Yes, late payments do affect your credit score, and once a creditor reports a payment that is 30 or more days past due, the damage can stay on your credit report for up to seven years. The severity depends on how late the payment is, and a single reported late payment can cut a strong score by about 100 points or more.

If you're a business owner, that isn't just a consumer finance problem. It's a capital access problem.

A missed personal card payment often happens during the exact kind of season when you're most distracted. Payroll is heavy, inventory is moving, a vendor is pressing for faster terms, and your inbox is full of approvals, statements, and renewal notices. Then a personal account slips. Not by much at first. But if it crosses the reporting line, that one oversight can follow you into your next equipment loan, line of credit renewal, or SBA application.

Lenders don't look at late payments in isolation. They read them as signals. A recent delinquency can raise doubts about repayment discipline, even when revenue is solid and the business is profitable. For owners who personally guarantee financing, that signal matters.

Table of Contents

- Introduction The Silent Threat to Your Next Business Loan

- The 30-Day Rule How Late Payments Get on Your Credit Report

- The Escalating Damage of Delinquency

- Personal vs Business Credit A Double-Edged Sword for Owners

- Beyond the Score How Lenders React to Late Payments

- Damage Control A Business Owner's Guide to Credit Recovery

- Building a Bulletproof Payment System for Your Business

Introduction The Silent Threat to Your Next Business Loan

A business owner can do almost everything right and still get tripped by one late payment.

I've seen the pattern often enough that it no longer surprises me. The company is growing, the owner is reinvesting aggressively, receivables are a little slow this month, and personal accounts get less attention because the business always comes first. Then a lender pulls credit for a funding request and finds a fresh delinquency sitting there like a warning label.

That late payment may have started as a simple oversight. To a lender, it can look like stress, disorganization, or weakening liquidity. None of those interpretations help when you're asking for capital.

Bottom-line view: A late payment is rarely just about a score. For a business owner, it's about whether the next lender sees stability or risk.

This matters most when personal credit is tied directly to business borrowing. Many owners assume the lender will focus on revenue, time in business, collateral, or tax returns. Those factors matter. But a recent derogatory mark on personal credit can still complicate the file, especially when the owner is the guarantor.

The hidden danger is timing. A late payment doesn't hurt only when it happens. It hurts when you need money soon after it happens. That could be during an acquisition, a truck purchase, a location buildout, or a seasonal working capital push.

So when owners ask, "Do late payments affect credit score?" the practical answer is larger than the question. Yes, the score can drop. But the bigger issue is how that drop reshapes lender confidence, pricing, and options at exactly the wrong moment.

The 30-Day Rule How Late Payments Get on Your Credit Report

This distinction is often misunderstood. Being late and being reported late are not the same thing.

A creditor may treat your payment as late almost immediately under the account terms. You can get a fee, a penalty, or a collection call before your credit report changes. But for credit reporting purposes, the serious line is typically 30 days past due. Experian explains that payment history accounts for about 35% of a FICO Score, and once a creditor reports a payment that is 30 or more days past due, that mark can stay on your report for up to seven years from the delinquency date. Experian also notes that FICO is used by 90% of top U.S. lenders, and that payments only a few days late typically don't affect your score because they generally aren't reported until they reach that 30-day point (Experian on 30-day late payments and credit impact).

A late fee is not the same as a credit hit

That distinction matters because owners often panic too early, or worse, relax too long.

If you're a few days behind, the immediate threat is usually account-level damage. You may get charged, your lender may raise the temperature, and your internal cash discipline is already slipping. But if you cure the payment before it reaches the reporting threshold, you may avoid the long-tail credit damage.

Think of it this way:

- A short delay: hurts cash and may trigger fees.

- A reported 30-day delinquency: moves from a billing issue to a credit event.

- A continuing delinquency: becomes an underwriting problem.

What the 30-day window really gives you

That window is not permission to pay late. It's a narrow rescue lane.

Business owners should treat any missed payment notice as urgent the same day it appears. The best move is simple. Confirm the due date, make the account current, and document the payment. If the account was missed because of a cash squeeze, address the root cause immediately rather than hoping the next deposit solves it.

A payment that stays inside the 30-day window may still cost you money. A payment that crosses it can cost you financing options.

Mature operators differentiate themselves through their methods. They don't rely on memory, a buried email, or a card issuer's reminder cadence. They run a payment process. If you don't, one overlooked personal bill can become a visible mark that outlasts the quarter that caused it.

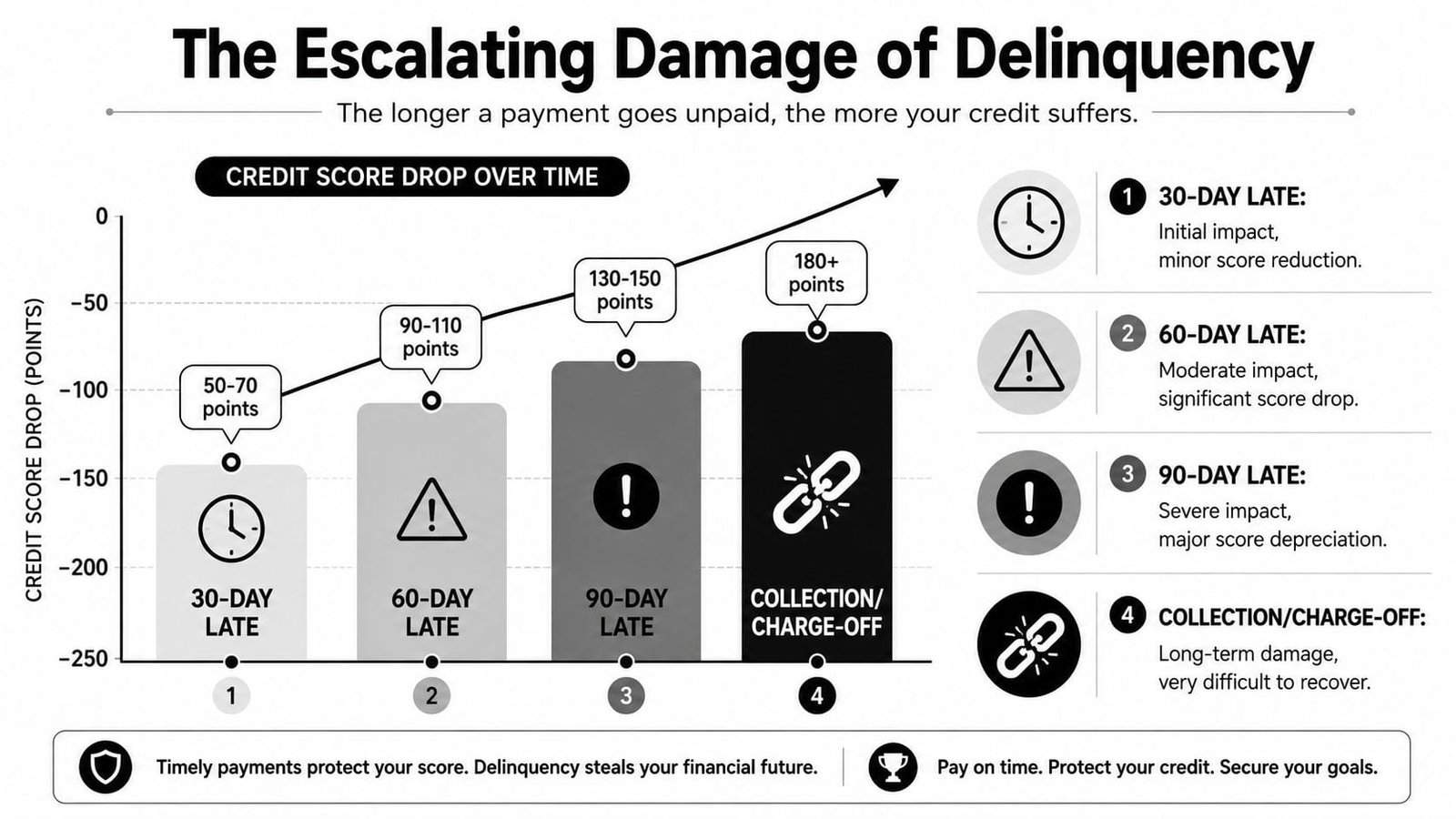

The Escalating Damage of Delinquency

The first reported late payment is bad. Letting it age into a deeper delinquency is worse.

Chase states that a single late payment reported to the credit bureaus can reduce a FICO Score by about 100 points or more, depending on the person's starting score and the scoring model. Chase also notes that the damage increases as the account moves from 30 days late to 60, 90, or 120 days late (Chase on when late payments show up and how scores react).

Why a strong borrower can feel the sharpest drop

This is one of the least intuitive parts of credit damage. Owners with cleaner files often have more to lose from a new late mark.

A borrower with a strong profile sends a clear signal to scoring models and lenders: consistent, reliable repayment. When that pattern breaks, the negative information stands out. That's why high-score borrowers often feel a steeper immediate hit than someone whose file already contains prior problems.

If you want a broader primer on what makes up your credit score, that breakdown is useful context for understanding why payment behavior carries so much weight.

The risk gets worse as the account ages

Lenders don't read 30, 60, and 90 days late as interchangeable. They read them as escalating evidence.

Here's the practical lending interpretation:

| Delinquency stage | What a lender may infer |

|---|---|

| 30 days late | You missed a payment, but may have had an isolated oversight |

| 60 days late | The problem wasn't corrected promptly |

| 90 days late or more | The account may reflect real distress or breakdown in financial control |

CNBC, citing LendingTree research on 100,000 credit reports, reports that consumers with a single missed payment average a credit score of 553, which is about 80 points lower than those with perfect payment histories. The same reporting says a 30-day late payment can drop a score by about 80 points on average, and that 90 days or more can hurt significantly more. It also notes that the mark can remain for up to seven years even after payment (CNBC on what a missed payment does to credit scores).

Recent delinquency tells a lender one thing. Unresolved delinquency tells them something worse.

For business owners, that difference matters because a 90-day late payment doesn't just shave points. It can change the entire conversation from prime credit to exception credit. That usually means fewer choices, more conditions, and more scrutiny.

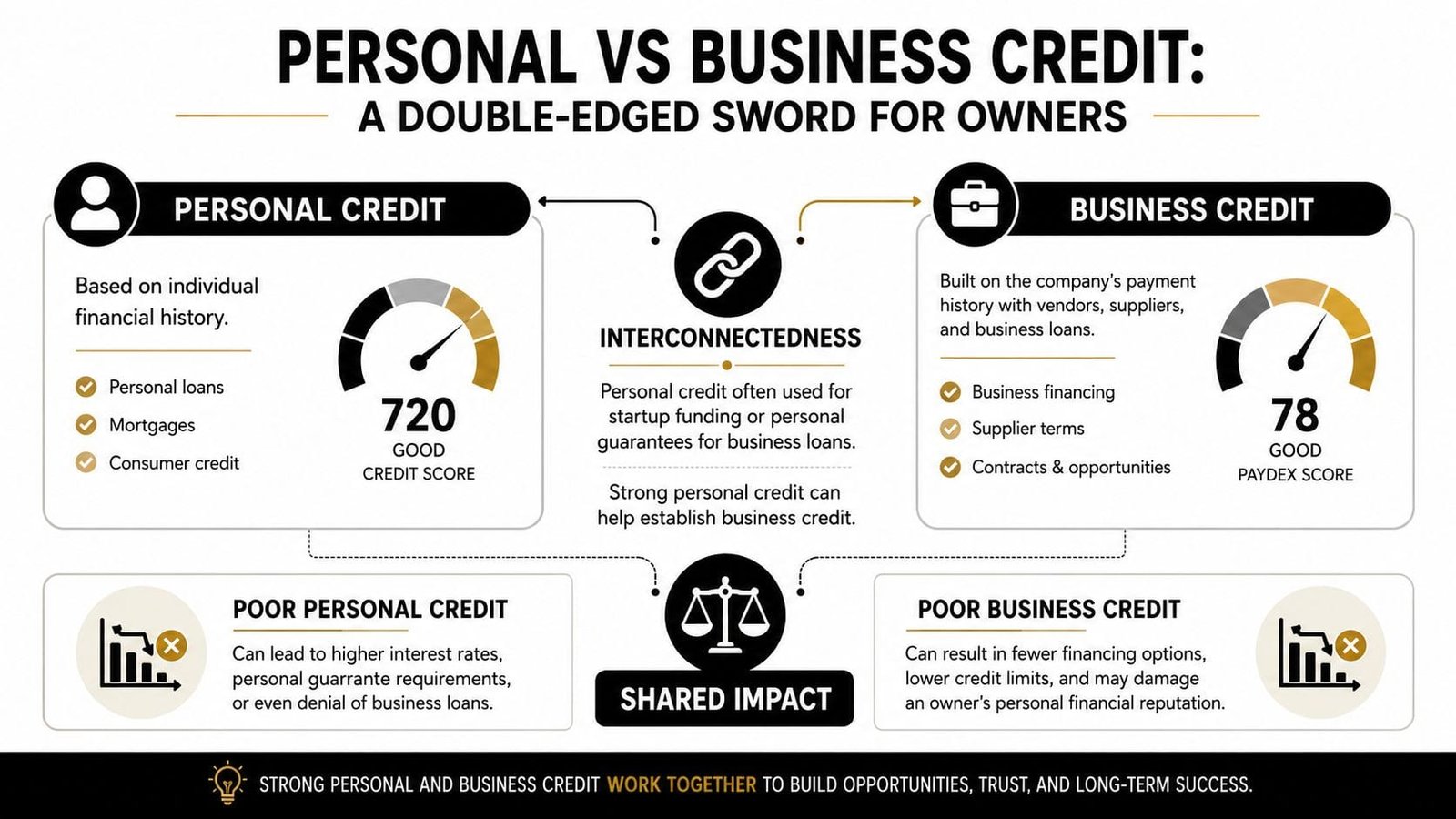

Personal vs Business Credit A Double-Edged Sword for Owners

Owners often assume personal credit and business credit live in separate silos. In real lending, they overlap constantly.

Two files, one lending decision

Personal credit follows you as an individual. Business credit tracks how the company handles trade lines, vendor accounts, and business obligations. On paper, those are separate records. In practice, lenders often evaluate both, especially when the owner signs a personal guarantee or the company is closely held.

That means a late payment on a personal credit card can spill into a business borrowing decision even when the company itself is performing well. The reverse can happen too. If the business pays vendors slowly, uses commercial credit poorly, or falls behind on business obligations, that can weaken the company's financing profile even if the owner's consumer file looks clean.

For a clear side-by-side explanation, this guide on business credit vs personal credit is a helpful reference.

Where owners get blindsided

The biggest mistake isn't misunderstanding scores. It's misunderstanding exposure.

A founder may think, "That card was personal, so it won't matter for the company." But lenders don't always separate the story that way. They ask whether the person steering the business handles obligations on time. A late mark can raise doubts about discipline, liquidity management, or both.

Here are the common blind spots:

- Startup habits that linger: Owners use personal cards for business spend, then assume one side won't affect the other.

- Strong revenue, weak controls: The company is profitable, but bills are paid reactively instead of systematically.

- Vendor drift: Trade accounts slip because the owner focuses only on bank financing and ignores business credit hygiene.

- Guarantee exposure: A personal guarantee effectively ties your personal repayment behavior to business capital access.

A lender may forgive complexity. They rarely forgive a recent sign of missed payments without asking harder questions.

The practical lesson is simple. Run both credit identities like strategic assets. Protect the owner's file because it often opens the door. Protect the business file because it supports better terms, stronger credibility, and more financing flexibility over time.

Beyond the Score How Lenders React to Late Payments

A credit score is the headline. Underwriting behavior is the consequence.

Lenders don't only ask whether your score fell. They ask what caused the drop, how recent the late payment is, whether there are multiple delinquencies, and whether the issue appears isolated or patterned. A file with one recent late payment may still get approved, but it often won't be treated the same as a clean file.

What underwriting sees

CNBC's reporting on LendingTree research says consumers with a single missed payment average a 553 credit score, roughly 80 points below those with perfect payment histories. That same reporting notes that late fees can reach up to $40, but the more serious fallout includes reduced credit limits and higher APRs on new loans (CNBC's review of missed-payment consequences).

For business owners, that means the lender's system may do one of several things:

- Flag the file for manual review: You aren't denied immediately, but the deal slows down.

- Price for risk: Approval comes back with less attractive terms.

- Ask for more support: The lender wants additional statements, explanations, or compensating strengths.

- Decline based on recency: The issue isn't your revenue. It's the freshness of the delinquency.

If you're trying to gauge how lenders typically think about borrower profiles, this overview of business loan credit score expectations gives useful context.

The cost shows up after approval too

The expensive part isn't the late fee. It's the change in lender posture.

A creditor may trim a limit. A future lender may offer a higher rate. Another may approve a smaller facility than you expected. None of those outcomes announce themselves as "punishment for that one missed payment," but that is often part of the story.

Business owners should think in terms of optionality. Clean credit preserves options. A recent late payment narrows them. When the company needs flexibility fast, fewer options usually means more expensive money.

Damage Control A Business Owner's Guide to Credit Recovery

The first move after a late payment is not to panic. It's to act quickly and document everything.

First moves that actually help

When an owner realizes a payment was missed, the priority order matters.

- Bring the account current immediately. Waiting and hoping the issue stays contained usually makes it worse.

- Call the creditor. Be concise, factual, and respectful. If the payment hasn't been reported yet, ask whether the account can remain internal if paid now.

- Record the details. Save confirmation numbers, dates, screenshots, and names of representatives.

- Review every other account the same day. One missed bill sometimes signals a process failure, not a one-off mistake.

If cash pressure caused the miss, solve the pressure point too. Owners trapped in expensive short-term funding often need to address the debt structure, not just the symptom. For that situation, this resource on how to navigate MCA debt for businesses is worth reviewing.

How to ask for a goodwill removal

If the late payment has already been reported, a goodwill letter or direct goodwill request can still be worth trying. It won't always work, but a professional request is better than silence.

Use a plain structure:

- State the account and the late date clearly

- Acknowledge responsibility without excuses

- Mention your prior payment history if it was otherwise clean

- Explain briefly why the miss occurred

- Request goodwill removal of the reported late mark

- Confirm the account is now current

Practical rule: Ask for accuracy first, goodwill second. If the reporting is wrong, dispute it. If it's accurate, request consideration.

A short explainer can help clarify the process before you make the call:

Why recovery is uneven, not linear

MyFICO states that scoring models weigh recent late payments 3 to 5 times more heavily than older ones, meaning a late payment today can hurt more than several much older delinquencies. It also notes that lender emphasis on recent credit history has grown in projected 2025 trends (MyFICO on how recent late payments carry more weight).

That changes how recovery works. Time helps, but not evenly. The freshest delinquency tends to carry the most sting. As it ages, its influence fades, especially if everything else stays clean.

That means what works is boring and disciplined:

- No new late payments

- Tight account monitoring

- Consistent on-time performance across personal and business obligations

- Clear documentation if a lender asks for an explanation

What doesn't work is waiting passively for seven years and assuming the market will ignore recency. It won't.

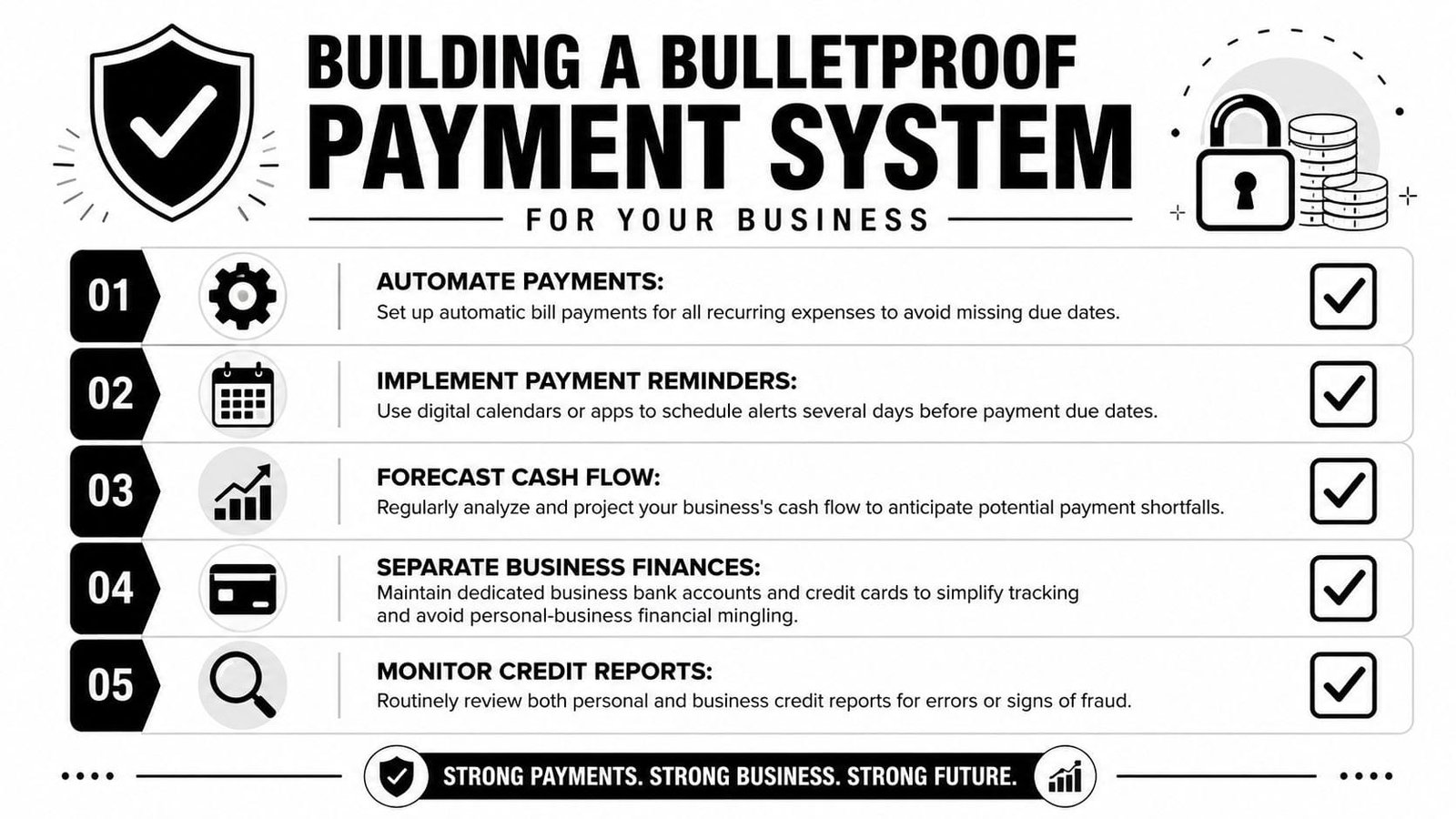

Building a Bulletproof Payment System for Your Business

The best answer to late-payment damage is prevention. Owners don't need a heroic memory. They need a system that keeps ordinary chaos from creating credit problems.

Systems beat memory

A reliable payment system should cover both personal obligations and business obligations, because lenders often evaluate both. The strongest setups are usually simple.

- Automate minimum payments: Autopay protects against the avoidable miss.

- Use a second reminder layer: Calendar alerts, banking notifications, and card issuer alerts catch failures when autopay breaks.

- Separate accounts clearly: Personal bills should never get buried inside operating noise.

- Review due dates monthly: Owners should know which obligations hit before large payrolls, tax drafts, or rent runs.

For companies tightening operations, stronger accounts receivable management practices can reduce the cash timing issues that often lead to late payments in the first place.

The simplest controls are usually the best ones

The payment process doesn't need to be elaborate. It needs to be visible, repeatable, and assigned.

A few practical controls work well:

- Dedicated cash buffer: Keep a reserve specifically for fixed obligations.

- Single dashboard review: One weekly look at upcoming due dates prevents surprises.

- Named ownership: Someone must be accountable for confirming that payments cleared.

- Clean bookkeeping tools: If your reporting is messy, due dates get missed. Owners comparing the best accounting tools for startups can use that list as a starting point for building cleaner processes.

Strong credit isn't built by reacting well to mistakes. It's built by making routine payments too organized to miss.

For business owners, that discipline protects more than a score. It protects financial standing, negotiating power, and access to capital when growth opportunities show up.

If you're planning to apply for funding, refinance debt, or secure a new line of credit, Business Loan Warrior can help you explore relevant options through one no-fee application, check pre-approval without affecting credit, and move faster with a clearer view of where your financing stands.