Gross revenue is the total sales income your business generates before any expenses, returns, or discounts are taken out. If you sell 1,000 units at $25 each, your gross revenue is $25,000.

That sounds simple until you're filling out a loan application and suddenly realize one basic question has a dozen practical versions. Do you count only product sales? What about service retainers, subscriptions, royalties, interest, or a one-time asset sale? If your bank statements, P&L, and application don't match, a lender notices fast.

I talk to business owners who know they had a strong month, a strong quarter, or even a record year, but still feel unsure when they have to present the numbers. That uncertainty matters. Lenders don't just want a big top-line figure. They want a clean, believable one that matches the story your documents tell.

Table of Contents

- Gross Revenue Is More Than Just a Number

- A Clear Definition What Gross Revenue Really Is

- How to Calculate Gross Revenue For Your Business

- Gross Revenue vs Other Key Financial Metrics

- What Lenders See When They Look at Your Gross Revenue

- Common Gross Revenue Reporting Mistakes to Avoid

- Making Your Gross Revenue Tell a Winning Story

Gross Revenue Is More Than Just a Number

A business owner closes out the month, sees strong deposits, and feels relieved. Sales were busy. Staff stayed moving. Customers kept buying. Then the financing application asks for gross revenue, monthly revenue, annual revenue, and supporting statements, and the confidence starts to wobble.

That reaction is normal because gross revenue sounds like a basic accounting term, but to a lender it's the opening signal. It's the first clue about how much business activity your company generates. Before anyone studies your margins, debt load, or working capital, they want to know whether customers are showing up and spending money.

Why owners hesitate on this number

The hesitation usually comes from one of three places:

- Multiple income streams: You sell products, offer services, and maybe collect another kind of payment that doesn't fit neatly into one bucket.

- Different documents show different totals: Your bookkeeping software may categorize income one way, while your tax documents group it another way.

- You're worried about saying the wrong thing: If you overstate revenue, you look sloppy. If you understate it, you may weaken your application.

Practical rule: A lender can work with a business that has uneven numbers. It's much harder for them to work with numbers that don't reconcile.

What the number says before you say anything

Think of gross revenue as the cover page of your business's financial story. It doesn't tell the whole plot, but it tells a lender whether the story is worth reading.

A healthy gross revenue figure can suggest demand, traction, and market presence. A confusing gross revenue figure suggests cleanup work, unclear reporting, or a business owner who may not have tight control over the books. That doesn't mean the business is weak. It means the presentation needs work.

When you understand what gross revenue means and how to show it correctly, you stop treating the application like a guessing game. You start using the number the way a lender reads it.

A Clear Definition What Gross Revenue Really Is

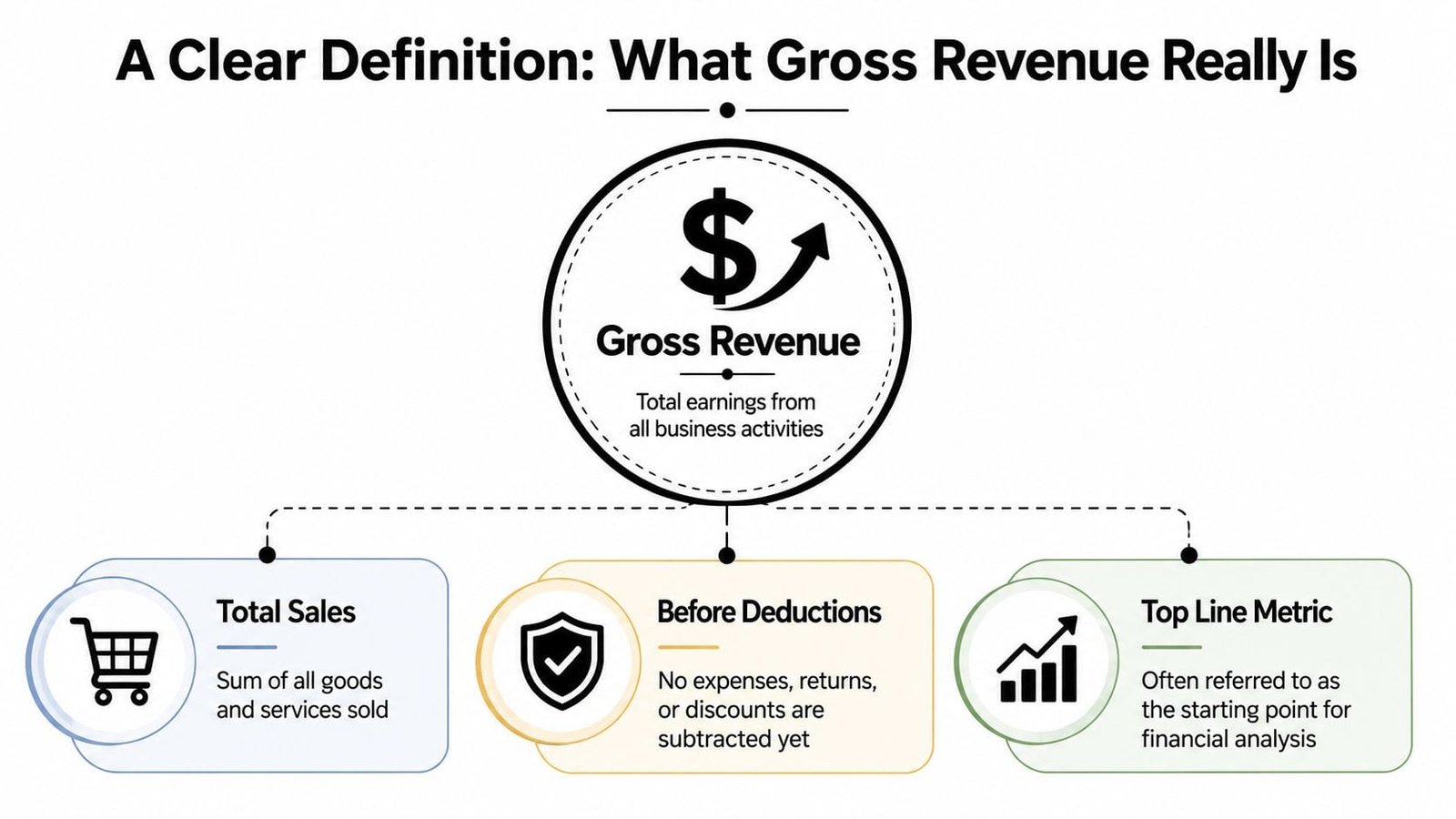

Gross revenue is the top-line figure in accounting. It is the total amount a business earns from sales or services before any deductions for returns, allowances, discounts, taxes, or operating expenses, as explained in Stripe's overview of gross-to-net revenue.

Think of it like the cash collected at a market stall

If you run a stall at a Saturday market, gross revenue is the total money customers hand over during the day. It's the amount collected before you subtract booth fees, card processing charges, spoiled inventory, payroll, or any discount you later honor.

That's why lenders care about it. It answers a very direct question: How much customer buying activity does this business generate before costs pull the number down?

Stripe also gives a simple example. If a company sells 1,000 units at $25 each, its gross revenue is $25,000 in that same explanation of top-line revenue. The point isn't just the math. The point is that gross revenue captures sales activity first, before the rest of the accounting story begins.

Why this definition matters on a loan application

Many owners hear “revenue” and think “money left over.” That's where confusion starts. Gross revenue is not what you keep. It's what you brought in from selling your product or service before deductions.

A lender knows this. If you report gross revenue like it's profit, your numbers will look off the moment they compare your application to your statements.

Use this checklist when you're asked for gross revenue:

- Start with sales activity: Include what the business earned from selling goods or services.

- Keep deductions separate: Don't mix in expenses, operating costs, or the amounts you spent to make the sale.

- Match your documents: The figure should line up with the financial statements you submit.

Gross revenue is your business at full volume, before accounting turns that activity into narrower measures.

If you've ever searched for what is gross revenue and felt like every answer was technically right but still not practical, that's the missing piece. The definition is simple. The main challenge is using it correctly when someone is underwriting your business.

How to Calculate Gross Revenue For Your Business

The core formula is straightforward. Gross revenue = units sold × price per unit. The IRS also defines gross receipts as total amounts received from all sources during an annual accounting period without subtracting any costs or expenses, which is why lenders see this as a standardized starting point in financial review, as noted in the IRS definition of gross receipts.

Three business models, three ways to think about it

A coffee shop can use the formula by counting drinks, food items, and other items sold, then multiplying by selling price. A consulting firm can apply the same logic to billable hours or fixed-fee engagements. A software company can apply it to active subscriptions billed during the period.

The structure changes by business model, but the logic doesn't. You're still measuring total incoming sales activity before subtracting costs.

Here's a practical way to approach it:

- Pick the period first: Monthly, quarterly, or annual figures all work, as long as you stay consistent.

- Pull sales data from one source of truth: That might be your POS, invoicing platform, subscription system, or accounting software.

- Add all qualifying sales for that period: Don't subtract payroll, rent, refunds still under review, or other expenses in this step.

- Reconcile the total to your statements: If the application asks for monthly gross revenue, make sure the reported number ties back to the financials you submit.

The process matters as much as the formula

A lot of reporting errors don't come from bad math. They come from scattered records. One system tracks invoices. Another tracks deposits. A third tracks adjustments. If your team is still doing much of that manually, tools and workflows like Matil's guide to invoice automation can help reduce avoidable mismatches.

If you're trying to separate top-line sales from what the business kept after expenses, it also helps to understand how lenders view earnings. This guide on finding net income for small business financing is useful for that next layer.

A clean calculation does two jobs at once. It gives you a reliable number, and it shows the lender that your reporting process is under control.

Gross Revenue vs Other Key Financial Metrics

People mix up gross revenue, net revenue, and gross profit all the time. That confusion can make a loan package harder to underwrite because each metric answers a different question.

Start with this: gross revenue is the starting point. Other metrics come after deductions.

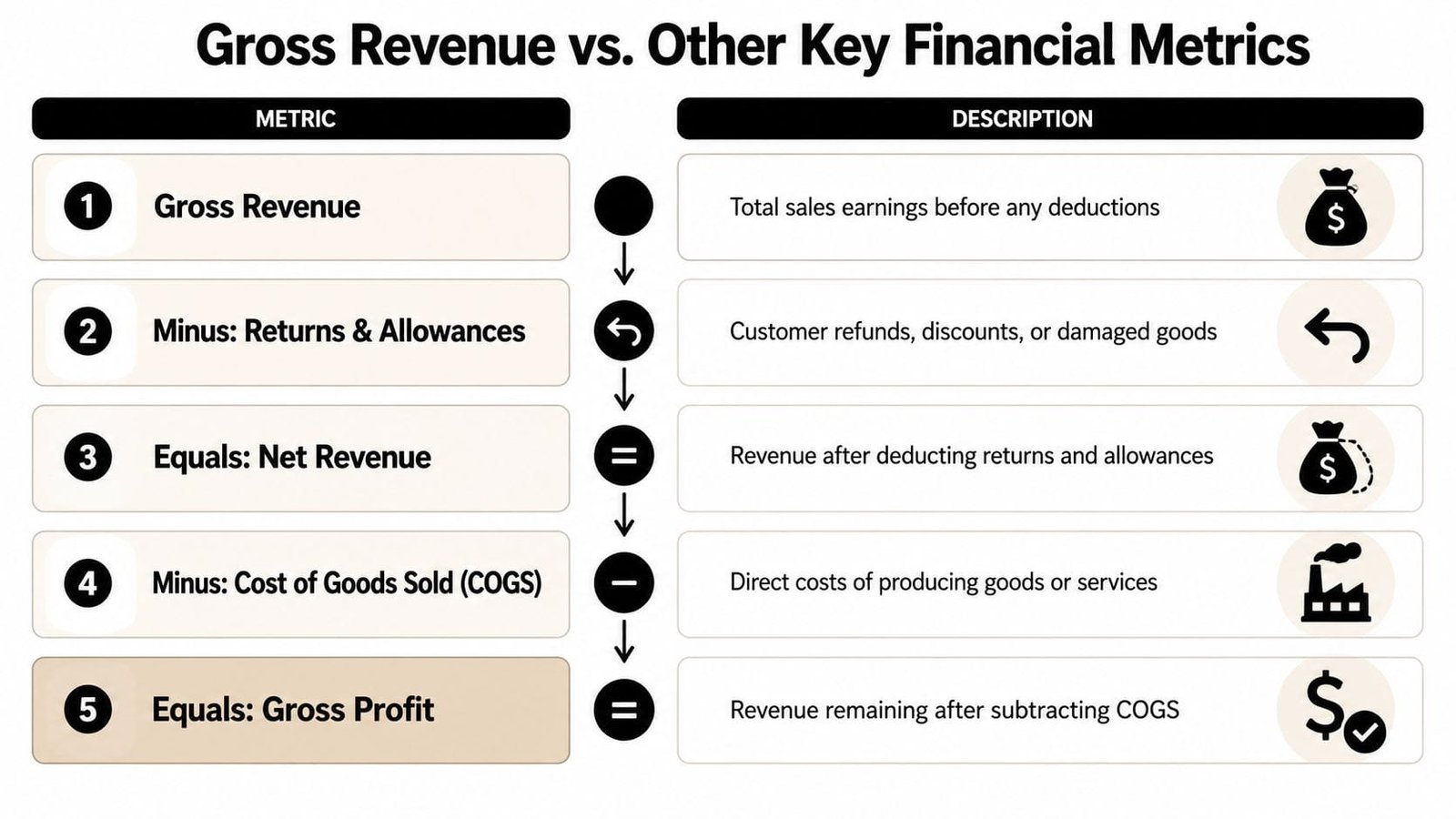

The basic funnel lenders think through

A lender often reads your numbers like a funnel:

- Gross Revenue: Total sales earnings before deductions.

- Net Revenue: What remains after returns, allowances, and discounts are taken out.

- Gross Profit: What remains after subtracting the direct cost of producing the goods or delivering the service.

That progression matters because a business can have strong sales activity and still struggle with returns, weak pricing, or high direct costs. Gross revenue shows scale. Net revenue shows what sales were retained. Gross profit starts to show whether the core offering has breathing room.

Here's a simple example without adding new figures. Say your company had a strong sales month. Some customers returned items. A few invoices were discounted. That lowers net revenue. Then you subtract the direct cost of inventory or labor tied to delivery. What's left is gross profit.

That's why these terms aren't interchangeable.

To make the distinction easier to visualize, watch this short overview:

A side-by-side comparison

| Metric | What It Measures | Simple Formula | What It Tells a Lender |

|---|---|---|---|

| Gross Revenue | Total sales activity before deductions | Sales before returns, discounts, and expenses | Business size and demand |

| Net Revenue | Revenue after sales-related deductions | Gross revenue minus returns, allowances, and discounts | Revenue quality and how much sales stick |

| Gross Profit | Revenue left after direct production or delivery costs | Net revenue minus cost of goods sold | Whether core operations generate room to cover overhead and debt |

A lender doesn't want one good number. They want to see whether each number leads logically to the next.

If you want a broader owner-level review of key financial metrics for businesses, that resource is helpful because it puts revenue in context with other operating measures. And when lenders move past top-line sales, they also look at liquidity. This explanation of a healthy working capital ratio and loan approval helps connect that next step.

What Lenders See When They Look at Your Gross Revenue

Lenders don't stop at the number itself. They read what the number suggests about your operation.

A strong gross revenue figure tells them the business has customer activity. It suggests the market recognizes your offering, your sales channels are functioning, and the company has enough commercial motion to deserve a closer look. Even before they examine profitability, they're asking whether the business is real, active, and capable of bringing money through the front door consistently.

Gross revenue shows business scale

From a lender's seat, gross revenue is one of the fastest ways to size a company. It helps them understand whether they're looking at a small local operator, a growing regional business, or a larger company with more established sales volume.

It also helps them compare periods. If revenue appears steady, seasonal in a predictable way, or trending upward, that shapes the lender's comfort level. If it swings sharply without explanation, they'll want context.

What helps here is narrative, not spin. If a quarter was softer because one product line was paused, say that plainly. If sales improved after a location reopened or a contract resumed, explain that too.

Gross revenue also shows discipline

The number itself matters. The way you support it matters just as much.

Lenders look for consistency across:

- Application figures: What you typed into the form

- Financial statements: Your P&L and related reports

- Bank activity: Deposits that support the revenue story

- Tax filings: The formal record of how the business reported income

If those sources disagree, the lender doesn't just question the total. They question the reporting process behind it.

Clean revenue reporting lowers friction in underwriting.

If you want to think like an underwriter, this article on pressure-testing revenue consistency before loan approval is worth reviewing. It mirrors the kind of consistency checks many lenders perform behind the scenes.

Gross revenue won't win approval by itself. But without a credible top line, the rest of the application has a much harder time standing up.

Common Gross Revenue Reporting Mistakes to Avoid

Many explanations of gross revenue skip the part that causes real trouble in applications. The hard part often isn't the definition. It's deciding what counts.

A major reporting ambiguity is whether gross revenue should include only operating sales or also other inflows like royalties and interest. The practical answer depends on whether the number is being used for internal management, GAAP reporting, or lender underwriting, as discussed in Paddle's explanation of gross revenue ambiguity.

Where owners get tripped up

The biggest mistakes usually look like this:

- Mixing core sales with unrelated inflows: If you sold equipment, earned interest, or received a non-operating payment, don't bury it inside core sales without labeling it.

- Using different methods across documents: If your application uses one revenue basis and your statements use another, underwriting slows down.

- Leaving out a sales channel: Online orders, retail sales, wholesale invoices, subscriptions, and service retainers all need to be captured consistently.

- Confusing gross revenue with cash left after expenses: That turns a revenue figure into something closer to profit and creates avoidable inconsistencies.

How to present mixed income clearly

If your business has mixed income streams, clarity beats oversimplification.

You don't need to force every dollar into one bucket. You need to separate categories in a way a lender can follow. For example, list operating revenue as one line and other income as another. If a one-time inflow affected the period, note that directly. That approach helps a lender evaluate recurring sales power instead of guessing.

A good lender-ready presentation usually includes:

- A primary revenue figure: Your operating sales, shown consistently.

- A short note on non-operating items: Keep these separate if they materially affect the period.

- Matching backup: P&L, bank statements, and tax records should support the same logic.

If a number needs explanation, add the explanation before the lender has to ask.

That small step can prevent a simple reporting issue from looking like a credibility issue.

Making Your Gross Revenue Tell a Winning Story

Knowing what gross revenue is gives you the starting point. Presenting it well is what makes the number useful.

A lender wants more than a total. They want a revenue story they can trust. Is the business stable? Growing? Recovering? Diversified? Concentrated in one client or channel? The cleanest applications answer those questions without forcing the underwriter to hunt for clues.

Keep your presentation simple:

- Use one clear reporting method

- Separate core sales from unusual inflows

- Make sure your documents reconcile

- Be ready to explain swings in plain language

- Show the trend, not just the headline number

When you do that, gross revenue stops being a term you hope you're using correctly. It becomes evidence that your business has activity, demand, and reporting discipline. That combination gives lenders something they can work with.

If you're preparing for funding and want a faster way to turn your numbers into a lender-ready application, Business Loan Warrior helps small business owners compare financing options, check pre-approval through a single application, and move from financial review to funding with more clarity and less back-and-forth.