You're probably in one of two places right now. A truck needs replacing before repair bills eat your margin alive, or a new contract is within reach and you need capital fast enough to act on it. In trucking, those moments don't arrive neatly. They show up when fuel is due, insurance renews, drivers need paying, and a customer is still on net terms.

That's why smart operators stop treating financing like a last-ditch move. They treat it like route planning. The wrong route burns time and money. The right one keeps the truck moving, protects cash, and gets you where you intended to go.

Table of Contents

- Keeping Your Trucking Business on the Road

- Decoding Your Trucking Loan Options

- Underwriting Insights Beyond Your Credit Score

- Navigating Rates Terms and Your Document Checklist

- Choosing the Right Financing for Your Next Move

- Applying Smarter Not Harder with Fintech

Keeping Your Trucking Business on the Road

An owner-operator can do everything right and still get squeezed. The load pays well, but fuel jumped, a tire issue turned into a shop invoice, and a customer payment hasn't landed yet. A fleet manager faces the same pressure at a bigger scale. One aging tractor starts breaking down more often, and every day it's off the road costs money twice: once in repairs and again in lost hauling capacity.

This is the core context for trucking business loans. They aren't just about borrowing. They're about keeping operational momentum when the business has to move before cash catches up.

The scale of the industry explains why financing is so central. The U.S. trucking industry recorded $940.8 billion in gross freight revenue in 2022, accounting for 80.7% of the total transportation industry's output, according to TruckInfo's trucking statistics research. An industry that large doesn't run on cash reserves alone. It runs on equipment, working capital, and access to funding at the right time.

Cash flow pressure isn't the same as business weakness

A carrier can be profitable on paper and still run tight week to week. That's common in trucking because money goes out daily while receivables can lag. Fuel, payroll, permits, repairs, and insurance don't wait.

That's also why risk management has to sit next to financing. If you're adding units or reviewing lender requirements, it helps to revisit commercial truck insurance essentials so coverage doesn't become the hidden cost that throws off your plan.

Practical rule: Borrow for a clear purpose. Don't use long-term debt to patch a recurring operating problem you haven't diagnosed.

Financing works best when it matches the job

A line of credit can help with uneven expenses. Equipment financing can protect cash when you need another truck. Factoring can turn delivered loads into quicker liquidity. The mistake isn't borrowing. The mistake is using the wrong product for the wrong problem.

If your operation deals with constant fuel swings and irregular receivables, a guide on how a business line of credit powers high-motion industries is worth reviewing because trucking behaves exactly like that: cash in motion, margin under pressure, and no room for downtime.

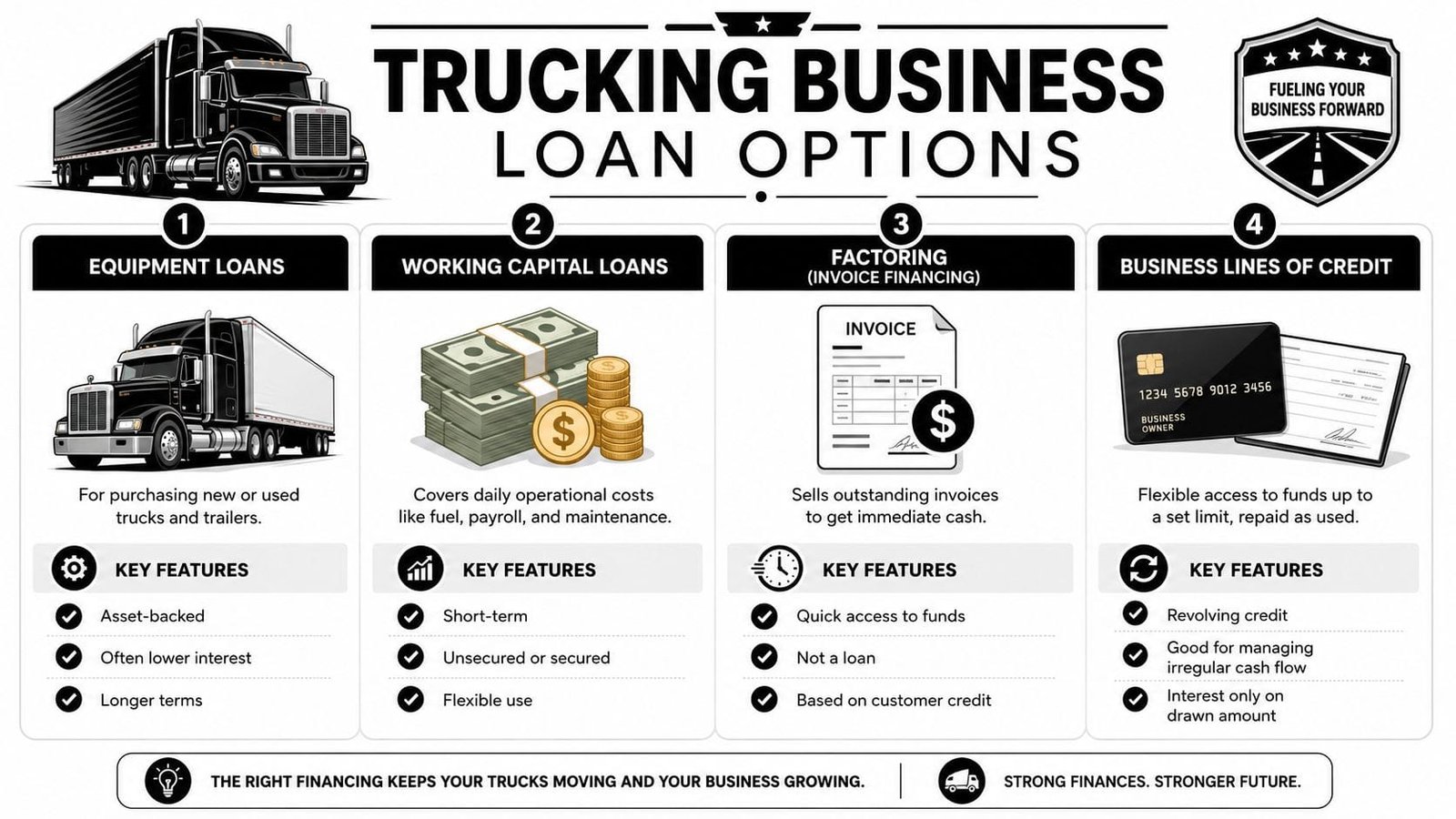

Decoding Your Trucking Loan Options

Not all trucking business loans are built the same. Some are meant to buy iron. Others are meant to keep dispatch moving while you wait to get paid. If you treat them as interchangeable, you'll usually overpay or create a repayment schedule that fights your cash flow instead of supporting it.

A simple way to think about it is this: some financing is like buying a truck engine, purpose-built and secured by the asset. Other financing is like carrying spare fuel cans, flexible and fast, but usually more expensive.

When the truck itself secures the deal

Equipment financing is usually the most natural fit when you're buying a truck or trailer. The asset serves as collateral, which is why this option often carries better pricing than unsecured borrowing. It's best when the purchase itself will generate revenue and you want payments spread across the useful life of the equipment.

SBA loans sit in a different lane. They're slower and usually more document-heavy, but they can be strong for larger purchases or expansion. For trucking businesses, loan size depends heavily on purpose. According to Crestmont Capital's guide to trucking business loans, working capital loans range from $25,000 to $250,000, business lines of credit can reach $500,000, and SBA 7(a) loans can provide up to $5 million for equipment and expansion. The same source notes that revenue-based financing uses factor rates of 1.15 to 1.45, while equipment financing rates range from 6% to 20% depending on credit and term.

If you're evaluating truck purchases alongside other heavy assets, this overview of heavy equipment loans is useful because the underwriting logic is similar. Lenders care about collateral quality, resale value, and whether the equipment produces income.

When cash flow matters more than the asset

Invoice factoring isn't a classic loan. You're converting unpaid invoices into immediate cash. That makes it useful when brokers or shippers pay slowly and your operation can't wait. It's often one of the cleanest tools for a carrier with decent receivables but tight working capital.

Business lines of credit are revolving capital. You draw what you need, repay it, and use it again. This works well for repair volatility, fuel swings, short payroll gaps, or taking on a contract that needs upfront cash before the revenue cycle catches up.

Working capital loans are more fixed. You get a lump sum and repay on schedule. They can make sense for planned operating needs, but they're less forgiving if your revenue timing gets uneven.

Merchant cash advances or other revenue-based products are usually the fastest and often the most expensive. They can help when other paths are closed, but they should be approached carefully. Fast money solves today's problem only if tomorrow's remittances don't choke your operating cash.

Here's a quick visual if you want a high-level walkthrough before comparing offers:

Trucking business loan comparison

| Loan Type | Best For | Typical Amount | Repayment Term | Funding Speed |

|---|---|---|---|---|

| Equipment Financing | Buying trucks or trailers | Varies by equipment and borrower profile | Usually tied to asset life | Often faster than SBA products |

| SBA 7(a) Loan | Expansion, larger purchases, working capital | Up to $5 million | Longer structured terms | Slower, more document-heavy |

| Invoice Factoring | Unlocking cash from unpaid invoices | Depends on invoice volume | Tied to receivable collection | Fast |

| Business Line of Credit | Repairs, fuel, payroll gaps, flexible access | Up to $500,000 | Revolving | Fast with many lenders |

| Working Capital Loan | Planned operating expenses | $25,000 to $250,000 | Fixed term | Fast to moderate |

| Merchant Cash Advance or Revenue-Based Financing | Last-resort speed when revenue is strong | Varies | Revenue-linked or frequent remittance structure | Very fast |

The best product is the one whose repayment rhythm matches how your freight revenue actually lands.

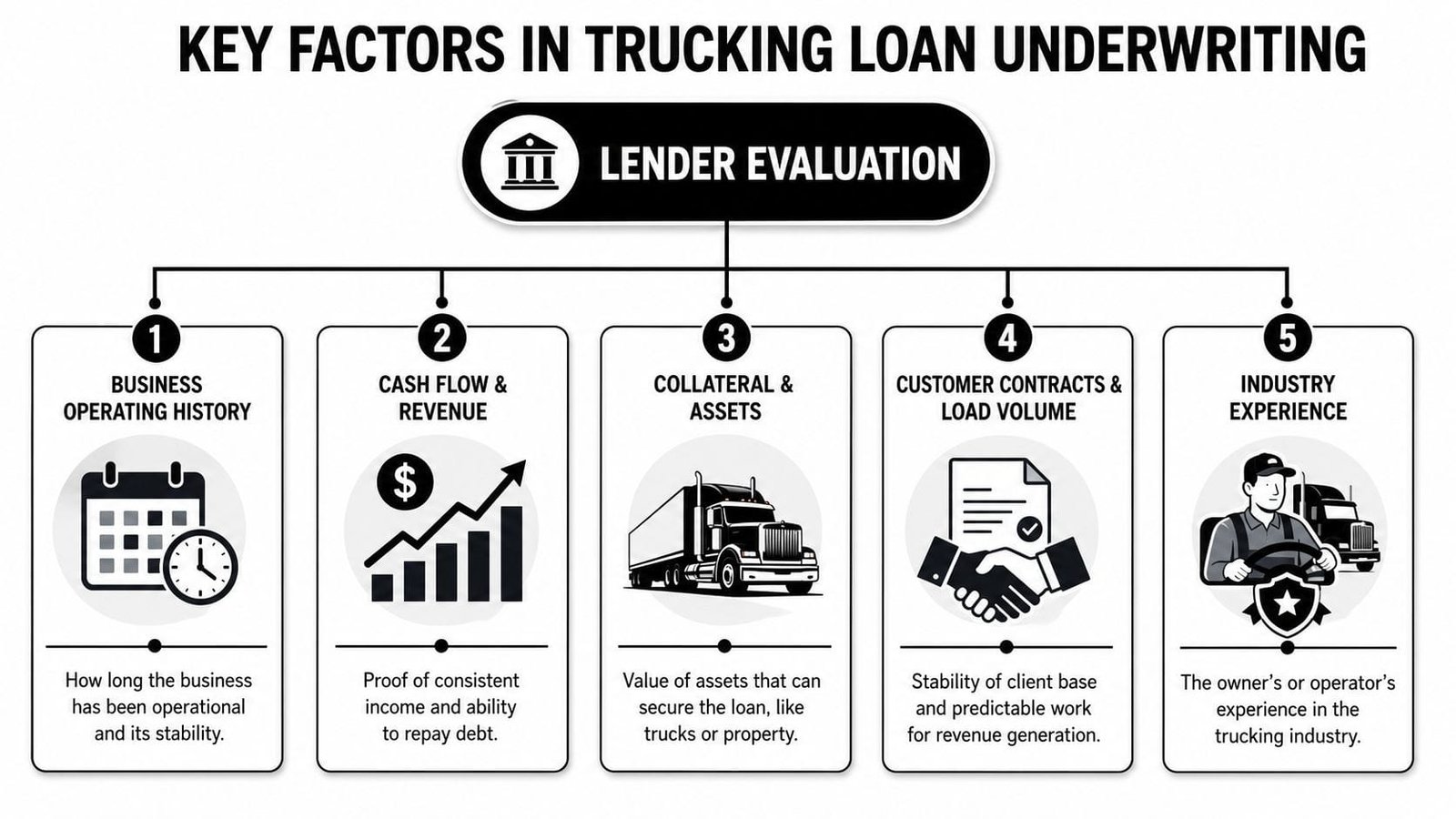

Underwriting Insights Beyond Your Credit Score

Many borrowers think a lender approves or declines a trucking loan based on credit score alone. That's not how a serious underwriter looks at a file. Credit matters, but it's just one gauge on the dashboard. Lenders also want to know whether your business generates enough dependable cash to carry the payment without choking operations.

What lenders check first

The basics are familiar:

- Credit profile: Personal credit often matters, especially for owner-operators and closely held carriers.

- Time in business: Newer companies usually have fewer options and tighter terms.

- Revenue consistency: Lenders care less about one strong month than a stable pattern.

- Collateral: For truck purchases, the age, condition, and resale profile of the unit can change the decision.

But trucking underwriters go further. They review bank activity, contract quality, dispatch stability, and whether the operation looks disciplined or chaotic. A borrower with decent revenue but irregular deposits, heavy NSF history, or no separation between personal and business spending often gets flagged fast.

Why DSCR changes the decision

One metric gets far less attention than it should: Debt Service Coverage Ratio, or DSCR. As explained in this discussion of DSCR in trucking loan approvals, lenders use DSCR to project whether a trucking business can sustain loan payments based on cash flow, not just current revenue, and it's increasingly a deciding factor for alternative lenders.

Think of DSCR as your cushion. If your business is an engine, revenue is horsepower. DSCR tells the lender whether there's enough controlled power left after operating demands to keep making debt payments reliably. Strong gross revenue with weak leftover cash is like a truck that can accelerate but overheats on every long climb.

A practical way to prepare is to rebuild your cash flow story from the lender's seat:

- Start with true operating income. Don't use top-line revenue as proof you can pay debt.

- Strip out irregular deposits. One-time injections can make the business look stronger than it is.

- Map recurring obligations. Existing truck notes, advances, cards, leases, and tax payments all matter.

- Stress-test the new payment. Ask whether the business can still carry it during a softer month.

If you need to sharpen this analysis internally, a primer on how to find net income can help because lenders care about what remains after real operating costs, not what entered the account.

A trucking loan gets approved on the lender's confidence that payment survives normal volatility.

Other risks underwriters notice fast

Beyond DSCR, I'd expect close scrutiny in three areas:

| Risk Area | What Lenders Notice | Why It Matters |

|---|---|---|

| Fleet condition | Deferred maintenance, older units with rising downtime | Reliability risk affects revenue continuity |

| Customer concentration | Too much dependence on one broker, shipper, or lane | One lost account can destabilize cash flow |

| Operating discipline | Clean statements, clear bookkeeping, organized records | A cleaner file feels lower risk |

A lot of rejections aren't really about low credit. They're about a weak operating narrative. If the file suggests thin cash cushion, unstable customers, or poor internal controls, lenders pull back even when the score looks passable.

Navigating Rates Terms and Your Document Checklist

Cost in trucking finance moves with risk. The cleaner the borrower, the stronger the collateral, and the more stable the cash flow, the better the pricing usually gets. The wider the uncertainty, the more expensive the capital becomes.

According to Bankrate's review of average semi-truck financing rates, commercial truck financing rates in 2026 exhibit a 29% APR spread, from 6% to 35%. The same source notes that traditional banks offer the lowest rates at 4% to 8% APR, while online lenders start at 8%+ and accept lower scores at higher cost.

Why one borrower gets a lower rate than another

Three practical factors usually explain the spread:

- Borrower quality: Higher credit and cleaner financials open the door to lower-cost lenders.

- Lender type: Banks usually price lower but underwrite tighter. Online and specialty lenders move faster but often charge more.

- Loan structure: Asset-backed financing generally prices better than unsecured working capital because the lender has collateral.

A lender also looks at how the requested financing fits the job. Using short-term capital for a long-life asset can create unnecessary pressure. Using long-term borrowing for a short-lived cash problem can leave you paying for yesterday's issue long after it's gone.

Don't compare offers by payment alone. Compare rate, fees, repayment cadence, prepayment rules, and how the debt fits your revenue pattern.

Your trucking loan document checklist

A complete file gets reviewed faster and usually earns more confidence. Gather these before you apply:

- Business financials: Recent bank statements, profit and loss statement, and tax returns if available.

- Entity documents: Articles of organization or incorporation, EIN confirmation, and business license records.

- Owner information: Government ID and, when relevant, CDL and background on trucking experience.

- Fleet details: A current equipment list with truck and trailer information, plus any notes on existing liens.

- Operating proof: Dispatch history, customer contracts, broker relationships, or load volume support when available.

- Insurance records: Active certificates and coverage documentation.

- Authority and compliance: DOT and MC records if applicable.

- Use of funds summary: A plain-language explanation of what you're financing and why it supports revenue or stability.

The stronger your package, the less time the underwriter spends guessing. In this market, clarity itself is a credit strength.

Choosing the Right Financing for Your Next Move

The right financing decision starts with the business problem, not the product name. A truck purchase, a receivables gap, and a regional expansion may all involve borrowing, but they should not be financed the same way.

Buying a truck or adding units

If you're purchasing your first rig or adding capacity, the core question is simple: do you need speed, or do you need long-term structure?

An equipment loan often wins when the truck itself is the center of the deal. The asset secures the financing, and that usually makes the approval logic more straightforward. This path tends to fit operators who know exactly which unit they want and need the funding built around that purchase.

An SBA 7(a) loan can make more sense when the purchase is part of a wider move. Maybe you're buying equipment, preserving working capital, and supporting expansion at the same time. In fiscal year 2025, nearly 3,800 SBA 7(a) loans were issued to transportation and warehouse companies in the United States, and those loans offer up to $5 million in financing, with interest rates starting as low as 6.5%, according to NerdWallet's guide to trucking business loans.

If you're sourcing trailers or planning equipment for rough-use operations, resources on financing for demanding jobsites can be useful because the same practical issue applies: make sure the asset, the payment, and the work cycle align.

Fixing a short cash gap

A slow-paying customer creates a very different problem. You don't necessarily need debt tied to a truck. You need liquidity.

In that case, invoice factoring is often cleaner than a term loan because it addresses the actual bottleneck, which is the lag between delivery and payment. If receivables are the issue, finance the receivable. Don't strap a longer-term obligation onto the business just to cover a temporary gap.

A line of credit can be the better answer when the problem repeats in uneven waves. Fuel spikes, surprise repairs, payroll timing, and seasonal softness all fit this pattern. A line is useful because you don't have to fully borrow upfront. You use it when needed and keep the balance moving.

Funding a larger expansion

Bigger moves require more patience and more discipline. If you're adding multiple trucks, entering new lanes, or acquiring another operation, cheap capital matters more than speed because the wrong structure can pressure the whole business for years.

Government-backed financing often stands out. Longer structure and lower starting rates can give a growing carrier room to scale without draining every operating dollar into debt service. But the application has to be lender-ready. Expansion stories fail when the borrower talks only about opportunity and doesn't prove repayment capacity.

For a larger move, I'd pressure-test five things before applying:

- Lane visibility: Are the loads durable or just temporarily attractive?

- Driver capacity: Can you staff the added equipment?

- Maintenance readiness: More units mean more downtime planning, not just more revenue potential.

- Customer mix: If expansion depends on one account, the loan becomes fragile.

- Payment tolerance: Can the business carry the new debt during a slower stretch?

A good loan should expand your options. It shouldn't turn one missed customer payment into a company-wide problem.

Applying Smarter Not Harder with Fintech

Traditional loan shopping can waste a lot of time. You fill out similar forms again and again, chase status updates, resend documents, and still don't have a clean side-by-side view of your real options. In trucking, that delay matters because equipment can get sold, repair issues can escalate, and a workable contract can pass to someone else.

That's why a fintech workflow makes sense for many borrowers. The practical advantage isn't hype. It's process. One application, cleaner document handling, faster screening, and a more organized path from inquiry to decision.

A strong platform should do a few things well:

- Reduce duplicate work: You shouldn't have to rebuild the same borrower profile for every funding conversation.

- Show options clearly: Different products solve different trucking problems. Visibility matters.

- Protect your time: Pre-approval workflows and secure account connections can speed up real underwriting.

- Keep the file organized: A dashboard beats chasing updates through scattered emails and calls.

The best borrowers still do the same fundamentals. They know what the money is for. They understand their cash flow. They prepare documents before urgency turns into panic. Fintech doesn't replace that discipline. It gives that discipline a faster lane.

If you're weighing trucking business loans and want a simpler way to compare options, Business Loan Warrior gives you a practical starting point. You can submit one no-fee application, check pre-approval without affecting your credit, connect accounts securely, and review funding paths that match how your business operates. For carriers that need speed without losing control of the process, that's a smarter way to get from application to capital.