You're probably dealing with this already, even if you haven't labeled it as financing. A supplier offers Net 30. Another gives you a little room until next month. You take delivery now because the job, the resale, or the seasonal rush can't wait. Cash stays in your account a bit longer, and the business keeps moving.

That's trade credit.

For a busy owner, the practical question isn't just what is trade credit. It's whether you're using it deliberately or just letting invoice terms pile up in the background. Used well, trade credit can protect payroll, smooth inventory buys, and reduce how often you need to reach for a bank product. Used poorly, it can become the most expensive “free” money in your business.

Table of Contents

- The Silent Engine of Your Business Cash Flow

- How Does Trade Credit Actually Work

- The Strategic Pros and Cons of Using Trade Credit

- How Suppliers Decide to Grant You Credit

- Managing Your Accounting and Cash Flow

- Trade Credit vs Other Short-Term Financing

- When to Look Beyond Trade Credit for Growth

The Silent Engine of Your Business Cash Flow

A lot of owners think of trade credit as a payment convenience. It's more useful to think of it as a supplier-funded working capital tool.

Say you need to stock shelves ahead of a busy period, order materials for a signed contract, or bring in parts before customer payments land. You could pay cash immediately and tighten your bank balance. Or your supplier could ship now and let you pay later. That gap between delivery and payment is what keeps many businesses operating smoothly.

It works like a running tab with a trusted local merchant, except in B2B form and with written terms on the invoice. You receive goods or services today. Payment happens on an agreed schedule. That might be Net 30, Net 60, or Net 90. Sometimes the supplier adds a prompt-pay incentive such as 2/10/30, which means you can take a discount if you pay within the earlier window instead of waiting for the full due date.

Trade credit isn't a niche tactic. It sits at the center of business commerce. In the United States, non-financial firms held about $5.2 trillion in trade credit outstanding as of Q1 2021, equal to 24 percent of U.S. GDP, according to the World Bank trade and value chains report. That tells you delayed payment isn't an exception. It's built into how businesses fund day-to-day operations.

Why owners lean on it

- Preserve cash: Keep money available for payroll, freight surprises, repairs, and taxes.

- Buy before cash arrives: Useful when revenue comes after delivery, installation, or resale.

- Avoid unnecessary borrowing: You may not need outside funding for every inventory or supply purchase.

- Support timing decisions: Strong payable control can help you improve B2B cash flow without cutting growth.

Practical rule: If a supplier gives you time to pay, don't treat that as administrative trivia. Treat it as part of your financing strategy.

If you want a broader operating view of where cash gets stuck, this guide on how to improve cash flow is a useful companion to the way trade credit fits into the bigger cycle.

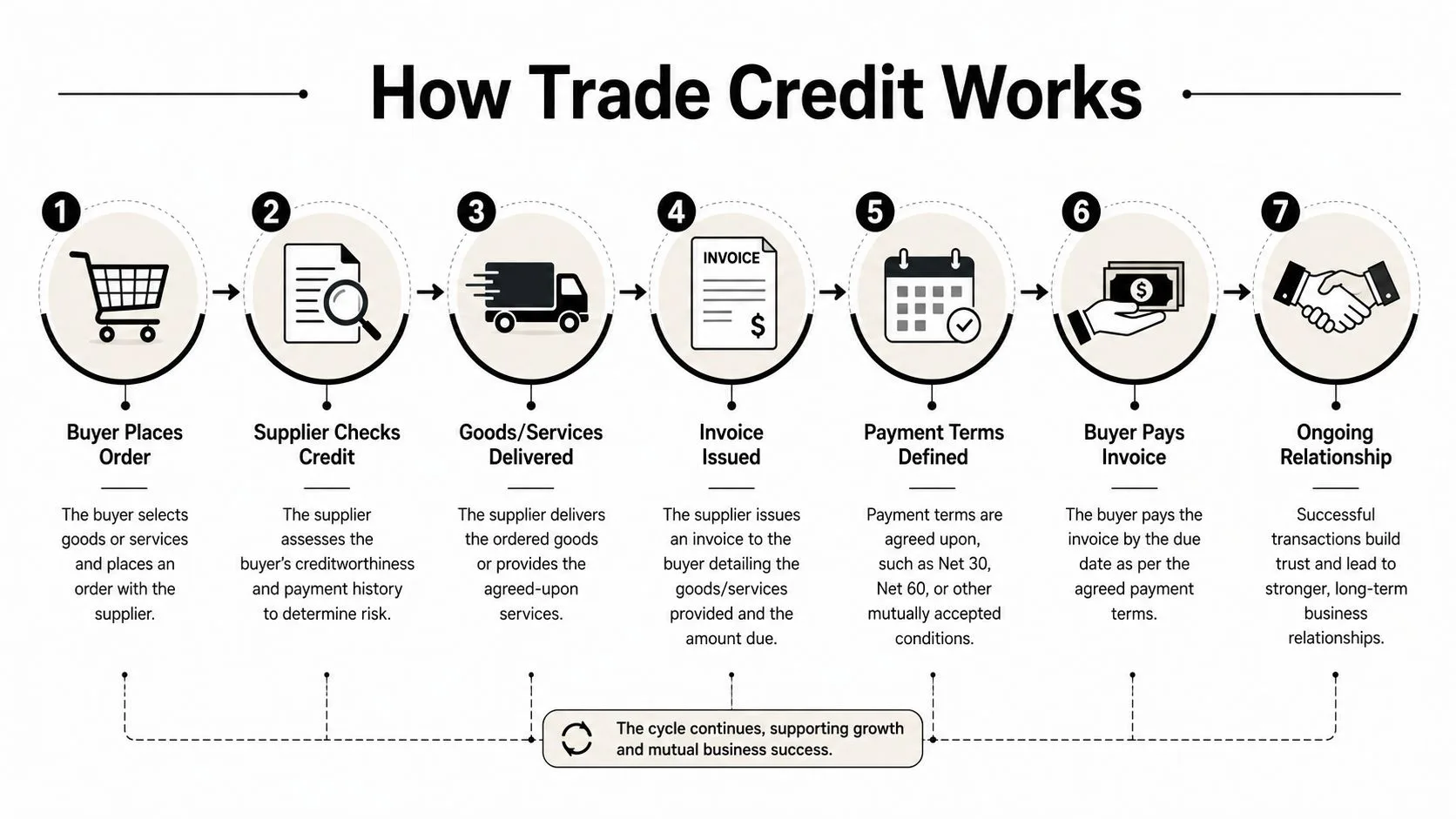

How Does Trade Credit Actually Work

The simplest way to understand trade credit is this. Your supplier acts like a short-term lender, but only for what they sell you.

The mechanics in plain English

A normal trade credit cycle usually looks like this:

- You place the order. This could be inventory, raw materials, packaging, parts, or services.

- The supplier reviews your credit profile. Sometimes that's formal. Sometimes it's based on past payment history and trade references.

- They deliver the goods or perform the service.

- They issue an invoice with terms.

- You pay according to those terms.

- Your history influences future terms. Pay reliably and you may receive larger limits or longer windows.

That's why trade credit is often described as interest-free, unsecured short-term financing. Suppliers extend payment terms without requiring the kind of formal loan process you'd expect from a bank. The Trevipay explanation of trade credit also notes that suppliers may offer early payment discounts such as 2/10/30, where the buyer gets a 2% discount if paid within 10 days rather than paying the full amount in 30 days.

Here's a quick visual walkthrough before getting into the invoice language:

What the invoice terms really mean

Owners often skim invoice terms when they're busy. That's a mistake because each code affects your cash position differently.

| Term | What it means in practice | Best use case |

|---|---|---|

| Net 30 | Full payment due 30 days after invoice | Standard operating purchases |

| Net 60 | Full payment due 60 days after invoice | Slower customer collection cycles |

| Net 90 | Full payment due 90 days after invoice | Longer project billing or inventory turnover |

| 2/10/30 | Discount if paid within 10 days, otherwise full amount due in 30 | Strong cash position and discount capture |

A common mistake is assuming longer terms are always better. They're not.

If cash is tight, using the full payment window can be smart. If cash is healthy, skipping an early payment discount may be costly. The supplier is telling you two things at once: “We'll finance this for a short period,” and “We value faster payment enough to reward it.”

Take the full term when you need the liquidity. Take the discount when your cash can earn less elsewhere than the savings from paying early.

There's another practical layer buyers often miss. Your terms don't come from goodwill alone. Suppliers manage risk behind the scenes, and that affects what lands on your invoice. A customer with clean history may get a more flexible tab. A customer that pays late, disputes often, or provides weak financial information may get tighter limits, shorter terms, or no credit at all.

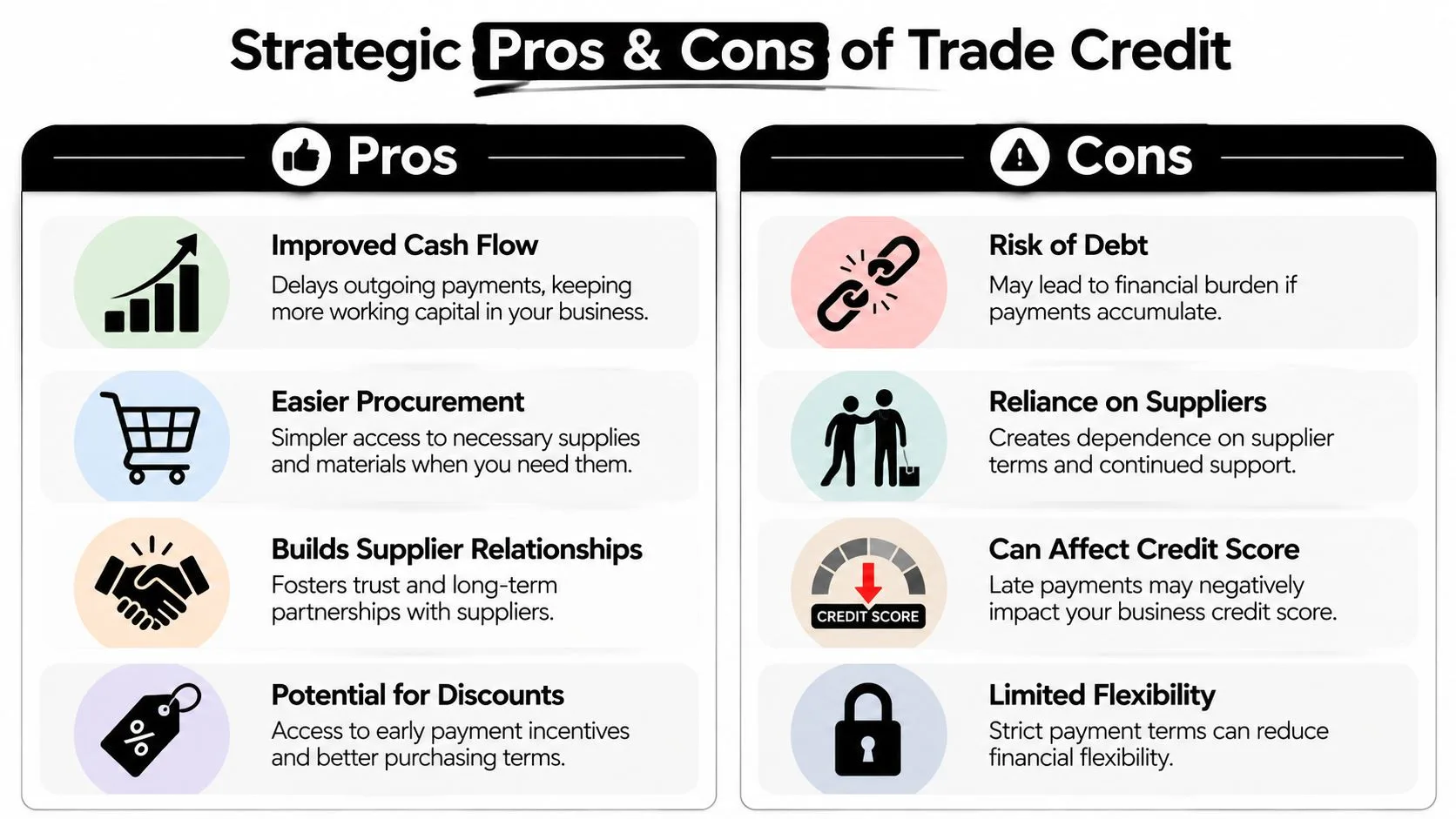

The Strategic Pros and Cons of Using Trade Credit

A profitable month can still turn into a cash squeeze if stock arrives now, payroll hits on Friday, and your customers take 45 days to pay. That is where trade credit earns its place. It gives a small business time to convert purchases into sales before cash leaves the bank.

Where trade credit helps

Used well, trade credit acts like a short-term working capital line supplied by your vendor instead of your bank. For many small businesses, that is the most accessible form of financing they can get.

The upside is practical:

- It preserves cash for higher-pressure uses. Rent, wages, tax payments, and urgent repairs usually cannot wait. Supplier terms give you room to keep trading without draining the account too early.

- It can stand in for bank borrowing. If your overdraft is small, your loan application is slow, or you do not want more bank debt on the balance sheet, supplier credit can fund day-to-day trading.

- It supports growth in a measured way. You can take on larger orders or hold more inventory without paying for every input upfront.

- It strengthens commercial relationships when managed well. Suppliers often back customers who pay predictably and communicate early when something changes.

That last point is often underestimated. A reliable trade credit record does more than keep goods flowing. It can improve the terms you are offered over time, which effectively lowers the cost of financing your operations.

Where it can hurt

Trade credit gives you room, not immunity, so managing it well is critical.

The first risk is timing. If supplier invoices fall due before customer cash comes in, trade credit stops helping and starts amplifying pressure. A business can look busy on paper and still run short of cash in the bank.

The second risk is that the price is not always obvious. Some suppliers will give longer terms but hold tighter on unit pricing, minimum order quantities, or delivery flexibility. Others may offer a prompt-payment discount that is financially better than using the full term. The smart choice depends on your margin, your cash position, and what that cash could earn or save elsewhere.

There is also a risk layer many owners never see. Suppliers assess your account the same way a lender would. In many cases, they also protect themselves with insurance or external credit controls. If your business looks harder to underwrite, the terms usually tighten. Credit limits come down. Documentation requests go up. Patience gets shorter. The TradeAventus supplier risk guide gives a useful look at how that process shapes the terms buyers receive.

Owner's lens: The real cost of trade credit often shows up off the invoice. You see it in lower credit limits, reduced flexibility, and suppliers who stop releasing orders until aging balances are cleared.

A quick check usually reveals whether trade credit is helping or becoming a problem:

- Payment behavior: Are invoices paid to plan, or only after reminders?

- Cash conversion: Will the goods be sold, delivered, and collected before payment is due?

- Supplier dependency: Would one supplier cutting your limit disrupt operations?

- Term selection: Are you choosing full terms or early-pay discounts deliberately, based on return, not habit?

- Communication quality: If cash gets tight, do suppliers hear from you early or after the due date passes?

Well-run businesses treat trade credit as part of their financing mix. Poorly run businesses treat it as extra time and hope the bank balance catches up. That difference shows up fast in cash flow.

How Suppliers Decide to Grant You Credit

Suppliers don't grant terms because a customer asks nicely. They extend credit when the risk feels acceptable and the relationship looks worth supporting.

What suppliers actually review

For a small business, getting trade credit usually starts with trust signals. If you're new, many suppliers want cash upfront or references before they'll open terms. The trade credit policy reference from PHDCCI notes that new buyers are often required to pay cash until trust is established, and that reliable transaction history or credit references matter.

In practice, suppliers often look at a mix of the following:

- Trade references: Other vendors who can confirm how you pay.

- Payment history: Whether you pay on time and without repeated excuses.

- Business profile: Time in business, ownership structure, and operating stability.

- Financial visibility: Basic statements that show whether the business appears solvent and organized.

- Order behavior: Consistent purchasing is usually more attractive than erratic one-off demand.

If you want to understand the thinking behind that process, this TradeAventus supplier risk guide gives a useful outside-in view of how vendors assess exposure.

How this shows up in your books

When a supplier grants terms, the invoice lands in Accounts Payable. That matters because payables are not just a stack of bills. They're part of how your business funds current operations.

A simple before-and-after view makes this clearer:

| Scenario | What happens operationally | Cash flow effect |

|---|---|---|

| Pay supplier immediately | Inventory or materials are purchased with cash on day one | Cash drops now |

| Use trade credit | Inventory or materials arrive, invoice sits in payables until due date | Cash stays available longer |

That extra time can help you cover payroll, freight, rent, or unexpected repairs before the supplier payment leaves the account.

A supplier extending terms is voting on your reliability. Every on-time payment is part of the next credit decision.

If you want better terms, act like a lower-risk buyer before you ask for them. Keep books current. Resolve disputes quickly. Don't surprise suppliers with silence when cash gets tight. Owners who communicate early usually preserve more flexibility than owners who disappear until the invoice is overdue.

Managing Your Accounting and Cash Flow

Trade credit only helps if your accounting team, bookkeeper, or controller treats it as an active lever. If no one is watching due dates, discount windows, and supplier priority, it stops being strategic and starts becoming reactive.

Treat payables like a control panel

At the accounting level, trade credit sits in Accounts Payable. At the cash level, it gives you timing options. The job is to use those options without damaging supplier trust.

A workable routine looks like this:

- Track invoice dates tightly: Use QuickBooks, Xero, NetSuite, or your ERP to flag due dates and discount deadlines.

- Segment suppliers by importance: Critical vendors should never be surprised by avoidable lateness.

- Match payment timing to cash conversion: If a product will sell fast, paying early for a discount may make sense. If cash is tight and sales are slower, preserve liquidity.

- Communicate before problems hit: Suppliers are more flexible when they hear from you before the due date, not after.

Trade credit gives you room, not immunity. A payable that's managed well protects cash. A payable that's neglected becomes a relationship problem.

For owners trying to tighten process, this guide to accounts payable management is useful because it connects the bookkeeping side with the cash side.

A practical decision matrix

Not every short-term funding need should be solved with supplier terms. Here's a straightforward way to think about the main options.

| Financing type | Ideal use case | Cost structure | Speed of access |

|---|---|---|---|

| Trade credit | Buying inventory, materials, supplies, or vendor services | Often no explicit interest, but may include missed discount cost | Fast if terms already exist |

| Line of credit | Flexible cash for mixed operating needs | Typically interest-bearing | Depends on lender setup |

| Invoice financing | Unlocking cash tied up in unpaid customer invoices | Financing cost tied to receivables | Often useful when receivables are strong |

Trade credit is strongest when the need is directly tied to a supplier purchase. A line of credit fits better when cash needs are broader, like payroll gaps or multi-use working capital. Invoice financing fits when customers owe you money and you need access before they pay.

The mistake is using one tool for everything. Good operators match the financing tool to the cash-flow problem in front of them.

Trade Credit vs Other Short-Term Financing

Trade credit deserves a place in your financing toolkit, but it shouldn't be confused with a universal solution. It's best for supplier purchases. It's not designed to fund every growth decision, every rough patch, or every timing mismatch.

Short-Term Financing Options Compared

Research has shown that small firms often rely more on trade credit when bank credit isn't available, which is why it functions as a substitute for traditional lending for many smaller businesses. That point is captured in the Review of Financial Studies research on trade credit use when bank credit is constrained. But substitute doesn't mean perfect replacement.

| Financing Type | Best For | Cost Structure | Access & Flexibility |

|---|---|---|---|

| Trade Credit | Inventory, materials, recurring supplier purchases | Often embedded in payment terms, with possible discount trade-offs | Limited to what suppliers will extend |

| Line of Credit | General working capital, uneven expense timing, emergency liquidity | Interest-based revolving access | More flexible use across business needs |

| Invoice Financing | Businesses with cash tied up in receivables | Cost tied to financed invoices | Access depends on receivable quality |

The main advantage of trade credit is precision. You need goods. The supplier funds the timing. Clean and efficient.

The main limitation is scope. You can't usually use supplier terms to cover rent, payroll, marketing, a software overhaul, or a major repair unless those costs are bundled into a supplier relationship. Even then, limits are based on what that supplier is comfortable carrying, not what your broader business needs may require.

Where trade credit stops being enough

Here's the practical test. Ask whether the problem is purchase-specific or business-wide.

If you need stock for an order you know you can sell, trade credit is often the right first move. If you need flexible cash that can move across categories, a line of credit is usually a better fit. If the business is profitable but cash is stuck in receivables, invoice financing is the cleaner answer. For owners comparing receivables-based options, this explainer on what invoice factoring is helps clarify where that tool fits.

There are also hybrid situations. Some owners use trade credit for inventory timing, then layer in cards or formal lending for everything else. If you're evaluating revolving spending tools without tying them to the owner personally, this roundup of business credit cards without a personal guarantee is a useful adjacent resource.

Use trade credit for what suppliers are good at funding. Use formal financing for needs that go beyond the supplier invoice.

That distinction matters because businesses get into trouble when they try to stretch supplier credit into jobs it wasn't built to do.

When to Look Beyond Trade Credit for Growth

Trade credit is excellent for operations. It's not the best tool for major expansion.

If you're opening another location, buying equipment, funding a construction project, acquiring a competitor, or carrying a growth plan that requires more capital than your suppliers will support, trade credit starts to hit its ceiling. Supplier terms are tied to purchases and relationships. Growth capital needs more range than that.

A few signs it's time to look beyond trade credit:

- Your need is larger than supplier limits. Even strong vendors won't carry unlimited exposure.

- The use of funds isn't supplier-specific. Payroll, build-outs, marketing pushes, and acquisitions usually need broader financing.

- You're juggling too many due dates. If vendor payments are driving constant cash pressure, a different structure may be healthier.

- You need predictability. Formal financing can be easier to plan around than hoping a supplier extends more room next quarter.

There's also a negotiation lesson here. Businesses get better trade credit terms when they don't look desperate for them. If you have alternative financing available, you can choose which invoices to stretch, which discounts to take, and which suppliers to pay early to deepen the relationship.

Trade credit works best as part of a capital stack, not as your entire short-term funding plan.

If trade credit is helping you run the business but not giving you enough room to grow it, Business Loan Warrior can help you explore the next step. Through one no-fee application, you can review suitable funding options for working capital, lines of credit, equipment, short-term financing, invoice funding, and more, without turning your supplier relationships into your only source of liquidity.