You're probably here because cash timing got tight fast. A customer paid late, inventory needs to go out now, payroll is coming, or an expansion opportunity showed up before your bank was ready to move. In that moment, a fast online lender like Fundbox can look like the cleanest answer on the screen.

Sometimes it is.

But for a more established business, especially one doing serious revenue and managing larger swings in working capital, speed alone isn't the right filter. The key question is whether the structure of the capital fits the job. A short-duration credit line can solve a temporary gap. It can also become an expensive habit if you use it for needs that should be financed with a larger, more structured facility.

Table of Contents

- Is Fundbox the Right Choice for Your Business?

- Understanding Fundbox's Core Offerings

- Fundbox vs Business Loan Warrior A Detailed Breakdown

- How Fundbox Compares to Other Lenders

- Which Funding Option Fits Your Business Scenario

- Secure Your Best Offer and Check Pre-Approval Now

Is Fundbox the Right Choice for Your Business?

When owners ask about Fundbox, they usually aren't asking from a calm planning cycle. They need an answer quickly. The appeal is obvious. Fundbox is a known name in online working capital, and its own company profile says it was founded in 2013, has helped more than 170,000 small businesses, and has provided over $6 billion in capital through its platform, which signals real scale rather than a niche product (Fundbox company overview).

That matters, but it doesn't answer whether it's right for your business. A product can be reputable, fast, and easy to use, and still be the wrong fit if your financing need is too large, too recurring, or too strategic for short-term revolving credit.

The first question to ask

Before you compare lenders, separate your need into one of these buckets:

- Timing problem: You're covering a near-term gap and expect cash to come back in quickly.

- Growth investment: You're funding something that should generate value over time.

- Balance sheet pressure: Your customers or operating cycle are tying up cash longer than they should.

- Capital structure problem: You've outgrown quick-access credit and need a more deliberate facility.

If you're in the first bucket, Fundbox may be a strong candidate. If you're in the last two, the conversation changes.

Practical rule: Fast capital works best when the problem is temporary. If the problem is structural, fast capital often becomes expensive capital.

A lot of businesses in the $20M+ revenue range make one mistake here. They use a small-business tool to solve a mid-market problem. That can work once. It usually doesn't work well when draws become frequent, repayment stays short, and the business needs more room than a compact line can provide.

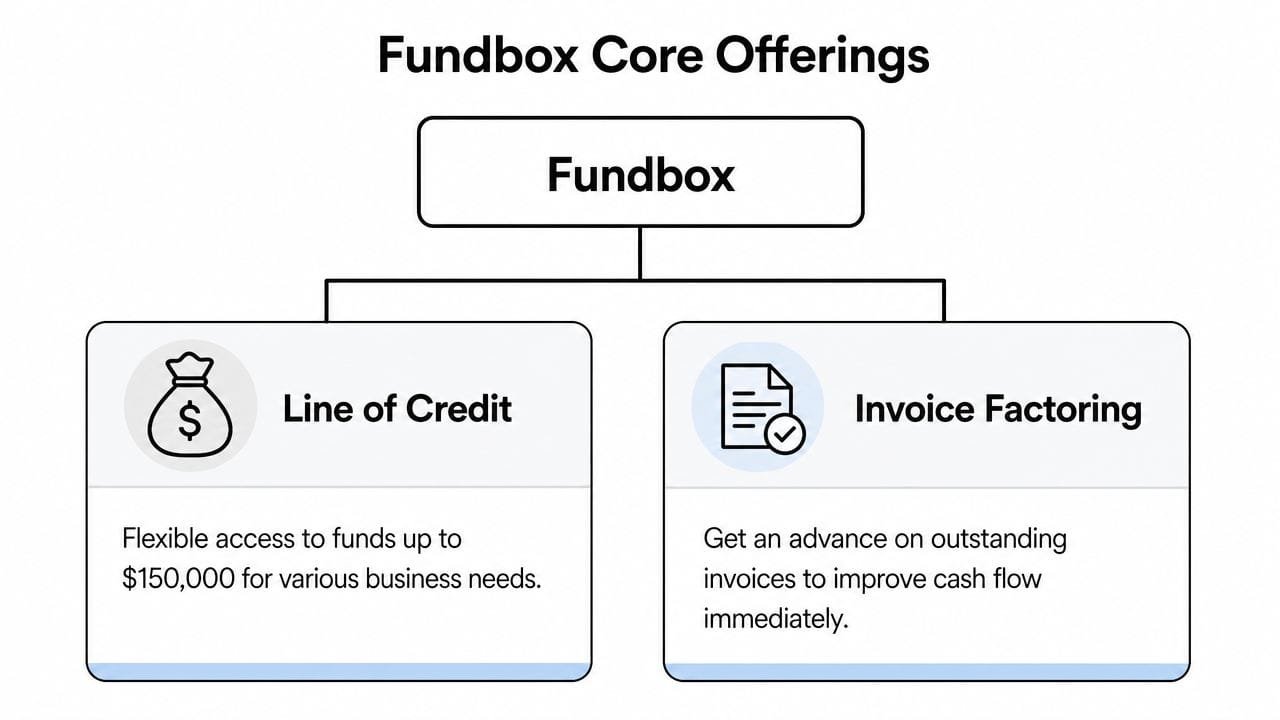

Understanding Fundbox's Core Offerings

A business usually looks at Fundbox for one reason. Cash is needed fast, and waiting through a longer bank process costs more than a short repayment schedule, at least on the surface.

What Fundbox is built to do

Fundbox is a working-capital product first. The practical use case is short-term liquidity, not long-term balance sheet planning. If receivables are slow, inventory has to be purchased now, or payroll lands before customer payments clear, a fast-access line can solve the timing issue.

That distinction matters.

For smaller firms, convenience often carries the day. For a company with more revenue, more vendor obligations, and larger borrowing needs, the better question is not whether funds are easy to access. It is whether the repayment structure fits the life of the expense.

Fundbox promotes a line of credit with relatively quick decisions, straightforward digital underwriting, and no stated origination or prepayment fee structure. Those features can make the product attractive for urgent needs. They do not reduce the importance of total borrowing cost once draws become frequent or the business starts using the line as a recurring operating tool.

How the product works in practice

The line of credit format is simple. A business draws part of its approved amount, repays on a short schedule, and regains availability as principal is paid back. That flexibility is useful when the exact cash need changes week to week.

The trade-off is repayment speed.

Short repayment cycles can work well for a brief gap that will reverse quickly. They get harder to manage when the funded use takes longer to pay off. A marketing campaign, a new location rollout, or a larger inventory build may produce returns over months, not weeks. In those cases, fast money can create pressure on cash flow before the investment has time to perform.

Some borrowers also associate Fundbox with invoice-related funding. If receivables are the core issue, that is a different analysis from using a general working-capital line. This breakdown of short-term loans, MCA, and invoice factoring is useful if you need to match the product to the actual cash-flow problem.

Where business owners misread the value

The easy mistake is focusing on the starting fee and ignoring reuse.

A draw-based product can look reasonable on day one and become expensive over a quarter if the business keeps pulling, repaying, and pulling again. We advise clients to model the full borrowing pattern, not just the first advance. That is where the true cost shows up.

A few practical rules help:

- Use short-term credit for short-term needs. If the benefit of the capital arrives slowly, the structure is usually wrong.

- Model repeated draws. The effective cost changes when the line becomes part of the monthly cash routine.

- Match loan size to business stage. Smaller flexible lines can help with gaps, but they often fall short for larger, planned capital needs.

- Watch convenience risk. Fast access is helpful. It also makes it easier to treat revolving credit like permanent working capital.

For very small businesses, those trade-offs may be acceptable because access is the main problem. For more established companies, especially businesses above the lower small-business range, Fundbox often works best as a tactical bridge rather than a primary financing strategy. Once the need gets larger, more structured, or tied to longer-term growth, the conversation shifts from speed to capital efficiency.

Fundbox vs Business Loan Warrior A Detailed Breakdown

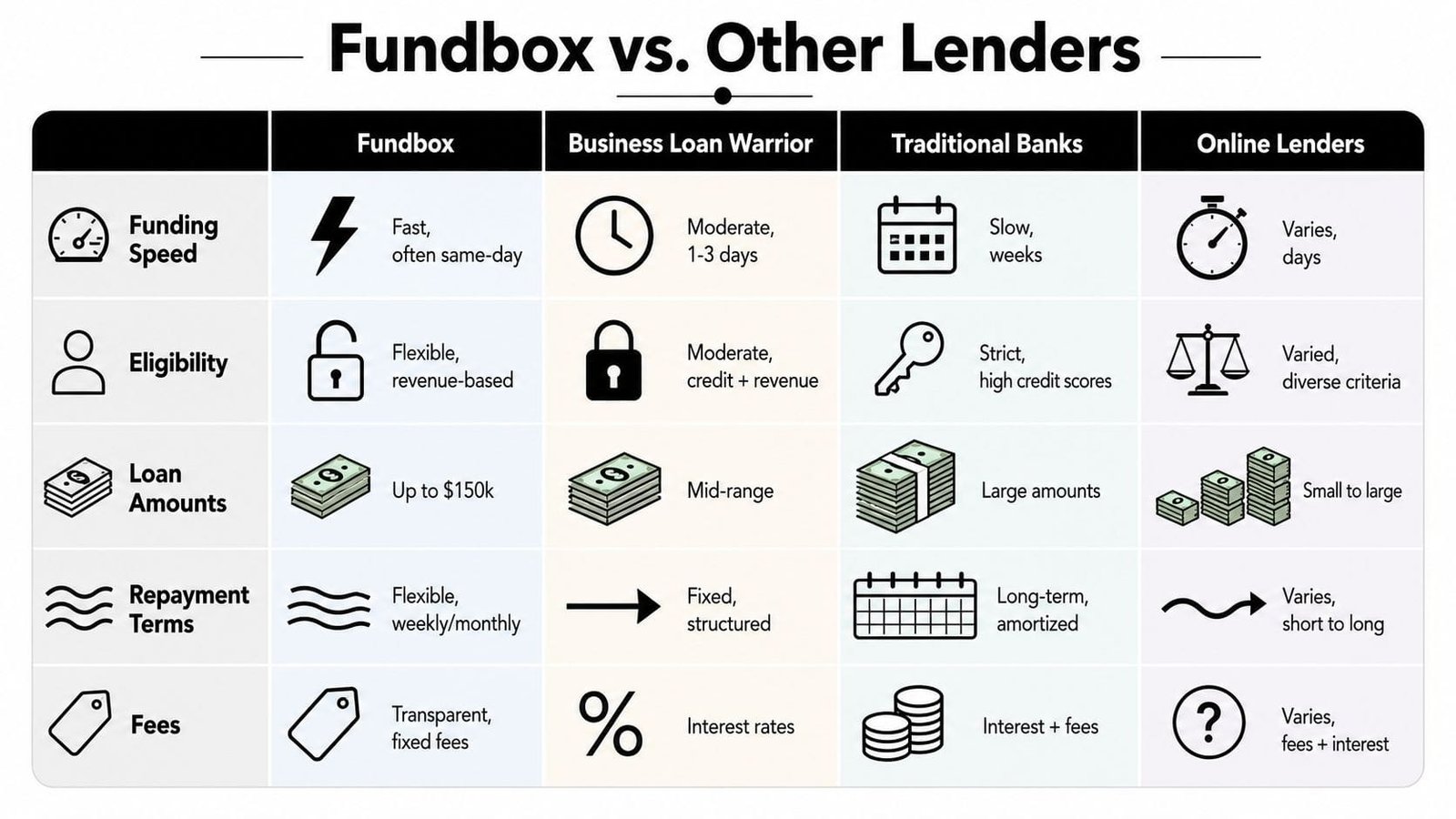

The decision now gets practical. Fundbox and Business Loan Warrior don't sit in exactly the same lane. Fundbox is primarily a fast-access working-capital option. Business Loan Warrior, based on its published offering, operates more like a broader lending platform with access to multiple structures rather than one core product family.

Fundbox vs Business Loan Warrior at a glance

| Feature | Fundbox | Business Loan Warrior |

|---|---|---|

| Primary focus | Short-term working capital | Broader small-business funding marketplace and platform |

| Typical best use | Immediate liquidity gaps, transactional funding | Matching the business with multiple funding structures |

| Product style | Fast-access line of credit and invoice-related funding | Term loans, SBA-related options, lines of credit, equipment financing, invoice financing, short-term funding, construction loans, acquisition loans, and more |

| Approval posture | More accessible underwriting for smaller businesses | More consultative fit based on need, scale, and product type |

| Best for larger established firms | Limited when the need is larger, longer, or more structured | Usually stronger when the financing need goes beyond a quick cash bridge |

| Decision lens | Speed first | Fit first |

Where Fundbox fits best

Fundbox is strongest when the business needs frictionless access and can live with a short repayment cycle. Third-party comparisons report a minimum 600 credit score, $30,000 annual revenue, and 3 months in business, with approvals sometimes issued the same day and funding within two business days (NerdWallet comparison of Bluevine vs. Fundbox).

That accessibility is a real advantage. It lowers the barrier for younger businesses and operators who don't want to spend weeks assembling a traditional loan package.

For a borrower, the upside looks like this:

- Fast access: Good for timing-driven needs.

- Low friction: Helpful when you need a decision quickly.

- Simple use case: Easy to understand if you already know you need short-term working capital.

The drawback is just as important. A short-term line is a poor substitute for financing that needs more runway. Businesses with larger revenue bases often need larger limits, longer amortization, or specialized products tied to equipment, expansion, acquisition, or project costs. Fundbox isn't built to win every one of those situations.

Where a broader lending platform fits better

A platform lender like Business Loan Warrior is built around optionality. Instead of assuming a line of credit is the answer, the process can point the borrower toward a term loan, SBA structure, equipment financing, invoice financing, or another product that better matches the use of funds.

That difference matters most for established companies. If a business is in the $20M to $50M range, the need usually isn't just cash. It's alignment between the financing and the asset or operating cycle. Short money for a long need creates pressure fast.

Here's the practical split:

- Use Fundbox when the need is immediate, short-lived, and small enough to fit a compact working-capital tool.

- Use a broader platform when the business needs a larger solution, a longer repayment path, or multiple products reviewed side by side.

- Avoid forcing speed into every decision if the cost or structure can hurt cash flow later.

A seasoned borrower usually asks three questions before choosing between these paths:

- How long will I use the money?

- How often will I need to draw again?

- What happens to cash flow if repayments start before the financed activity pays back?

If the answers point to repeated use or a longer payoff cycle, Fundbox becomes less attractive.

A quick approval feels efficient on day one. The real test is whether the repayment structure still feels efficient after the second or third draw.

That's the key trade-off. Fundbox is a tool. It's not a capital strategy by itself. More mature companies usually need the second.

How Fundbox Compares to Other Lenders

Fundbox makes the most sense when you place it in the broader lending market. It isn't trying to be a traditional bank, and it isn't identical to every online lender either. It sits in the middle ground where convenience, speed, and embedded workflow matter more than a long underwriting conversation.

Fundbox also has the balance-sheet support and private-market backing to be taken seriously in fintech. One compiled company profile reports $383.5 million raised across funding rounds and a $1.1 billion valuation, which supports the view that it has the resources to compete at scale with major online lenders (Fundbox company profile).

For visual comparison, this helps frame the scene:

Against traditional banks

Banks usually win on cost and loan size when the borrower is strong and the request fits bank credit policy. They often lose on speed, flexibility, and willingness to work with shorter operating histories or more variable cash flow.

That means the bank comparison is straightforward:

- Banks fit better for planned borrowing, larger facilities, and businesses that can tolerate a slower process.

- Fundbox fits better when timing is urgent and the business needs access without a lengthy approval cycle.

For larger established companies, banks should still be part of the conversation whenever the need is strategic rather than urgent. If the funding is for expansion, equipment, or a planned project, slower money may still be better money.

This is also where receivables-based solutions can become more relevant than general-purpose credit. Businesses dealing with invoice timing may want to review accounts receivable financing options before defaulting to a revolving line.

Against other fintech lenders

The fintech comparison is narrower. Most online lenders compete on some combination of speed, qualification flexibility, product breadth, and repayment style.

Fundbox stands out less for being the biggest facility and more for reducing friction. That's increasingly tied to its distribution model. In a May 2025 press release, Fundbox said it had shifted to a "partner-first financial infrastructure provider", signaling a model built around embedded finance inside other platforms rather than only direct lending (Fundbox press release on its new look and model).

That embedded model matters in practice because it changes how borrowers encounter the product. Instead of shopping for a lender first, they may see financing where they already manage payments, bookkeeping, invoices, or operations.

Here's the practical takeaway:

- Fundbox is attractive when the easiest capital is the capital already embedded in your workflow.

- Other fintech lenders may be stronger when you want a larger facility, longer terms, or a more customized underwriting discussion.

- Traditional lenders still matter when total cost is the top priority and timing allows patience.

A short video overview can also help if you want a quick visual take on lender categories before choosing a path.

Which Funding Option Fits Your Business Scenario

The right answer changes with the job. Fundbox can be excellent in one situation and a poor fit in the next. Most mistakes happen when owners choose based on brand familiarity instead of use case.

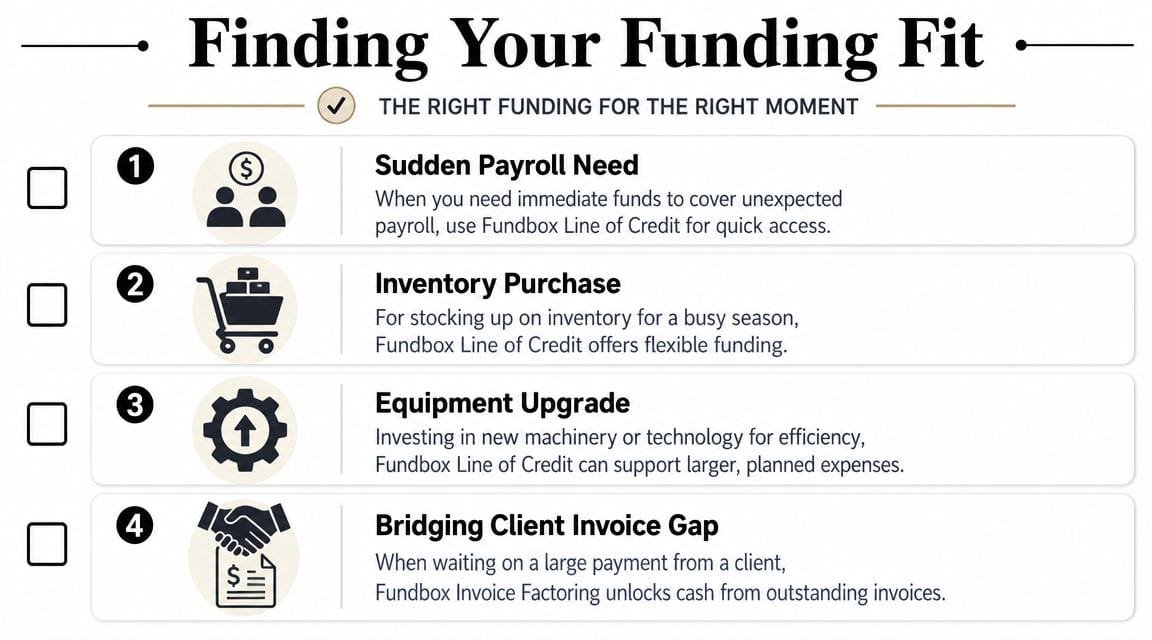

Urgent short-term operating gap

A customer payment slips. Payroll and vendor payments don't.

This is one of the clearest Fundbox use cases. If the gap is temporary and visibility on incoming cash is strong, quick-access credit can do exactly what it should do. You use it, close the gap, and get out fast.

A platform like Fundbox also benefits from being built into broader workflows. As noted in its 2025 positioning, Fundbox is leaning into a partner-first financial infrastructure model, which reinforces its strength for in-workflow, transactional funding rather than consultative, large-scale financing.

Best fit: Fundbox, if the need is short-lived.

Planned expansion or major project

A new location, major buildout, or broad growth initiative is different. The return on that investment usually unfolds over a much longer period than a short-term working-capital product is designed to support.

For that kind of use, a broader financing search usually produces better outcomes. A business should compare structured term debt, SBA-related options where relevant, construction financing, or other longer-duration products. Quick capital feels convenient, but it often compresses repayment against an investment that hasn't had time to pay back.

Best fit: A structured lending platform or bank option, not a short-duration credit line.

When the project horizon is long, match it with long-duration capital. Don't ask a working-capital tool to carry a strategic investment.

Equipment purchase with lasting value

Equipment sits in the middle. If the purchase is modest, urgent, and tied to immediate revenue, quick capital can work. If the equipment is central to operations and will deliver value over a longer period, specialized equipment financing is usually cleaner.

Why? Because the financing should track the useful life of what you're buying. Weekly or compressed repayment can strain cash even when the purchase is smart.

Consider these questions:

- Will the equipment produce cash quickly enough to support short repayment?

- Is this a stopgap purchase or a core asset?

- Would fixed structured repayment make planning easier?

Best fit: Depends on urgency and size, but larger, durable equipment usually belongs in a dedicated equipment structure.

Receivables pressure from slow-paying clients

Service firms, contractors, agencies, wholesalers, and B2B sellers deal with this constantly. Revenue is real, but cash arrives later than expenses.

In this scenario, the smartest tool often depends on what you're really solving. If you just need a bridge, Fundbox can help. If the issue is recurring invoice lag, invoice-based financing or receivables financing may be more precise because it ties capital to the asset creating the delay.

For businesses dealing with that pattern regularly, it's worth reviewing broader alternative business loan options instead of defaulting to the same line every month.

Best fit: Fundbox for occasional gaps. Invoice or receivables financing for recurring client-payment delays.

Secure Your Best Offer and Check Pre-Approval Now

A fast approval can solve the wrong problem.

That is the key decision point with Fundbox. It fits short, contained cash needs where speed matters and repayment will be quick. It gets less attractive when the need is larger, tied to a long-life asset, or part of a broader growth plan. For established businesses, especially companies doing $20 million or more in revenue, that distinction matters because the wrong structure can create cash pressure even when the capital arrives fast.

The practical mistake is judging the offer by the starting fee instead of the full borrowing pattern. As noted earlier, Fundbox presents low entry pricing, but short repayment cycles and repeated draws can push the actual cost up fast. That is why we look at total cost of capital, not just the first number in the marketing copy.

Fundbox is specific. That can be a strength.

If you need to cover payroll before a receivable clears, bridge a brief inventory gap, or handle a short-term operating squeeze, it may do the job well. If you are financing equipment, expansion, recurring working capital needs, or a larger facility with room to scale, it usually makes sense to compare against lenders that can offer longer terms and more structured repayment.

Before accepting any offer, pressure-test it against four points:

- Use of funds: Is this a short cash gap or a longer-term investment?

- Repayment pressure: Will the payment schedule fit normal cash flow without forcing weekly trade-offs?

- Repeat usage risk: Are you solving one issue, or starting a cycle of frequent draws?

- Total cost: What will this capital cost based on how your business borrows and repays?

The best offer is usually the one that still looks smart six months from now, not the one that arrives first.

If you want to compare Fundbox with term loans, SBA financing, equipment financing, invoice financing, or other working-capital products before you commit, Business Loan Warrior lets you check pre-approval through one no-fee application without affecting credit. That side-by-side view is often the better move for owners who want speed, but also want to protect margin and cash flow.