You're ready to move on a growth plan. Maybe it's inventory, equipment, a second location, or a working-capital cushion so you can stop managing every week like it's an emergency. You apply for financing, and the lender asks for business bank statements.

That request catches a lot of owners off guard.

They think the underwriter wants tax returns, a P&L, maybe a balance sheet. Those matter. But if you've ever sat on the lending side of the desk, you know why statements get requested early and reviewed hard. They show how the business behaves when money comes in, when bills hit, and when pressure builds.

A clean set of business bank statements can move an application forward fast. A messy set can slow it down even when revenue looks solid on paper.

Table of Contents

- Why Bank Statements Matter More Than You Think

- Deconstructing Your Business Bank Statement

- The Lender's View on Your Financials

- Decoding What Underwriters Want to See

- Bank Statements Compared to P&L and Tax Returns

- Red Flags That Halt Loan Applications

- Your Pre-Application Bank Statement Checklist

Why Bank Statements Matter More Than You Think

When a lender asks for statements, they aren't asking for busywork. They're asking for the closest thing they can get to a direct read on your operating cash flow.

A business bank statement is typically issued on a monthly or 30-day cycle and gives a transaction-by-transaction record of deposits, withdrawals, checks paid, and service charges. That's why it's a foundational tool for cash-flow analysis. It shows what moved through the account, not what was projected or invoiced on paper, as explained in Bill's overview of business bank statements.

That distinction matters more than most owners realize.

A P&L can show profit while the bank account is under strain. An invoice can show revenue that hasn't arrived yet. A statement shows whether cash landed, when it landed, and what happened to it next. For an underwriter, that's the difference between a theoretical repayment source and a verified one.

Practical rule: If your financials tell one story and your statements tell another, the statements usually win.

There's also a rhythm to statement review that many borrowers never see. Underwriters compare one month to the next, looking for continuity. They want to know whether deposits are stable, whether outflows make sense for the business model, and whether the account is managed with discipline or patched together under pressure.

That's why strong statements speed things up. They reduce the number of follow-up questions. They make your application easier to defend inside a credit team. And in many files, they do more to shape the decision than owners expect.

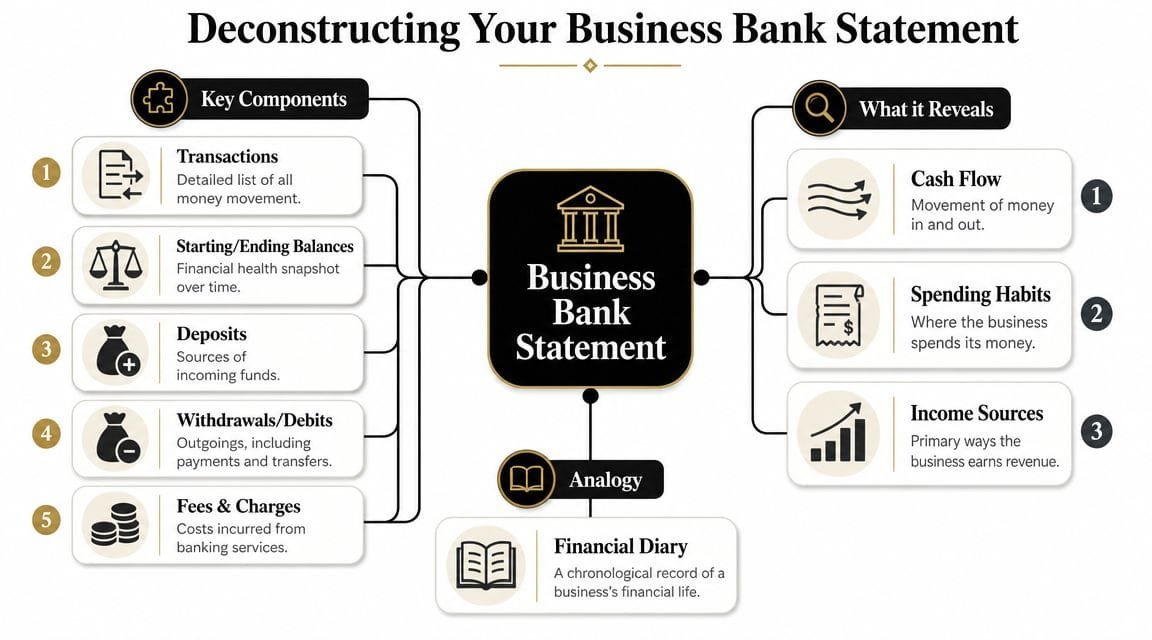

Deconstructing Your Business Bank Statement

Think of your statement as your business's financial diary. Not the polished version you'd show at a board meeting, but the unvarnished account. It records the timing, sequence, and texture of money moving through the company.

The summary tells the first story

Most statements open with a summary box. Underwriters usually start there because it gives them a fast orientation.

That summary typically includes the opening balance, closing balance, and broad categories of account activity such as deposits, withdrawals, and fees. On a practical level, this is the first signal of whether the account stayed steady, built cash, or ended the period weaker than it began.

What matters here isn't a single line item. It's the relationship between them.

If deposits look healthy but the closing balance keeps falling, the business may be leaking cash faster than it collects it. If fees keep appearing, the account may be running too close to the edge. If the opening balance on one statement doesn't line up with the prior closing balance, an underwriter will want to know why.

The transaction detail tells the real story

The body of the statement is where the file either gets stronger or starts to unravel. Each transaction usually includes a date, description, and amount, which makes the statement useful for matching cash activity against invoices, recurring bills, and internal records. Finli explains that this transaction-level view helps lenders and accountants identify timing gaps, bank-only charges, and unrecorded payments in its guide to reading a bank statement as a small business owner.

That's why underwriters don't just scan totals. They look at patterns.

A series of customer deposits that land on a predictable cadence is easier to credit than sporadic lump sums with vague descriptions. Regular outgoing payments to vendors, payroll providers, landlords, or utilities often support the story that the business is operating normally. Random transfers, reversals, and unexplained withdrawals do the opposite.

A good habit is to review your statements the same way an outsider would:

- Check the account identity: Make sure the legal business name and account details are correct and consistent.

- Read the month in sequence: Look for timing gaps, unusual spikes, or periods where money came in late but bills still hit.

- Notice bank-generated entries: Fees, returned items, and similar lines often reveal stress before owners mention it.

- Match reality to your books: If the statement and internal reporting disagree, fix the books before you apply.

Your statement doesn't need to look perfect. It needs to look understandable, consistent, and credible.

The Lender's View on Your Financials

Owners often ask why a lender needs bank statements when they've already provided a P&L or tax return. The short answer is simple. Statements show liquidity in motion.

Cash movement beats reported intent

A P&L tells me whether the business appears profitable over an accounting period. A tax return tells me what was reported historically for tax purposes. Both are useful. Neither tells me, with the same clarity, what cash did inside the operating account.

Underwriting is full of judgment calls, but one concern always sits near the top. Can this business handle its obligations without running out of room?

That's why statements carry so much weight. They reveal whether receivables turn into deposits, whether expenses hit in a controlled way, and whether the company has enough breathing room between inflows and outflows. If you lend money, you care about repayment from real operating behavior, not just reported performance.

Why underwriters trust statements

Business bank statements also benefit from being issued by the bank itself on a recurring cycle. They function as an outside record of activity rather than a document created internally for presentation. That makes them a grounding document when the rest of the file feels too polished.

They're also useful because they can be reconciled across periods. Analysts can compare opening and closing balances, track chronology, and test whether the movement on the account aligns with the borrower's story. When it does, confidence rises. When it doesn't, the file gets slower.

Here's the trade-off in plain terms:

- P&L statements can explain the business model.

- Tax returns can show historical earning power.

- Bank statements can prove current operating behavior.

A lender doesn't get repaid by net income on a spreadsheet. A lender gets repaid by cash arriving in the account and staying there long enough to cover obligations.

That's why a borrower with average-looking financial statements but strong cash management can still look financeable. The reverse is true too. A borrower can show solid revenue and still raise concern if the statements show constant strain.

Decoding What Underwriters Want to See

A business owner submits statements that show solid monthly sales, but the account still dips close to zero three or four times before each statement closes. From an underwriting seat, that file does not read as stable revenue. It reads as tight cash timing.

When I review business bank statements, I want a cash pattern that makes sense on its own. The best files are easy to follow. Deposits arrive in a rhythm that matches the business model. Expenses look tied to real operations. Balances hold enough cushion that one slow week does not put the account under stress.

Patterns that build confidence

Underwriters read statements the way a mechanic listens to an engine. We are checking whether the business runs smoothly, whether it strains under load, and whether the story holds up from page to page.

Consistent deposits help, but context matters more than sameness. A contractor may show lumpier inflows than a subscription business. A retailer may spike around holidays. What helps the file is a deposit pattern that matches how the company gets paid.

Average daily balance often matters more than the ending balance. Owners sometimes transfer money in just before month-end to make the account look stronger. Underwriters usually spot that quickly. We look for how the account behaved between statement dates, especially whether it spent long periods near the floor.

Transaction descriptions matter for a practical reason. Clear merchant names, repeat customer payments, normal payroll debits, tax payments, rent, and vendor activity give the file a believable operating rhythm. If half the account is transfers between personal apps, cash withdrawals, or unexplained incoming wires, the lender has to stop and ask questions.

What strong statement hygiene looks like

Strong statement hygiene usually looks like this:

- Revenue lands in the main business account. That lets the lender verify where sales settle.

- Payments out match the business model. Payroll, inventory, software, rent, shipping, and vendor payments should look like a real operating company.

- Transfers are limited and easy to explain. Frequent movement between accounts is not always a problem, but it creates extra work and more room for doubt.

- Returned items and overdraft behavior stay rare. One isolated issue may be explainable. A pattern suggests weak control.

- Bookkeeping and bank activity line up. If reported profit says one thing and the account activity suggests another, underwriting slows down.

One point trips up a lot of borrowers. Deposits are not the same as profit. If you need a cleaner read on that distinction before applying, review this guide on how to find net income.

The unwritten rule is simple. Every statement page should reduce uncertainty. If an underwriter can trace how money comes in, where it goes, and how much stays available, the file moves faster. If each page creates a new question, even a good business can become a harder approval.

Bank Statements Compared to P&L and Tax Returns

Most loan packages ask for more than one financial document because each one answers a different question. Problems start when owners assume the documents are interchangeable.

How each document helps a credit decision

Here's the cleanest way to think about it.

| Criterion | Business Bank Statements | Profit & Loss (P&L) | Tax Returns |

|---|---|---|---|

| Verification level | Bank-issued record of account activity | Internally prepared financial report | Filed historical tax document |

| Primary lens | Cash movement and liquidity | Profitability over a reporting period | Historical taxable income |

| What a lender learns | How money actually moved through the account | Whether operations appear to generate profit | What the business reported to tax authorities |

| Best use in underwriting | Validating operating behavior and repayment rhythm | Understanding margins and operating structure | Confirming longer-term history |

| Main weakness | Doesn't explain full accounting context by itself | May not reflect real-time cash pressure | Often backward-looking and less useful for current momentum |

Business bank statements are the ground-truth document when the question is, “What happened in the account?” A P&L is better when the question is, “Did the business earn money on paper?” A tax return is better when the question is, “What has this business reported over time?”

That's why lenders frequently want all three. Together, they form a triangulation exercise. If all three line up, the file feels coherent. If they don't, the lender has to decide which document best reflects reality.

Some business owners look specifically for funding that doesn't rely on statement review. If that applies to your situation, this overview of business loans with no bank statements lays out when that path may or may not fit.

The practical takeaway is straightforward. Don't send statements thinking they're just backup documentation. In many files, they are the document that either confirms or challenges everything else you submitted.

Red Flags That Halt Loan Applications

A file usually stalls for one of two reasons. The cash pattern suggests stress, or the statements make the business hard to trust.

From an underwriter's seat, red flags are rarely about one ugly transaction. I can work around a bad week or a one-time dip if the rest of the account behavior makes sense. What slows approvals is a pattern with no cushion, no controls, or no explanation.

The issues that force a second look

Frequent negative balances, returned payments, and recurring overdraft or NSF fees are the first things many lenders notice. Those items signal that cash is arriving too late, bills are hitting too early, or the owner is running the account with no room for error. A business can still be selling well and have this problem. That is exactly why it matters. Strong revenue does not help much if timing risk is constant.

Co-mingling creates a different problem. If grocery charges, family subscriptions, or other personal spending run through the business account, the statement stops being a clean operating record. Underwriters then have to separate business activity from owner behavior, and that usually means slower review, more questions, and less confidence in the numbers presented elsewhere.

Large unexplained transfers are another common stop sign. Transfers between related accounts can be harmless, but only when they are easy to trace and consistently described. If money keeps leaving the operating account without a clear purpose, an underwriter may assume it is masking debt service, owner draws, payroll pressure, or obligations not listed on the application.

Then there is document integrity. Missing pages, broken date sequences, balances that do not roll forward properly, or statement fields that look altered can move a file out of credit review and into fraud review. Once that happens, approval gets much harder.

If a statement looks edited, incomplete, or internally inconsistent, the review often shifts from repayment analysis to document verification.

How to clean up a weak statement file

Start with account discipline. Keep business revenue and business expenses in the business account, and stop using that account for personal spending. That one fix improves clarity faster than almost anything else.

Next, get ahead of unusual activity. If you transfer money to another account every month, label it clearly and be ready to explain it the same way every time. Inconsistent explanations hurt more than the transfer itself.

Then fix the presentation problems that create avoidable friction.

- Remove co-mingling going forward: Use separate cards and accounts for owner spending and business operations.

- Review every page before upload: Missing pages, cut-off transaction detail, and out-of-order statements create immediate delays.

- Watch recurring fees and returned items: One fee can be noise. A repeating pattern usually reads as weak cash management.

- Document related-account transfers: Keep a short note on what moved, where it went, and why.

- Reconcile monthly, not during the loan process: A simple bank statement variance tracker for faster SMB approvals helps catch issues before an underwriter does.

A lender can often live with a rough month. A repeated pattern with no explanation is what gets files set aside.

Your Pre-Application Bank Statement Checklist

Strong applications are usually boring in the best way. The statements are complete, legible, consistent, and easy to verify.

What to review before you connect accounts

Before you submit anything, run through this short checklist:

- Confirm the account name: Make sure the business name on the statement matches the legal business entity or DBA used in the application.

- Check statement completeness: Include every page. Summary-only uploads create delays because underwriters need the transaction detail.

- Scan for red flags: Review recent months for overdrafts, unusual withdrawals, or items that will need explanation.

- Match books to bank activity: Your accounting records should make sense against the statement trail.

- Prepare brief notes: If something unusual happened, write a concise explanation before the lender asks.

If you want a practical way to organize monthly reviews, this walkthrough on how to build a bank statement variance tracker for faster SMB approvals is a smart operational habit.

How to submit statements without creating delays

Use secure upload or bank-connection tools when they're available. Don't email sensitive statements around loosely if the platform gives you a protected submission path. Underwriters want clean files, but they also want an unbroken document trail.

A second habit helps too. Download and review your statements as soon as each cycle closes. Since business bank statements are generally issued on a recurring monthly cycle, waiting until you urgently need financing often means you're seeing problems for the first time under deadline pressure.

Here's a quick demo format that many borrowers find helpful before they submit documentation:

The goal isn't to make your statements look prettier. It's to make them easier to underwrite. When your records tell a clean story, the lender spends less time asking what happened and more time deciding how to approve the request.

Business Loan Warrior gives small business owners a faster path from application to funding. With a single, no-fee application, secure bank connectivity, and access to real underwriters, Business Loan Warrior helps you check pre-approval, compare funding options, and move forward with less friction.