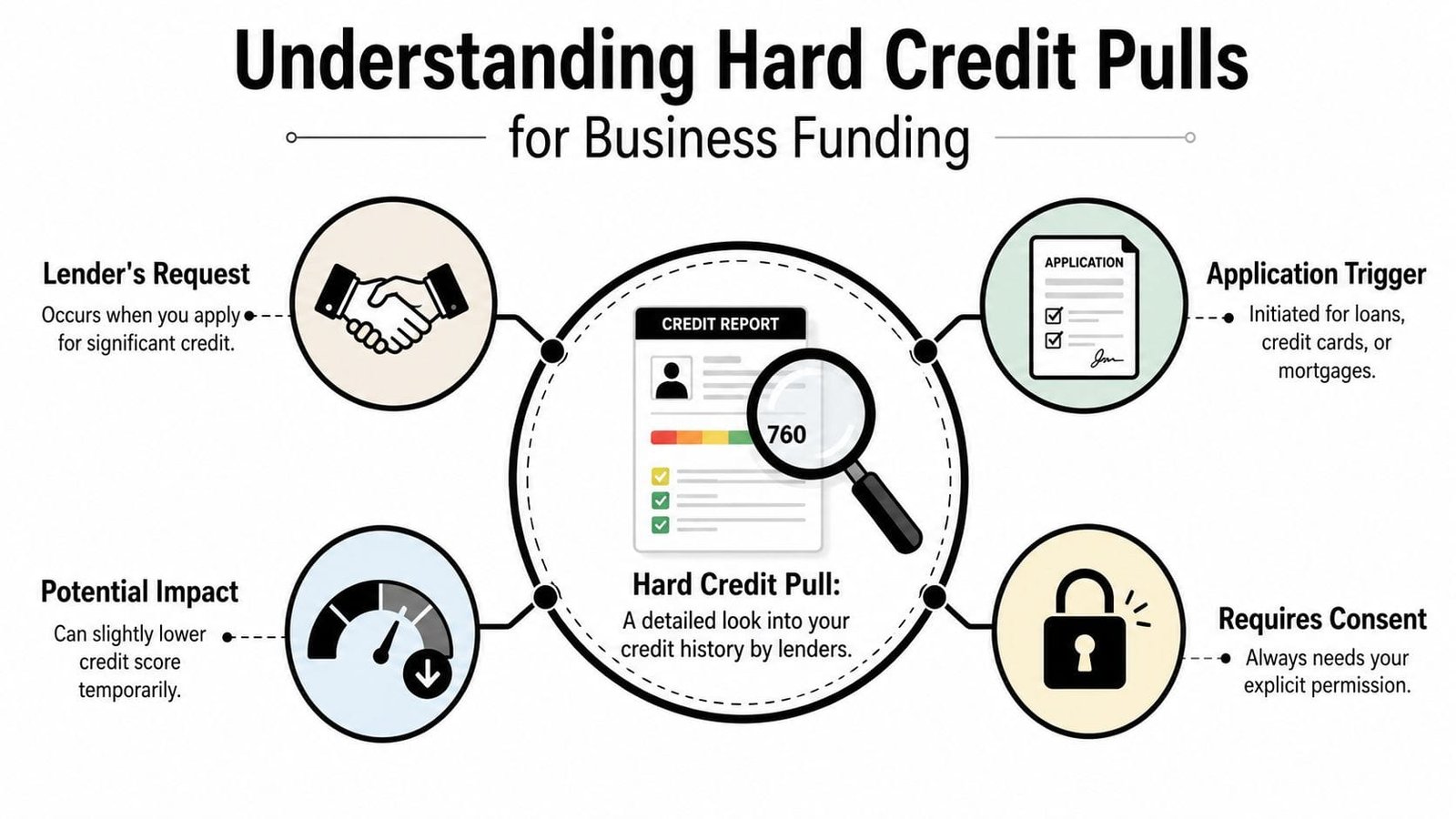

When a lender evaluates a formal credit application, they may ask for permission to review your full credit file. That's what a hard credit pull is. It's an authorized request to access your credit report from one or more of the major bureaus to assess creditworthiness for a new application, including a business loan, and it can lower a score by 3 to 7 points per pull, stay on your report for up to two years, and affect scoring models for 12 months, according to Experian's explanation of hard inquiries.

A hard credit pull is akin to giving a lender a key to your financial house. A soft pull is a glance from the sidewalk. A hard pull is the lender walking through the rooms, opening cabinets, and checking whether the structure is solid enough for them to lend against.

Lenders use a hard pull because they're making a real risk decision. If you're asking for capital, they want a fuller picture than a marketing pre-check can provide. They may review recent inquiries, existing obligations, repayment patterns, and whether you seem to be seeking credit from multiple places at once.

That last part matters more in business lending than many owners expect. A lender isn't only asking, “Can this business use the money?” They're also asking, “How urgently is this owner trying to borrow, and who else might already be in line?”

Practical rule: A hard pull is not a red flag by itself. A pattern of hard pulls in a short stretch can become one.

If you want a second plain-English explainer before you authorize anything, Cash Compass explains credit pulls in a way that's useful for borrowers comparing lending options.

Hard Pulls vs Soft Pulls for Business Owners

A lot of confusion starts here. Owners hear “credit check” and assume every check works the same way. It doesn't.

The practical difference

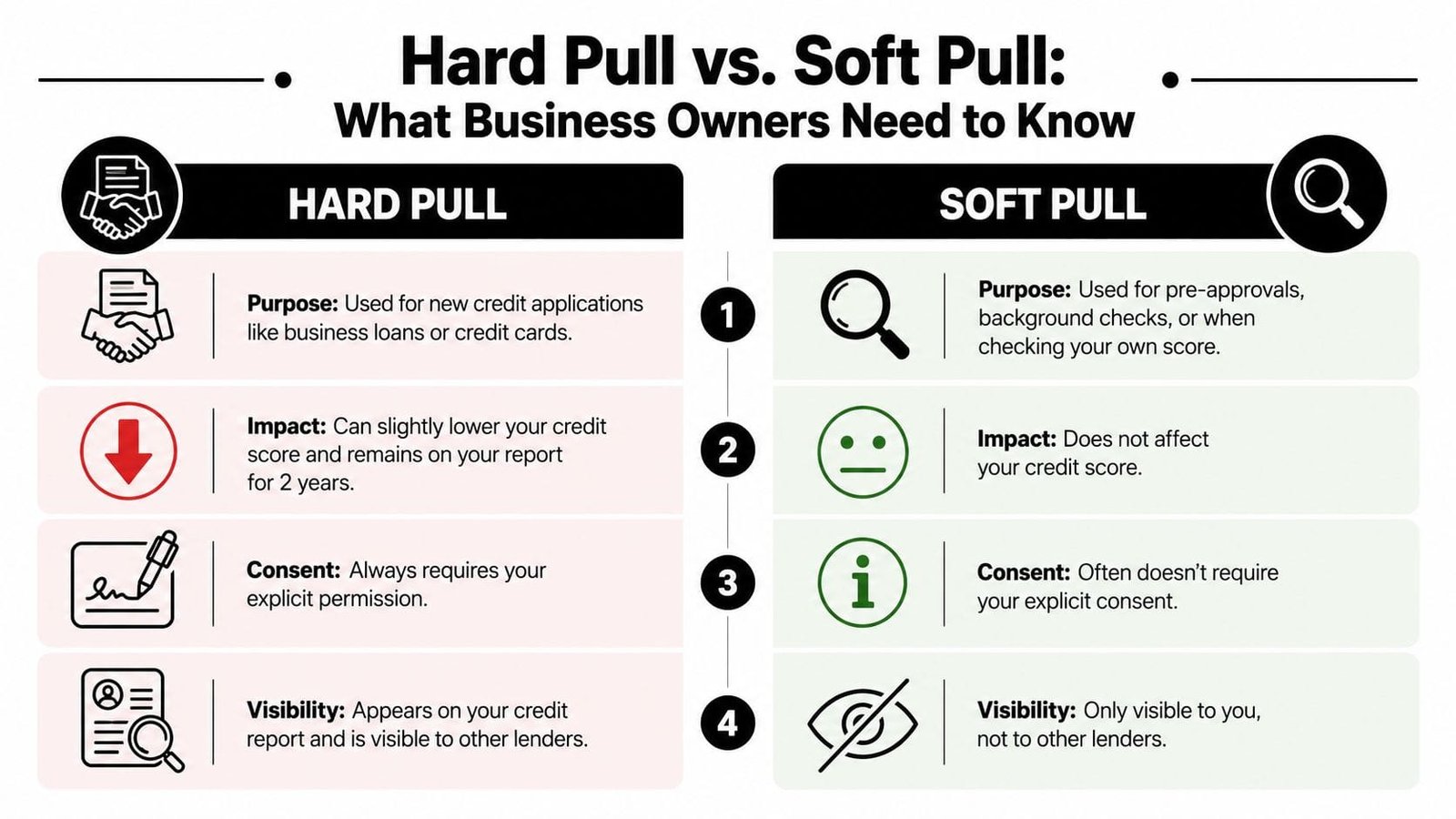

A hard pull happens when you formally apply for credit and authorize the lender to review your report. A soft pull is used for things like prequalification, self-checks, or background reviews. Hard pulls are visible to future lenders and can affect your score. Soft pulls aren't visible to other lenders and have zero score impact, as outlined in Citadel's breakdown of hard vs. soft inquiries.

Here's the side-by-side view business owners need:

| Feature | Hard pull | Soft pull |

|---|---|---|

| Trigger | Formal credit application | Prequalification, self-check, screening |

| Permission | Explicit consent tied to credit request | Often not tied to a formal application |

| Score effect | Can lower score | No score impact |

| Visible to lenders | Yes | No |

| Best use case | Final underwriting | Early-stage shopping |

That difference shapes how you should approach funding. If a lender can only tell you whether you “might qualify” through a soft pull, that's useful for screening. If they need a hard pull to issue a real offer, that's the point where you slow down and decide whether the lender is worth the inquiry.

A lot of business owners benefit from starting with a soft-pull route first. That helps narrow the field before any visible inquiry hits the file. For example, some lenders offer a line of credit pre-approval option that lets you gauge fit before moving into full underwriting.

What this means during funding searches

The expensive mistake is treating soft-pull language as if it applies all the way through approval. It usually doesn't. A lender may advertise a no-impact pre-check, then require a hard pull once you submit the full application package.

This quick walkthrough helps clarify the difference in real terms:

A soft pull helps you explore. A hard pull means the lender has moved from curiosity to commitment.

When you're short on time and need funding fast, it's tempting to fill out every form in front of you. That's usually the wrong move. Use soft-pull prequalification to filter options first. Save hard pulls for lenders that fit your need, your timeline, and the kind of facility you're seeking.

The Impact of Hard Inquiries on Your Credit

A small business owner can absorb one hard pull and still move forward without much trouble. Problems usually start when several lenders pull credit in a short stretch, especially if the owner is applying broadly because cash flow is tight. Underwriters do not just see a score. They also see recent borrowing activity, and that context matters.

What the score impact usually looks like

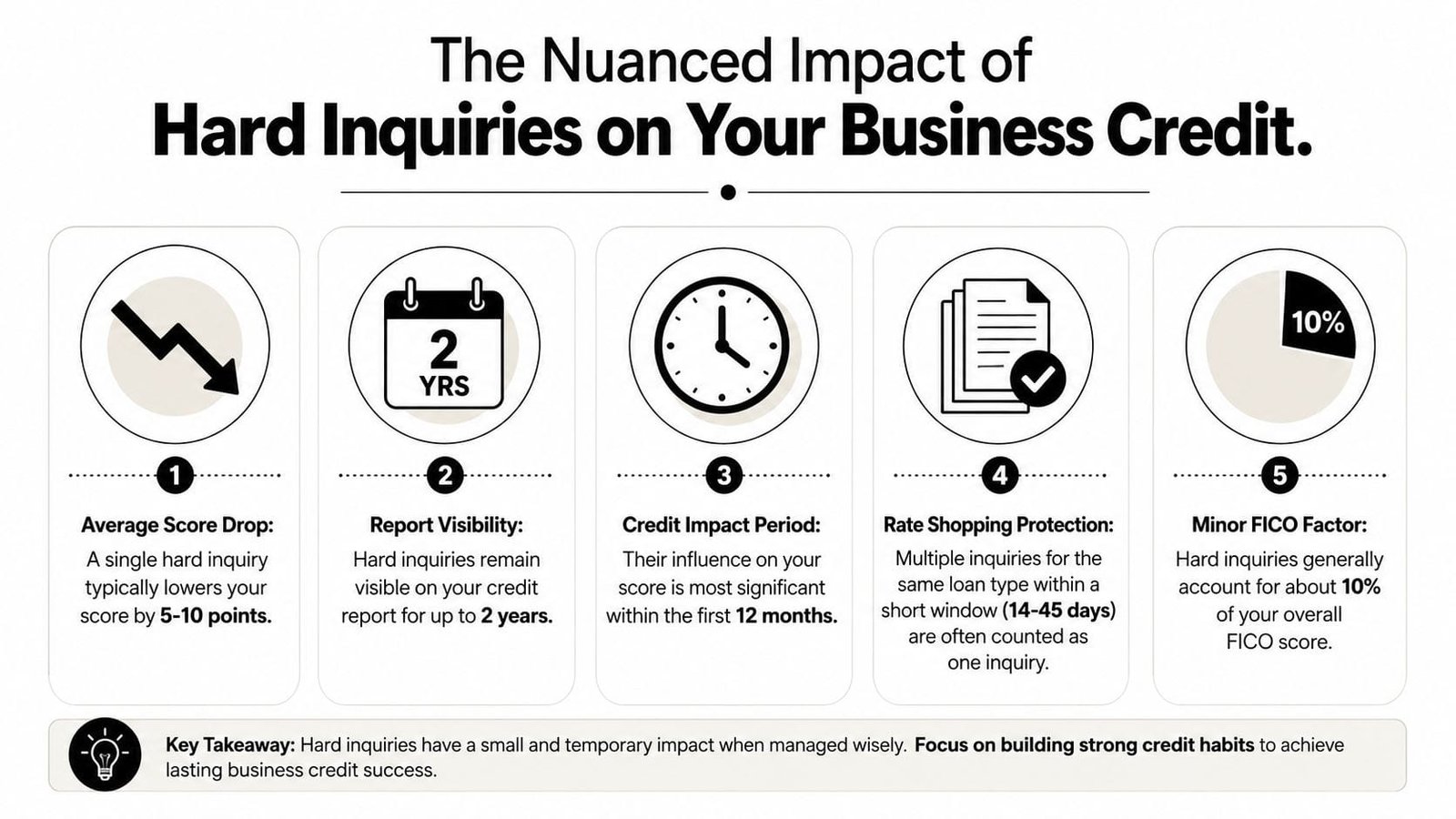

A hard inquiry typically reduces a FICO or VantageScore by 3 to 8 points per pull, with the impact lasting up to 12 months. The inquiry remains visible on the report for 24 months. For borrowers with a thin file, meaning under 5 accounts or less than 2 years of credit history, one hard inquiry can cause a larger drop of 10 to 15 points, based on Credit Karma's overview of hard inquiries.

Two timelines matter here:

- Score-impact clock: the period when scoring models still react to the inquiry

- Visibility clock: the longer period when lenders can still see that the inquiry happened

Those timelines create a practical problem for business borrowers. Your score can start to recover while the inquiry is still sitting on the report for an underwriter to review. If you are applying for financing after a round of declined applications, the score effect may be modest by then, but the pattern still raises questions.

That is why I tell owners to watch both the number and the story. A lender may tolerate a minor score drop. A lender may be less comfortable if your report shows several recent attempts to get credit.

A useful starting point is knowing where your score sits relative to common lending thresholds. This guide on business loan credit score requirements gives a clearer benchmark by product type.

Why this hits business loan shopping differently

General consumer advice can mislead business owners here. In mortgage and auto lending, multiple inquiries for the same type of loan are often treated more leniently during a defined shopping window. That consumer-friendly pattern is not something business borrowers should assume.

In business lending, there is no widely published, standardized rate-shopping window you can rely on across lenders and scoring models. If three business lenders run three hard pulls, the safe assumption is that all three inquiries count separately. That is the part many consumer guides skip, and it matters if you are comparing term loans, lines of credit, or SBA options at the same time.

The trade-off is straightforward. Shopping widely can help you find better pricing or terms. It can also leave a cluster of inquiries on your personal credit file if the lender underwrites the owner along with the business.

For an established borrower with strong income, solid payment history, and a thick file, that may be manageable. For a newer owner, or someone already close to a lender's minimum score, a few extra pulls can be the difference between approval, a reduced offer, or a higher rate.

The practical move is to narrow your lender list before you authorize full applications. Ask who can prequalify with a soft pull, who needs a hard pull for a firm offer, and which products are realistic for your profile. That approach protects your credit file while still letting you compare real funding options.

When Lenders Perform Hard Credit Pulls

A hard inquiry doesn't happen because you asked a casual question. It happens when you move into a formal credit request and authorize the lender to access your file. Hard pulls are triggered exclusively when a consumer formally applies for new credit and grants the lender permissible purpose under federal law. They stay on the credit report for up to two years and affect FICO scoring for the first 12 months, according to Credit Odds' explanation of hard inquiries.

Common business funding moments

In everyday lending, owners most often run into hard pulls during applications for:

- SBA loans

- Business lines of credit

- Term loans for expansion

- Equipment financing

- Business credit cards

- Working capital products that require full underwriting

The same pattern applies in consumer borrowing. Mortgages, auto loans, and new credit cards commonly trigger hard inquiries once the borrower submits a real application instead of a casual pre-check.

In practice, the hard pull often appears at one of these moments:

- You complete a full application rather than a rate check.

- You sign disclosures authorizing the lender to review credit.

- The file moves from initial screening to underwriting.

- The lender needs to issue a firm approval decision rather than a general estimate.

What to ask before you authorize one

A short conversation can save you unnecessary inquiries. Ask direct questions.

- Will this step trigger a hard pull? Don't settle for vague wording like “we may review your profile.”

- Is this prequalification or a full application? Those are different stages.

- What documents are missing before underwriting? Sometimes you can resolve fit issues before credit is pulled.

- Are you evaluating me personally, the business, or both? That matters for owner-guaranteed loans.

If the lender is serious, they should answer cleanly. If they dance around it, assume the inquiry is real and proceed cautiously.

How to Strategically Manage Hard Inquiries

Credit protection isn't about avoiding every hard pull. That's unrealistic if you need capital. The goal is to make each inquiry count.

Before you apply

Start with your own file. Review your personal credit and business records before any lender does. You're looking for obvious friction points such as recent missed payments, reporting errors, or signs that you've already applied too broadly.

Then tighten your borrowing story. Lenders respond better when the request is specific. “We need a line to smooth inventory purchases during seasonal swings” is cleaner than “We're exploring options.” Clarity won't erase a hard pull, but it improves the odds that the pull leads somewhere useful.

If you're also trying to stabilize your broader credit position, this piece on debt relief and credit advice gives a practical outside perspective on improving credit habits before new applications.

Borrower discipline: Don't apply first and organize later. Organize first, then choose where your inquiry budget goes.

While you shop lenders

Business owners get into trouble when they scatter applications across the market. A better approach is controlled sequencing.

- Use prequalification first: If a lender offers a soft-pull screen, take that route before consenting to a full review.

- Pick a primary target: Choose the lender most aligned with your use case, timeline, and collateral structure.

- Keep backup options limited: Have a short bench, not a dozen open applications.

- Ask for the exact trigger point: Find out when the soft review ends and the hard pull begins.

Some borrowers also look for products marketed around lighter credit review processes. If that's relevant to your situation, compare the trade-offs carefully through resources like this guide to a line of credit with no credit check. The key is understanding what you gain in speed or accessibility and what you may give up in pricing, structure, or underwriting depth.

What doesn't work is “shotgunning” the market. Owners do this when cash is tight. They send a full package to multiple lenders and hope one says yes quickly. The result is often a stack of inquiries, inconsistent offers, and a weaker negotiating position with the lenders that could have been a good match.

A strong funding process looks more like triage than shopping. Screen broadly. Apply narrowly. Move fast only after you know which lender deserves the hard pull.

FAQ for Small Business Borrowers

Does a business loan hard pull affect personal credit

Often, yes.

Many business lenders underwrite the owner as much as the company, especially for newer firms, thinner business credit files, or loans backed by a personal guarantee. If the lender pulls your personal credit during that process, the inquiry can show up on your personal report. Your LLC or corporation does not automatically block that.

Ask before you authorize anything: “Are you pulling personal credit, business credit, or both?” That one question prevents a lot of confusion later.

Can you get business funding without a hard pull

Sometimes, at the front end.

A lender may let you check offers through a soft pull, bank statement review, or basic prequalification. That can help you screen options without adding an inquiry to your file. For many term loans, SBA loans, and other fully underwritten products, a hard pull often comes later once you move into a formal application.

That is why “no hard pull” marketing needs a careful read. It may describe the initial screening step, not the final credit decision.

Should you apply to several lenders at once

Usually, no. For small business owners, consumer credit advice often falls short.

With mortgages and auto loans, borrowers may get some protection when multiple inquiries happen within a short shopping window. Business lending is less borrower-friendly. In many cases, there is no clear, standardized rate-shopping window you can rely on for business loan applications, so multiple hard pulls can stack up one by one.

The better approach is controlled comparison. Screen lenders with soft-pull or no-pull steps first. Then choose the few that match your loan purpose, timeline, and collateral profile before you authorize a full application.

Can you remove a hard inquiry if you regret the application

Usually not, if you authorized it.

A valid hard inquiry generally stays on your report for the normal reporting period. Bureaus and lenders do not remove it because the offer was unattractive or because you changed course after applying. The practical focus should be prevention. Confirm the pull type and the trigger point before you proceed.

What's the safest way to shop for business funding

Use a staged process instead of treating every lender conversation like an application.

Start with fit. Look for soft-pull prequalification when available, and match the product to the need. A seasonal cash gap, an equipment purchase, and a long-term expansion plan should not all be sent through the same lending funnel.

Then tighten the field.

- Check qualification method first: Ask whether the first review is a soft pull, hard pull, or business credit check.

- Match the product to the problem: Short-term working capital and long-term asset financing should be evaluated differently.

- Limit full applications: Apply only where terms, structure, and approval odds make sense.

- Track your authorizations: Keep a running list of which lenders have permission to pull credit.

Every hard pull for a business loan should be intentional.

If you want to explore business funding without taking a scattered-application approach, Business Loan Warrior offers a practical starting point. You can review options, check pre-approval paths, and move toward the right funding product with more clarity before committing to full underwriting.