A past-due invoice isn't just an administrative chore—it's earned money you can't touch, and it directly chokes your company's ability to function and grow. Simply put, a past-due invoice is any payment that hasn't landed in your bank account by the agreed-upon due date, effectively holding your own working capital hostage.

Table of Contents

- The True Cost of Past-Due Invoices

- Your Step-by-Step Invoice Collection System

- Using Your Accounts Receivable Aging Report Strategically

- Using Financing to Bridge Cash Flow Gaps

- When to Escalate to Collections or Legal Action

- Frequently Asked Questions About Past Due Invoices

The True Cost of Past-Due Invoices

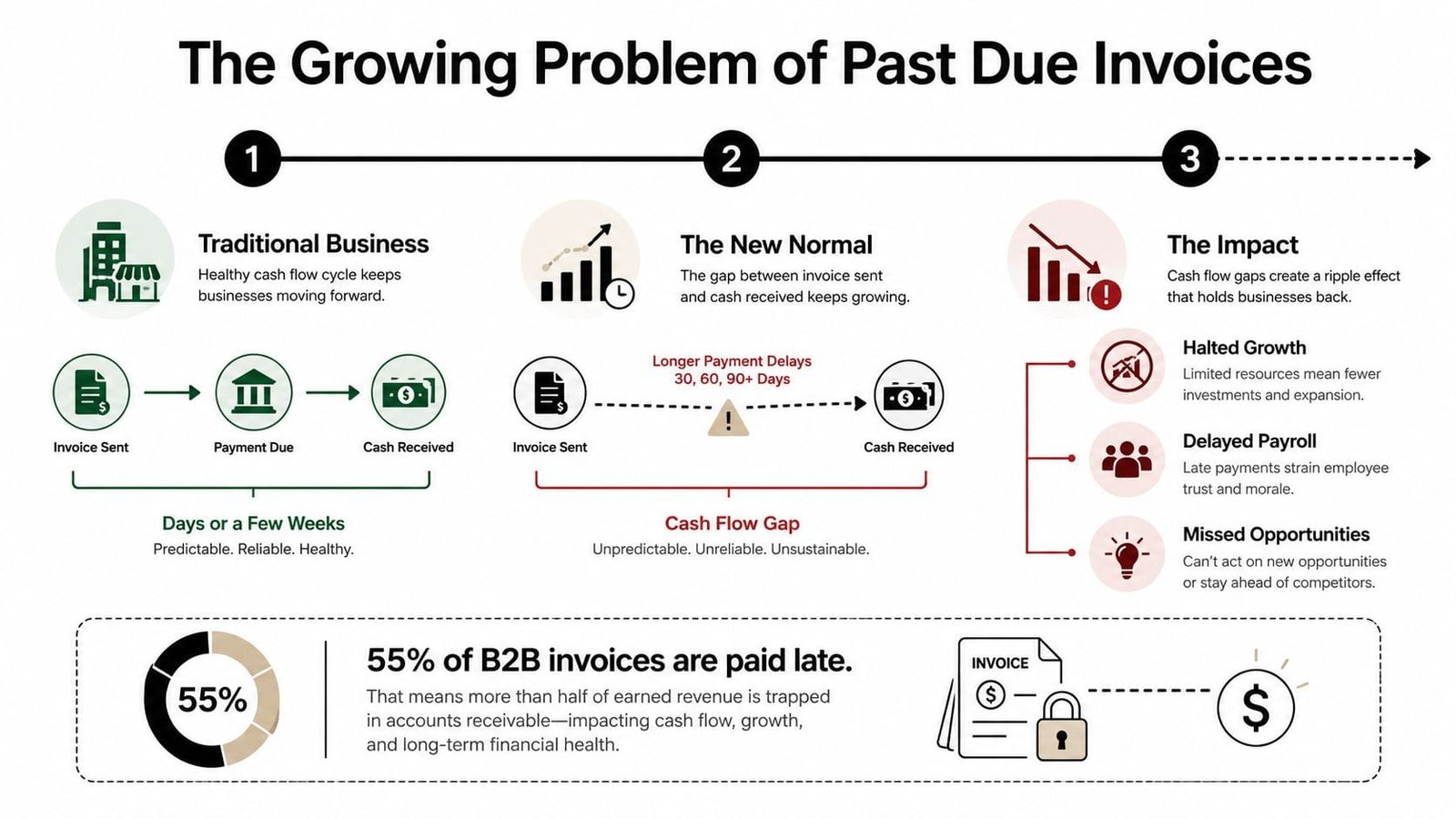

Imagine your business is a car with a full tank of gas, but the fuel line is clamped shut. You have everything you need to get moving, but you're stuck on the side of the road. That’s exactly what happens when customers pay late. These overdue payments create a constant gap in your cash flow, putting even the most profitable companies under serious financial pressure.

When a large chunk of your revenue is tied up in accounts receivable, the consequences are immediate and real. This trapped cash means you might not be able to:

- Pay your team and suppliers on time, which can hurt morale and sour valuable vendor relationships.

- Invest in new inventory or equipment, leaving you unable to keep up with customer demand.

- Seize time-sensitive growth opportunities, like launching a promising new product or expanding into a fresh market.

This isn't just a rare hiccup; for many, it's a chronic condition. Late payments have unfortunately become standard practice in the B2B world, forcing businesses to completely rethink how they manage their money.

Quantifying the Financial Drag

The sheer scale of this problem is hard to overstate. In the United States B2B market alone, an estimated 55% of all invoiced sales are paid late. That means more than half of the money businesses have already earned is just sitting in their accounts receivable, not in their bank accounts where it belongs. You can read more about how B2B late payments are impacting businesses at CashInUSA.com.

For a small or mid-sized company doing between $20 million and $50 million in annual sales, this can easily mean millions of dollars are stuck in limbo at any given moment.

This delay isn't just an inconvenience; it’s a direct threat to your financial stability. Every day an invoice remains unpaid, it erodes your purchasing power and forces you to make decisions based on cash scarcity rather than strategic opportunity.

Ultimately, the true cost goes far beyond the dollar amount on the invoice. It includes the hidden operational costs of chasing down payments, the stress it puts on you and your team, and all the lost potential from being unable to reinvest in your own company. Acknowledging this financial drag is the first step toward putting the right strategies in place to get your cash flowing again.

Your Step-by-Step Invoice Collection System

Chasing down late payments is one of the most frustrating parts of running a business. It can feel awkward, time-consuming, and even strain client relationships if not handled well. But it doesn't have to be a chaotic fire drill every month. The trick is to have a clear, repeatable system that escalates professionally over time, turning a stressful task into a predictable part of your operations.

The best approach is to start gently and only become more direct as an invoice ages. Think of it as a series of polite-but-firm nudges that respect your client's time while still protecting your own cash flow.

It’s easy to underestimate how much time this manual follow-up eats. A recent study revealed that 65% of businesses spend roughly 14 hours a week just chasing overdue payments. That’s valuable time you could be putting into growing your business. When you consider that around 55% of B2B invoices are paid late, it’s clear that automating the early stages of this process is no longer a luxury—it’s a necessity. You can see more data on how this affects companies at DocuClipper.com.

A solid collection process isn't confrontational. It's about clear communication and setting expectations. The following timeline outlines a professional way to handle invoices at every stage, from the moment they're due to when you may need to take more serious action.

Invoice Collection Timeline and Actions

| Days Past Due | Recommended Action | Communication Tone |

|---|---|---|

| 1-7 Days | Send a friendly, automated email reminder. Attach a copy of the invoice. | Gentle & Helpful. Assume it was an oversight. |

| 8-15 Days | Send a second, slightly more direct email reminder. | Courteous but Firm. Confirm they received the invoice. |

| 16-30 Days | Make a personal phone call. Speak to your contact in accounts payable. | Professional & Solution-Oriented. Ask if there's an issue. |

| 31-60 Days | Send a formal letter or email stating the invoice is seriously overdue. Mention potential late fees. | Serious & Urgent. Reference past communications. |

| 61-90 Days | Send a final demand letter. State that the account will be sent to collections if not paid by a specific date. | Formal & Conclusive. This is the last step before escalation. |

| 90+ Days | Escalate to a third-party collections agency or consider legal action. | N/A (Handled by a third party). |

This structured timeline removes the guesswork and ensures you're treating every late payment consistently and professionally, which is crucial for maintaining good records and relationships.

This infographic shows just how much late payments can disrupt the cash flow that keeps your business running smoothly.

When an invoice remains unpaid after those initial email nudges, it's time to pick up the phone. An email is easy to ignore, but a direct conversation cuts through the noise. When you call, keep it professional and focus on finding a solution together. A simple opener like, "Hi, I'm calling to follow up on invoice #123 and wanted to make sure you received it okay?" can get the ball rolling.

Pro Tip: During a collection call, document everything. Note the date, the person you spoke with, and the exact payment date they committed to. This paper trail is invaluable if you need to escalate things later.

For clients who are struggling but communicative, a structured payment plan can be a great way to recover the funds without burning the bridge. For others, you have to know when to stand firm. Mastering this balance is the core of effective accounts receivable management, which is essential for a healthy business.

Let's be honest, the best way to handle past due invoices is to make sure they never get late in the first place. While you absolutely need a system for collecting overdue payments, the real power lies in prevention. It’s a simple shift in mindset: stop chasing debt and start building a framework that encourages clients to pay on time, every time.

Think of it as setting the rules of the game before anyone even starts playing. When you're upfront and professional about your payment expectations, you create a culture of respect and accountability. This weeds out potentially risky clients from the very beginning, long before you send a single invoice.

Establish Clear Payment Terms Upfront

The cornerstone of preventing late payments is a rock-solid contract. I can't stress this enough: never start work based on a verbal agreement alone. Your service agreement needs to spell out your payment expectations in no uncertain terms.

Here are the non-negotiables your contract must include:

- Due Dates: Be specific. "Net 15," "Net 30," or "Due Upon Receipt" are clear. Vague language just invites delays.

- Payment Methods: Make it easy for them to pay you. List every method you accept, whether it's an ACH transfer, credit card, or check. More options mean fewer excuses.

- Late Fee Policy: If you intend to charge for overdue payments—and you should consider it—this must be in the contract. A common rate is 1-1.5% per month on the outstanding balance.

- Contact Information: Name a specific person or department for billing questions. This simple step prevents payments from getting stuck because someone "didn't know who to ask."

Getting these terms signed before you begin work gives you legal footing and, more importantly, ensures everyone is on the same page. This one step can head off countless headaches down the road.

Design Invoices for Immediate Action

Once the work is complete, the invoice you send is your most important tool for getting paid. A confusing or incomplete invoice is one of the most common reasons payments get held up. Your goal should be to create an invoice that is so clear, the client's accounts payable department doesn't have to think twice.

An invoice shouldn’t just be a request for money; it should be a clear, simple call to action. Make the invoice number, due date, and total amount the most prominent elements on the page.

To get your invoices paid faster, make sure they always have these elements:

- A Unique Invoice Number: This is essential for tracking the payment and referencing it in any follow-up communication.

- A Clear "Due Date": Don't bury it. Put it right at the top where it can't be missed.

- An Itemized List of Services: A clear breakdown shows the client exactly what they're paying for and builds trust.

- A Clickable Payment Link: If you accept online payments, embed a direct link. This simple addition removes friction and has been shown to cut payment times dramatically.

As a final tip, consider offering an early payment discount. Something as small as a 2% reduction for paying within 10 days can work wonders. This positive reinforcement often fosters more goodwill than the threat of a late fee and turns your accounts receivable into cash that much faster.

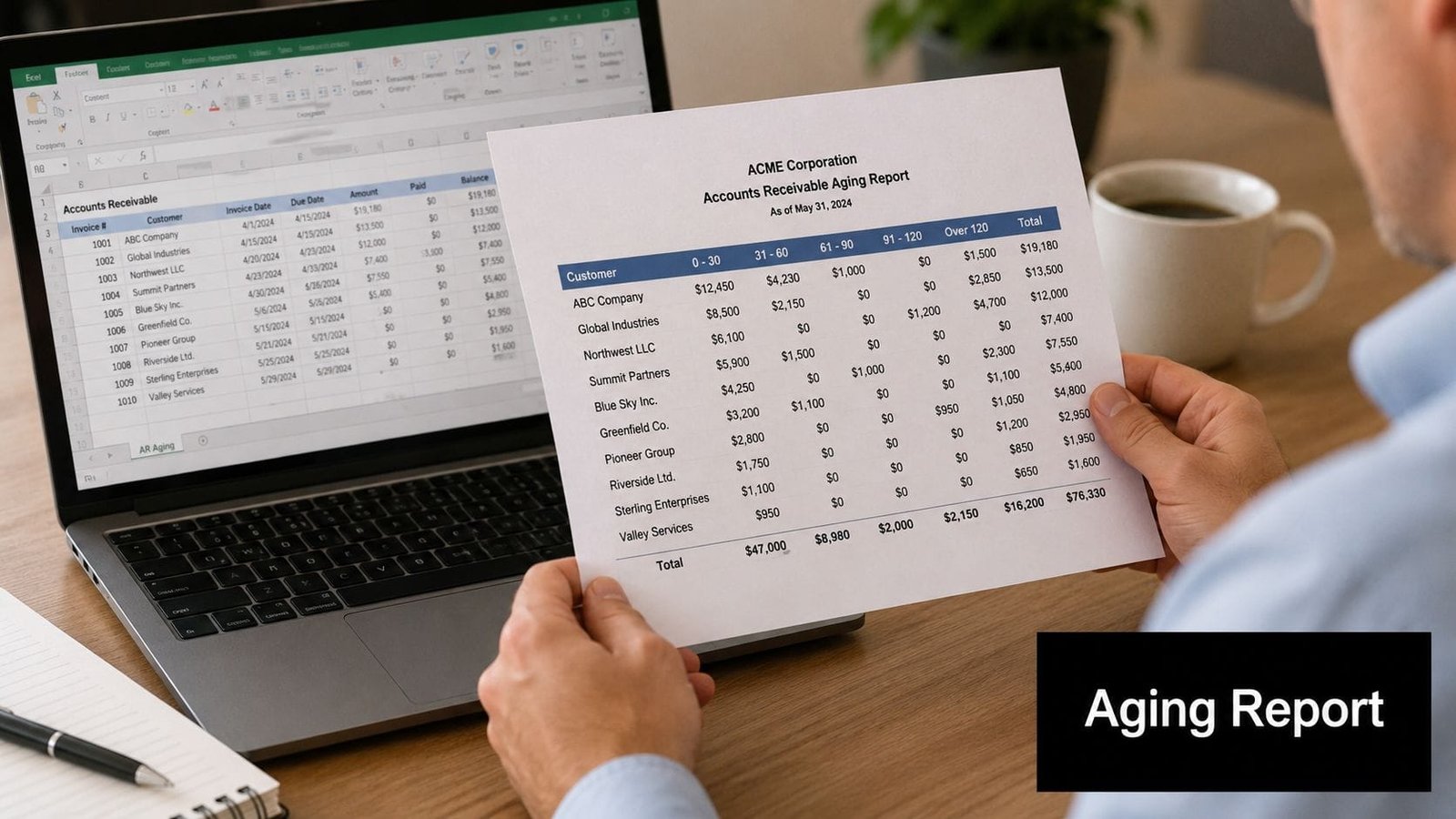

Using Your Accounts Receivable Aging Report Strategically

If you're only glancing at your accounts receivable aging report when your accountant sends it over, you're missing the plot. This isn't just another document for the books; it’s a live, strategic tool that gives you a clear view of your company's financial health. Think of it as an X-ray for your cash flow—it shows you the cracks and potential fractures before they become serious breaks.

An aging report organizes all your unpaid invoices by how long they've been outstanding. This simple breakdown tells you exactly who owes you money and, more importantly, for how long.

Typically, you'll see your receivables sorted into familiar time brackets:

- Current: Invoices that are still within their payment terms.

- 1-30 Days Past Due: These are often simple oversights and the easiest to collect with a quick reminder.

- 31-60 Days Past Due: This is where you need to start paying closer attention and making direct contact.

- 61-90 Days Past Due: A red flag. There’s likely a bigger issue with this client's payment.

- 90+ Days Past Due: At this point, you're facing a high risk that this invoice will turn into uncollectible bad debt.

Uncovering Payment Trends and Risks

When you review this report regularly, you can finally get ahead of collections instead of always playing catch-up. It helps you see patterns you'd never notice by just chasing individual invoices. You might spot a specific client, for instance, who always seems to end up in the 31-60 day column. That’s not just a late payment; that's a habit.

With that knowledge, you can act strategically. Forget sending another generic reminder for a past due invoice. It's time to pick up the phone and have a real conversation. You might discover they run all their vendor payments on the 45th day of the month. A simple tweak to their payment terms could solve the problem for good.

An aging report doesn't just show you what’s late; it helps you predict what will be late. It’s your early warning system for managing financial risk before it escalates into a crisis.

This analysis is also absolutely crucial if you plan on seeking a business loan or line of credit. Lenders will definitely ask for this report to assess how reliable your cash flow really is. If you're heading in that direction, it pays to learn how to write the AR aging narrative your lender wants to read ahead of time.

By truly understanding your aging report, you shift from reacting to overdue payments to proactively managing your financial future. You'll protect your cash flow, pinpoint at-risk accounts, and make smarter, data-backed decisions that will strengthen your business.

Using Financing to Bridge Cash Flow Gaps

Instead of letting past-due invoices call the shots, you can turn a reactive problem into a proactive strategy. Waiting for clients to pay can feel like waiting for rain in a drought—your business needs capital now, not whenever the check finally arrives. Think of financing as building your own irrigation system, one that ensures a steady flow of working capital no matter what your clients' payment schedules look like.

These aren't just emergency measures; they're smart, strategic tools for keeping your business stable and poised for growth. By using financing, you can neutralize the immediate threat of late payments and take back control of your company's financial destiny.

Turning Unpaid Invoices into Immediate Cash

One of the most direct ways to fight the effects of a past-due invoice is with invoice financing. At its core, this method lets you sell your outstanding invoices to a financing company at a slight discount. In return, you get a huge chunk of the invoice's value—often 80-95%—within just a few days.

Think of it this way: instead of having $50,000 tied up in a single unpaid invoice, you could have $45,000 in your bank account this week. The financing company takes on the task of collecting the full payment from your client. Once they get paid, they send you the remaining balance, minus their fee.

This approach instantly turns your accounts receivable into cash you can actually use. Suddenly, you can:

- Meet payroll without breaking a sweat.

- Pay your own suppliers on time, protecting those crucial relationships.

- Invest in new inventory or equipment for your next big project.

It’s an incredibly powerful tool for businesses that have reliable customers who are just notoriously slow to pay. If this sounds like a potential fit for your business, you can dive deeper into accounts receivable financing to see exactly how it works.

Creating a Financial Safety Net

While invoice financing is great for targeting specific unpaid bills, other options can give you broader protection against cash flow gaps.

- A Business Line of Credit: This is like a flexible financial safety net. It gives you access to a set amount of capital that you can draw from whenever you need it. You only pay interest on the funds you actually use, making it perfect for covering unexpected shortfalls or getting through slow months.

- A Short-Term Loan: When you need a specific lump sum for a clear purpose—like buying a large amount of inventory or bridging a seasonal gap—a short-term loan can be the answer. The repayment terms are fixed, which makes it simple to budget for.

The problem of late payments is only getting worse. Recent data shows that 56% of U.S. small businesses are currently owed money from unpaid invoices, with an average of about $17,500 outstanding per business. This is a widespread issue, and it's why lenders increasingly offer these financing products as strategic tools to protect otherwise healthy businesses from the risks of inconsistent payments. You can get more insights on this trend in a recent Intuit QuickBooks report.

By proactively using these financing options, you can ensure that past-due invoices never stop you from running and growing your business with confidence.

When to Escalate to Collections or Legal Action

You’ve done everything by the book. You’ve sent the friendly reminders, made the follow-up calls, and even issued a formal notice. But that one invoice is still sitting there, gathering dust at 90 days past due. At this stage, every extra minute your team spends chasing it is time and money you're not getting back.

This is the crossroads where you have to stop thinking about it as a "late payment" and start treating it like a serious business risk. Letting a severely overdue invoice fester any longer dramatically reduces the odds you'll ever see that money. It’s time to shift from polite reminders to decisive action.

The Final Internal Step: A Demand Letter

Before you call in the big guns, there's one last formal step you should take in-house: sending a demand letter. This isn't just another email. It's a formal, legally significant document that clearly signals you mean business. For proof of delivery, send it via certified mail.

Your demand letter should be direct and unambiguous. It must include:

- The total amount owed, including any late fees.

- A final, non-negotiable deadline for payment (something like 10 business days is standard).

- An explicit statement that if payment is not received by the deadline, you will escalate the matter to a collection agency or initiate legal proceedings.

Often, the formality and serious tone of a demand letter are enough to get a non-responsive client to finally pay up. If not, you’ll have a clean paper trail proving you made every reasonable attempt to resolve the issue amicably.

Think of the demand letter as your final, firm line in the sand. It’s a calculated, professional step that protects your business and sets the stage for what comes next if the client still refuses to pay.

Once the deadline in your demand letter comes and goes, you’re left with two main paths: handing the debt over to a collection agency or taking legal action. The best route depends on the size of the invoice, your history with the client, and what you’re willing to spend to recover the funds.

A collection agency is often the most practical choice for smaller debts. They typically work on contingency, meaning they only get paid if you do, by taking a percentage of what they recover—usually 20% to 50%. This can be a cost-effective way to get a professional chaser on the case without a big upfront investment.

For larger, more significant debts, or when there's a principle at stake, hiring an attorney might be the right move. They can help you file a suit in small claims court or, for very large sums, civil court. While it’s a more expensive and time-consuming process, the weight of a legal summons and the possibility of a court-ordered judgment can be far more compelling. This is your last resort, but it's a vital tool when a major chunk of your cash flow is on the line.

Frequently Asked Questions About Past Due Invoices

Even with the best systems in place, questions about late payments are inevitable. Let's tackle some of the most common tricky situations you'll face when an invoice goes past its due date.

How Should I Word an Overdue Invoice Reminder?

The key is to be professional, direct, and clear, but your tone should change depending on how late the payment is.

For the first follow-up, keep it light and friendly. It’s entirely possible your client just got busy and forgot. A simple note that includes the invoice number, amount, and due date is usually all it takes.

If the invoice hits 30 days past due, it’s time to be a bit more firm. You might write something like, “Following up on invoice #123, which is now 30 days overdue. Please let us know when we can expect payment.” Always attach the original invoice to every reminder and include a direct payment link to make it as easy as possible for them to pay you.

Should I Charge Late Fees on Past Due Invoices?

You absolutely can, but you have to lay the groundwork first. Your policy on late fees needs to be spelled out clearly in your client contract and listed on every single invoice you send. A common rate is 1% to 1.5% per month on the outstanding balance.

Think of late fees as both a tool and a relationship test. While they can definitely motivate a slow-paying client, consider a strategic waiver for a top-tier client. Sometimes, the goodwill you build by forgiving a small fee is worth far more than the fee itself.

When Is an Unpaid Invoice Considered Bad Debt?

An invoice crosses the line into bad debt territory once you've tried everything to collect it and have to accept that the money just isn't coming. For accounting purposes, this typically happens after an invoice is 90 to 120 days old and your calls or emails are going unanswered.

At that point, writing it off as bad debt lets you claim the loss as a business expense on your taxes, which can soften the financial blow. This is a critical move, so it's always smart to talk with your accountant to make sure you’re following the proper procedures and have the right documentation.

When past due invoices are choking your cash flow, you need a way to bridge the gap. Business Loan Warrior offers solutions like invoice financing and flexible lines of credit that are built to turn your unpaid receivables into the working capital you need now. Find the right funding to get your finances stable and focus on what you do best—growing your business. Learn more at businessloanwarrior.com.